Carvana (NYSE:CVNA), which operates an e-commerce platform for buying and selling used cars in the U.S., has seen its market value increase by a staggering 802% in the last 12 months. On the back of these gains, Carvana stock looks overvalued today despite the improving fundamentals. Carvana still enjoys a long runway to grow, but this expected growth seems priced in already. I am bearish on Carvana stock, as I believe the company’s valuation has detached from its economic reality.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Slowing Growth Is Compensated by Improving Profitability

In Fiscal 2023, Carvana’s revenue declined by 21% year-over-year to $10.77 billion. This decline in revenue does not come as a surprise, given that growth decelerated from 129% in 2021 to just 6% in 2022. However, in contrast to a company that is losing revenue because of macroeconomic developments out of its control, Carvana’s revenue losses are primarily stemming from its strategic decision to focus on profitable growth.

More than a year ago, the company pledged to focus on improving the unit economics of the business by growing the gross profit generated per used car sold (also known as gross profit per unit or GPU). In 2023, GPU reached $5,984, a notable improvement from around $2,000 in 2022. This eclipsed the previous high of around $4,600 registered in 2021 as well. Adjusted EBITDA per unit, which is a strong indicator of the company’s cash-flow generating ability, improved by more than $900 in 2023 as well.

In 2023, CVNA’s adjusted EBITDA margin improved to 3.1% from a negative 7.7% in 2022, highlighting the effectiveness of Carvana’s new strategy, which is centered around profitability targets.

This strategy involved a focus on reducing costs, enhancing the efficiency of the used vehicle purchasing process, employing sophisticated data analytics for pricing and credit risk evaluation, and maximizing the utilization of existing infrastructure to minimize additional capital outlays. These measures all played a part in improving the operational efficiency of the business last year.

Carvana seems to be enjoying certain competitive advantages stemming from its vertical integration efforts that enable the company to have greater control over the business process. Carvana manages all parts of the customer journey, including buying, reconditioning, selling, and financing used vehicles.

The Debt Problem Persists

In 2023, Carvana took decisive steps to reduce its debt burden. After initiating debt exchange offers with bondholders, the company successfully converted a portion of its unsecured debt into secured notes, thereby extending maturities and reducing total debt by approximately $1.3 billion. Even more importantly, the company was able to reduce its short-term interest expenditure by around $455 million for the next two years.

With a reduced short-term debt burden, Carvana can now afford to redirect its resources to other initiatives to maximize profitability and cash flows. These measures include improving the customer experience, which could likely turn out to be a differentiator between Carvana and its competitors.

The company, according to management, has eliminated $1.1 billion of annualized expenses since 2022 by reducing its headcount by more than 4,000 and using AI to streamline several business processes, including vehicle reconditioning.

Despite these positive developments on the debt reduction front, Carvana still carries $5.2 billion in long-term debt. If challenging macroeconomic conditions limit Carvana’s cash-flow generating ability this year, its debt problem will once again resurface, potentially deteriorating the investor sentiment toward the company.

According to Cox Automotive, in 2023, sales of used vehicles in the U.S. came in ahead of expectations and ended with a decline of 3% year-over-year. The continued shortage of new vehicle supply drove this outperformance, but the used vehicle market is expected to move toward normalcy, with easing chip shortages enabling auto manufacturers to double down on new vehicle launches.

If the used vehicle market softens this year, Carvana may face difficulties in growing retail sales, which, in turn, will negatively reflect on its adjusted EBITDA. Any hit to the expected cash flows this year – even if they prove to be temporary – will likely have a negative impact on its market value.

Valuation Comparison: Carvana vs. CarMax

Carvana is currently valued at a price-to-sales multiple of 0.82 compared to 0.43 for CarMax (NYSE:KMX), which is one of the most established players in the used car market in the United States. CarMax is a much larger business, with revenue of over $28 billion in the last 12 months. Even more importantly, CarMax has been consistently profitable in the last decade in complete contrast to Carvana, which is still trying to generate positive GAAP net income on a consistent basis.

While it’s true that Carvana has been growing at faster rates than CarMax, this valuation disparity between the two companies deserves scrutiny.

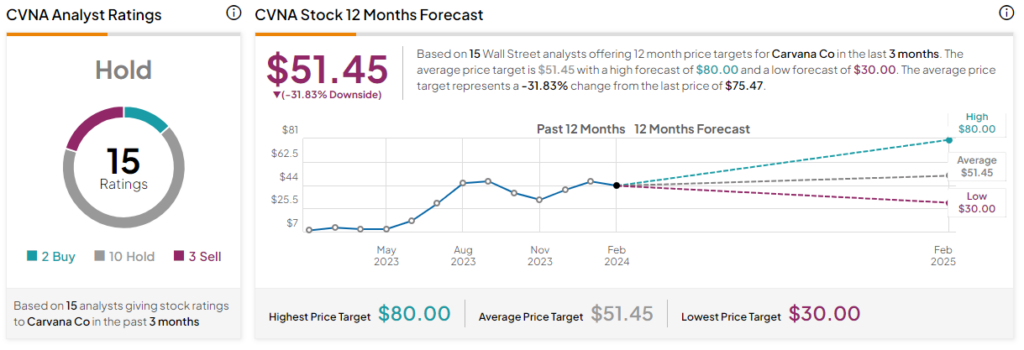

Is Carvana Stock a Buy, According to Analysts?

Earlier this month, Hedgeye listed Carvana as one of its top short ideas, citing 50% downside risk in the next 18 months. Hedgeye analyst Brian McGough believes Carvana’s highly leveraged balance sheet may bring about the downfall of the company at a time when the macroeconomic environment is proving to be challenging.

BTIG, in contrast, identified Carvana stock as a potential winner of a short squeeze opportunity a couple of weeks ago, with short interest rising to as much as 33% of the company’s float back then. After digesting the firm’s fourth-quarter earnings, Raymond James upgraded Carvana based on rosy expectations for adjusted EBITDA this year.

Overall, based on the ratings of 15 Wall Street analysts, the average Carvana stock price target is $51.45, which implies downside risk of 31.8% from the current market price.

The Takeaway: Carvana Is Too Risky Despite Recent Progress

Carvana made a strong comeback in 2023 with a fresh focus on profitability. In addition, the company successfully addressed bankruptcy concerns by restructuring some of its debt to extend maturities. While the recent progress deserves credit, Carvana seems expensively valued today on the back of a stellar stock market performance in the last 12 months.