When people think of the auto industry, their minds often go straight to Detroit’s Motor City with its legendary muscle cars, or perhaps to Elon Musk and his sleek Tesla electrics. What doesn’t often come to mind is the network of auto dealers that moves the cars from the manufacturers’ lots to the customers’ driveways.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Yet, those dealers and retailers form a vital network, in every sense of the word. They handle sales, offer support, and manage logistics – all essential elements of car culture.

For investors, this network offers opportunities through the ‘Public 6,’ a group of large, publicly traded franchised auto retail companies.

Analyst Jeff Lick, in his recent coverage of the auto retail sector for Stephens, notes, “We believe the Public 6 generate a diverse stream of cash flows stemming from an essential need (transportation) and possess several competitive moats. The current stock setup is tricky due to an on-going earnings normalization from a COVID era boom… Longer term, we see the Public 6 as shareholder friendly businesses that are vital players in the transportation needs and preferences of U.S. and, for three of the six, international consumers.”

Lick sees these companies as ‘cash flow boosters,’ and he recommends two of them for investors to buy under current conditions. Do Lick’s picks sit well with the rest of Wall Street’s analyst community? This we can find out by also running these names through the TipRanks database. Let’s take a closer look.

AutoNation (AN)

We’ll start with AutoNation, a company that has been part of the US auto dealer scene since 1996. From its headquarters in Florida, the company operates more than 300 dealer locations, offering customers a comprehensive package of services: sales for new and used vehicles; financing when needed; and expert-level maintenance and repair services. The company’s goal is to make transportation services easy, transparent, and personalized to the customer’s needs.

AutoNation is one of the largest dealer franchise companies in the US and boasts a market cap of $6.6 billion. The company’s total sales reflect its size and reach—AutoNation was the first US dealer network to sell 8 million cars, a milestone it reached in 2011, and since its founding, it has sold more than 14 million vehicles.

The company’s business is split among four divisions: New and Used Vehicles; After Sales; and Customer Financial Services. New and Used Vehicles are the largest divisions, generating 47% and 29% of the company’s revenue, respectively.

That total revenue came to $6.5 billion in 2Q24, the last period reported. That figure was down 6% from the prior year and missed the forecast by $240 million. The company’s EPS also missed; at $3.99 per share, the non-GAAP earnings were 19 cents lower than expected.

Nevertheless, for Lick, AutoNation is the easy call for investors regarding the ‘Public 6’ dealers. He writes of the company, “We view AN as the most basic, least uncertain way for investors to gain exposure to the Public 6 dealership groups. We estimate only 5% of AN’s revenue has been acquired since 2019. 52% of AN stores are located in California, Texas and Florida with a heavy focus on major metro, high population locations. AN has remained focused on a U.S. centric, franchise dealership strategy. It has dipped its toe in the water with a used only (AutoNation USA) and captive finance company strategy, but both efforts are insignificant relative to the total operation at this time.”

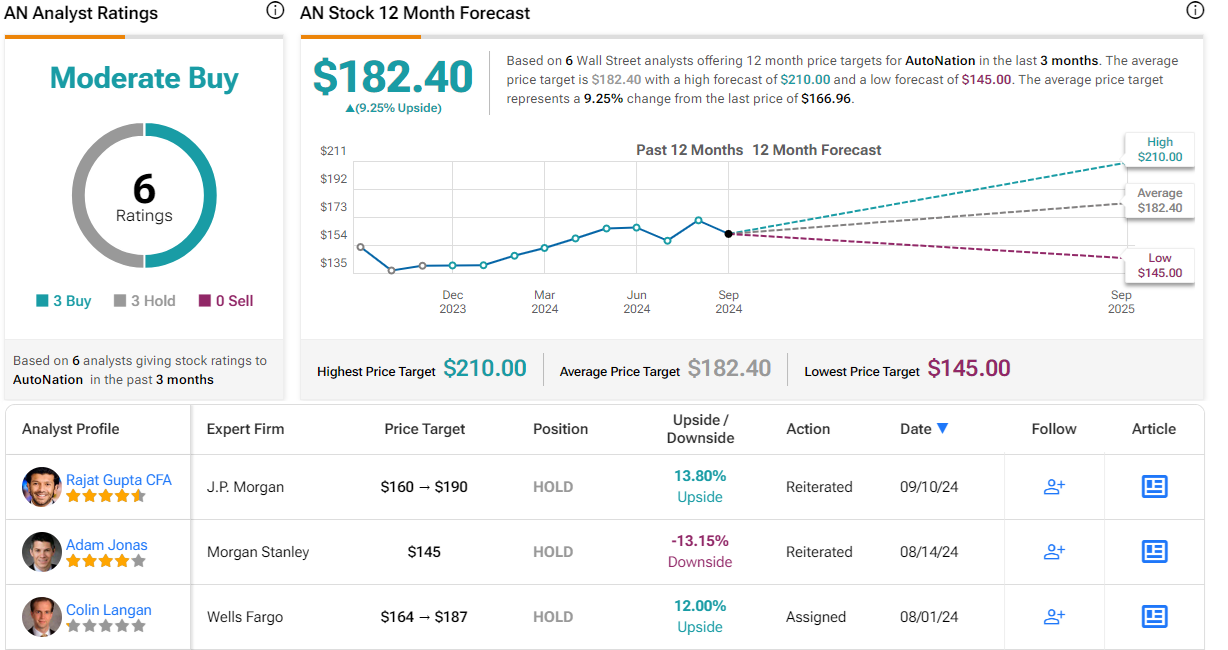

The analyst goes on to rate AN shares as Overweight (i.e. Buy), with a $210 price target that implies a one-year upside potential of 26%. (To watch Lick’s track record, click here)

This stock has a Moderate Buy consensus rating from the Street, based on an even split among the 6 recent reviews—3 each for Buy and Hold. The stock is priced at $166.96, and its average target price, $182.40, suggests a gain of 9% over the coming year. (See AutoNation stock forecast)

Lithia Motors (LAD)

Next up is Lithia Motors, another of the major auto dealer groups working in the US market. Lithia is a ~$7.5 billion company, with more than 460 dealer locations. These break down to 299 in the US, 15 in Canada, and 155 in the UK. Lithia deals in new cars, used cars, and certified used cars.

New cars make up the bulk of Lithia’s business. The company’s US dealer locations have a total of 66,228 new cars on the lots, backed up by more than 5,300 certified used vehicles and another 32,300+ used cars. The company’s large exposure to the used car market provides a distinct advantage, giving Lithia some protection against cycles and volatility in the new car market.

Looking at the company’s last set of financial results, which covered 2Q24, we find that Lithia had a top line of $9.2 billion. This grew year-over-year by almost 14%, although it did miss expectations by $80 million. The company’s non-GAAP EPS figure came to $7.87 and beat the forecast by 83 cents per share. The bulk of the company’s business came from new vehicle retail (47% of revenues) and used vehicle retail (32% of revenues). Lithia also offers a customer financing service, which saw its first profitable quarter, netting income of $7 million.

This company’s combination of scale and solid sales, and its strong growth plan, have analyst Lick taking a bullish stance on the stock. He says of Lithia, “In our view, LAD is the most ambitious, and therefore the most potentially volatile, of the Public 6 dealerships. LAD is also the largest of the Public 6 in terms of EBITDA at ~$1.6B. LAD is currently rolling out a captive finance business, which already accounts for over 10% of their total U.S. based vehicle sales. Similar to ABG, roughly 70% of LAD’s TTM revenues have been acquired in the last five years. Over the last 15 years, and certainly the last five, LAD has been the most aggressive and consistent acquirer of dealerships of the Public 6. Their track record as an integrator is impressive, in our view.”

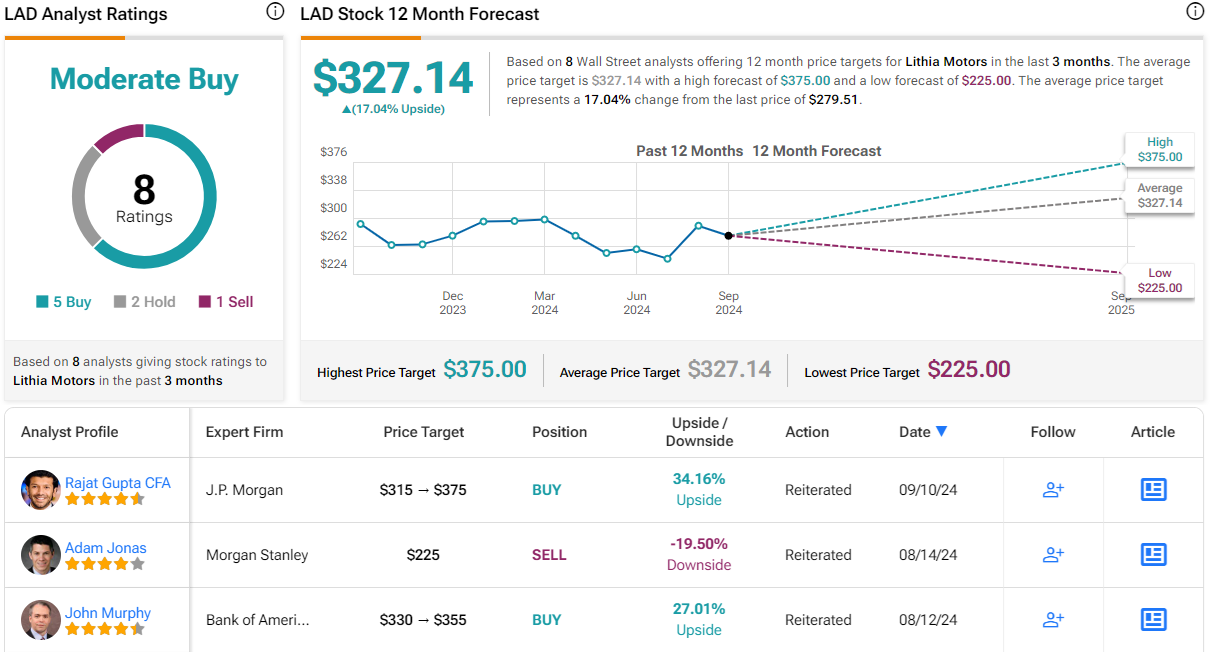

Lick complements this stance with an Overweight (i.e. Buy) rating and a $360 price target that points toward a one-year gain of 29%.

This is another stock with a Moderate Buy consensus rating from the Street’s analysts. Lithia has 8 recent reviews on file, and these include 5 to Buy, 2 to Hold, and 1 to Sell. The stock’s $279.51 share price and $327.14 average price target together imply a 17% upside in the next 12 months. (See Lithia stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.