Cathie Wood has built a reputation as one willing to bet on disruptive tech and potential game-changing stocks. It’s a strategy the ARK Invest CEO has stuck to whether her choices have easily outperformed the market – as was the case during the pandemic – or badly trailed it – as happened last year.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

So far, this year, Wood’s flagship fund, the ARK Innovation ETF, has done rather well, showing year-to-date gains of a market-beating 24% although the ETF still remains some distance off the highs notched back in February 2021.

As someone who goes against the grain, Wood is also known to be a bit of a contrarian, and not everyone on Wall Street is always supportive of her stock choices. In fact, Wood has recently been loading up on two equities that the analysts at banking giant Goldman Sachs believe are not suitable for adding to a portfolio at this time.

We thought we’d get the lowdown on the pair and have opened the TipRanks database to see what the rest of the Street has to say about these choices. Here are the results.

Palantir Technologies (PLTR)

Cathie Wood’s favorites are often companies operating at the cutting edge of tech, and the first name we’ll look at offers just that. Palantir is described as a Big Data company as it specializes in providing software solutions that help organizations manage and analyze large and complex datasets. The company’s software is designed to handle massive amounts of data, and it can process, store, and analyze it in real-time. This enables clients to identify patterns, uncover insights, and make data-driven decisions in a more efficient and effective way.

Such a proposition has proven to be particularly valuable to governments, who have been the main revenue source for the company. The commercial sector has proved harder to crack although the company has been making a concerted effort to gain more share of the market.

Nevertheless, government sales accounted for the bulk of revenue again in the recently released Q1 report. Total revenue rose by 18% year-over-year to $525 million, while beating the Street’s call by 19.25 million. Of that, government revenue accounted for $289 million (up 20% y/y) and commercial revenue $236 million (up 15%).

Adj. EPS of $0.05 also came in ahead of the $0.04 forecast and for the full-year, the company expects revenue in the range between $2.185 – $2.235 billion, at the midpoint above consensus at $2.2 billion.

The Street liked the results, subsequently sending shares higher. Wood must have liked them too. A couple of days later, on May 10, she bought 3,757,000 shares via the ARKK ETF and an additional 614,547 shares through the ARKW fund. In total, these purchases are now worth over $41.5 million.

However, scanning the latest print, Goldman Sachs analyst Gabriela Borges thinks now is not the time to be picking up PLTR shares.

“We still think that it is difficult to own the stock given the lack of visibility and disclosures, specifically around the Government side of the business, even though we believe Palantir’s technology positioning is interesting. Additionally, given the volatility in SPAC revenue, <10% growth in the International business, and the possibility for disruptions in the US Government segment from a continuing resolution and/or debt ceiling negotiations, we await a better entry point,” Borges opined.

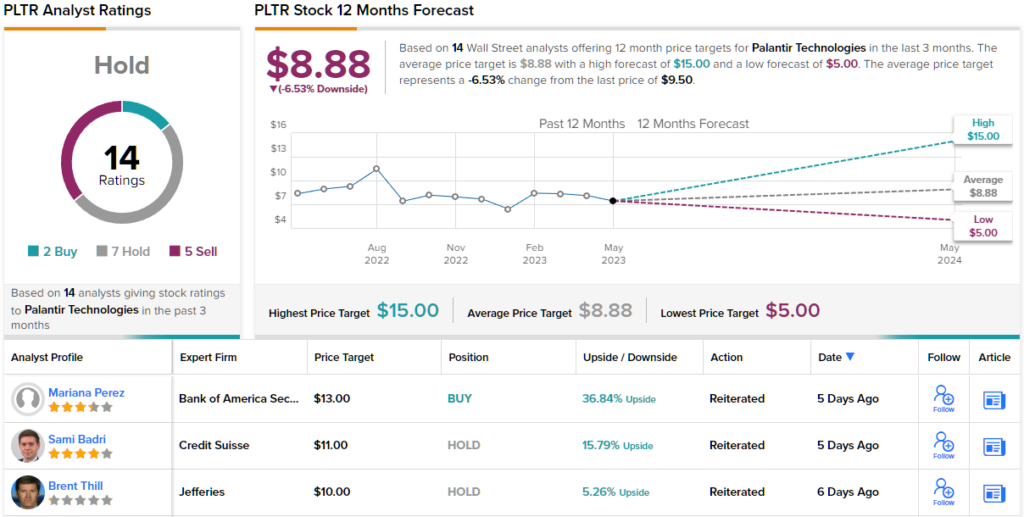

To this end, Borges rates PLTR shares a Neutral, while her $9 price target suggests the shares will decline by 5% over the coming months. (To watch Borges’ track record, click here)

Overall, PLTR gets mixed reviews from the rest of the Street. The stock claims a Hold consensus rating, based on 7 Holds, 2 Buys and 5 Sells. The analysts see shares falling by 6.5% in the year ahead, considering the average target stands at $8.88. (See PLTR stock forecast)

Coinbase Global (COIN)

Wood is a big fan of disruptors and that’s what you get with Coinbase, a company considered a disruptor of the financial industry. The leading cryptocurrency exchange enables users to buy, sell, and trade a variety of digital currencies and is one of the most popular and trusted exchanges in the industry.

Coinbase offers a user-friendly platform that makes it easy for individuals and institutions to get started in crypto and that has further accelerated adoption. Coinbase is also the only publicly listed cryptocurrency exchange in the US. In what marked a big deal in the mainstream adoption of cryptocurrencies, the firm went public in April 2021.

That, however, turned out to be some very bad timing. The listing coincided with the peak of the crypto bull market, and the company has suffered since. The shares are down by 82% since the first day of trading.

That said, the shares are up by 62% year-to-date, helped along by the recently released Q1 report. Although revenue fell by 33.4% year-over-year to $772.5 million, the figure came in ahead of the forecast by $119.2 million. Likewise on the bottom-line, EPS of -$0.34 fared a lot better than the -$1.36 anticipated on the Street.

In the meantime, Wood has been loading up. Since early March, she bought 1,546,296 shares via the ARKK ETF. These are currently worth over $88.6 million.

Evidently, Wood has high hopes for Coinbase, but that is not something that can currently be said about Goldman Sachs analyst Will Nance.

Looking at the latest set of results and outlook, Nance lays out the bear case: “Given the lack of visibility around organic growth and potential negative impacts from crypto regulation (and a pending lawsuit from the SEC following the recent Wells Notice), we remain negative on the outlook for shares. We believe renewed progress on retail crypto adoption and reduced uncertainty around the U.S. regulatory backdrop is likely necessary for shares to re-rate higher.”

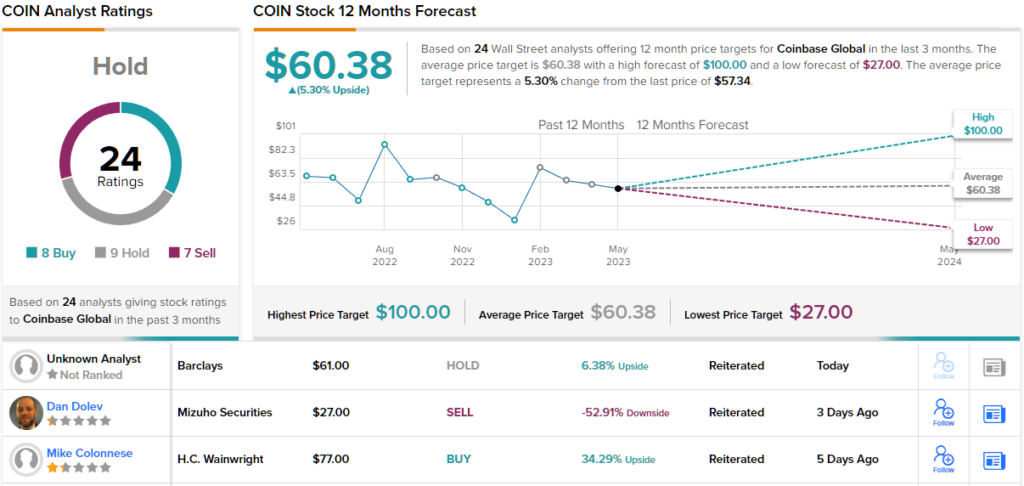

Accordingly, Nance rates COIN a Sell, and has a $45 price target for the shares. If it gets there, COIN stock could drop 21.5% gain from here over the course of the next year. (To watch Nance’s track record, click here)

The ratings for COIN on Wall Street span the entire spectrum quite evenly. The stock garners a Hold consensus rating, based on 8 Buys, 9 Holds and 7 Sells. Going by the $60.38 average target, the shares are expected to post modest gains of 5% over the coming year. (See Coinbase stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.