You’ve probably never heard of CGI, Inc. (TSE:GIB.A) (NYSE:GIB), but it’s a relatively large Canadian company with a C$27.1 billion market cap. It also has a Strong Buy rating from analysts, an “outperform” Smart Score rating, and it outperformed most tech stocks last year (it’s not far away from its all-time high). CGI, Inc. provides information technology (IT) and consulting services across many countries. It’s a very profitable company with a quantifiable competitive advantage, and its shares look reasonably valued. Since this is the type of stock that the market likes these days, it’s not unreasonable to believe that CGI can continue to perform well.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

How Can We Determine CGI’s Competitive Advantage?

Its Earnings Power Value Advantage

There are a couple of ways to quantify a company’s competitive advantage using only its income statement. The first method involves calculating a company’s earnings power value (EPV), a metric made famous by Professor Bruce Greenwald from Columbia University.

Earnings power value is measured as a company’s EPV adjusted earnings, divided by the weighted average cost of capital (WACC), and reproduction value (the cost to replicate/recreate the business) can be measured using a company’s total asset value. If the company’s earnings power value is higher than its reproduction value, then it’s considered to have a competitive advantage.

That may sound complicated, but let’s break down the numbers and explain.

For CGI, the calculation is as follows:

EPV = EPV adjusted earnings / WACC

C$20.48 billion = C$1.7 billion / 0.083

Since CGI has a total asset value of C$15.18 billion, we can say that it does have a competitive advantage. In other words, assuming no growth for CGI, it would require C$15.18 billion of assets to generate C$20.48 billion in value over time.

CGI’s Expanding Gross Profit Margin

The second method to determine if a company has a competitive advantage is by looking at its gross margin because it represents the premium that consumers are willing to pay over the cost of a product or service. An expanding gross margin indicates that a sustainable competitive advantage is present.

If a company has no edge, then new entrants would gradually take away market share, leading to decreasing gross margins over time due to pricing wars.

In CGI’s case, its gross margin has expanded in the past several years, going from about 29.5% in Fiscal 2014 to 31.6% in the past 12 months. This indicates that a competitive advantage is present in this regard as well.

CGI’s Valuation Looks Reasonable

CGI, Inc. is expected to produce earnings per share of C$6.70 and C$7.27 based on analyst estimates for Fiscal 2023 and Fiscal 2024, respectively. This brings its forward P/E ratio to 17.4x for 2023 and 16x for the next year. These numbers also suggest high-single-digit earnings growth. Although this isn’t a screaming bargain, we think that this is a reasonable valuation for an established tech company such as CGI.

The company’s earnings growth should also be aided by buybacks in the future, as its five-year average buyback yield comes in at 4.1%.

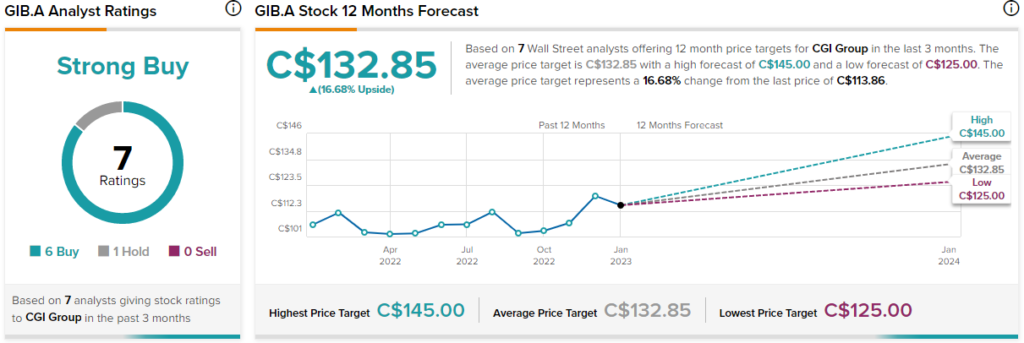

What is the Price Target for GIB.A Stock, According to Analysts?

CGI, Inc. has a Strong Buy consensus rating on TipRanks based on six Buys and one Hold rating assigned by analysts in the past three months. The average GIB.A stock price target of C$132.85 implies 16.7% upside potential.

The Takeaway: CGI is a Solid Company That’s Reasonably Valued

CGI, Inc. has a quantifiable competitive advantage based on expanding gross margins and its earnings power value. Also, it’s trading at a reasonable valuation when taking into account its growth potential. Analysts remain optimistic about the stock, and it’s possible that it can continue outperforming the overall tech market.