Carvana Co. (CVNA), which operates an e-commerce platform facilitating used car sales in the U.S., is continuing to defy the odds by posting better-than-expected earnings despite challenging market conditions. Carvana stock is up almost 250% in the past 12 months as investors have rallied behind the company in response to this stellar financial performance. The company, which was feared to be headed toward bankruptcy in December 2022, turned a surprise profit of $48 million for the second quarter, or 14 cents per share, compared to Wall Street expectations for a loss of 12 cents per share. However, despite the blockbuster financial performance, I remain cautiously bullish on Carvana’s prospects. This caution is warranted because, while the company shows strong potential, I believe the valuation has become expensive.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Carvana Has Shifted to a Sustainable Growth Model

Building on the impressive financial performance mentioned earlier, Carvana’s recent strategic shift towards sustainable, profitable growth adds important context to my evaluation of the stock. Since Q4 2022, the company has moved away from a strategy of pursuing growth at any cost, opting instead for a focus on profitability and sustainability. As a result of this shift, Carvana has made significant investments in supply chain improvements, cost reductions, and debt restructuring, leading to a notable recovery. For example, the gross profit per unit has increased substantially from $3,368 in Q2 2022 to $7,344 in Q2 2024, reflecting the effectiveness of these new strategies.

Moreover, Carvana is projecting adjusted EBITDA of $1.1 billion for 2024, up from $339 million last year. To maintain this strong earnings growth momentum, the company is concentrating on several key areas. These include improving operational efficiency by keeping selling, general, and administrative costs flat while increasing unit sales, expanding production capacity to meet rising demand for used cars, investing in AI technology to enhance the customer experience, capturing a higher market share by focusing on customer convenience, and improving balance-sheet health through debt repurchase.

Nevertheless, despite these strong financial results and strategic advancements, I maintain some caution on my bullish stance on Carvana’s stock due to its high valuation. To justify this elevated valuation, Carvana must continue to achieve operational efficiencies and address several key areas.

Carvana’s High Valuation Shows Optimism and Risks

Carvana’s remarkable recovery has garnered significant attention in the market since early 2023. The company’s strong financial performance has been rewarded with a higher valuation compared to its competitors. Specifically, Carvana’s stock is currently valued at a price-to-sales (P/S) multiple of 1.32. In contrast, its peers such as CarMax, Inc. (KMX) and AutoNation, Inc. (AN) have lower P/S multiples of 0.42 and 0.26, respectively. This higher valuation reflects the market’s optimism about Carvana’s growth prospects.

However, this elevated valuation comes with its own set of risks. While Carvana is experiencing faster growth compared to traditional used car market players, the higher valuation means that the stock is priced for exceptional performance. As a result, any negative developments or downturns in the used car market could disproportionately impact Carvana’s stock price. This is because the stock is already priced based on high expectations of continued strong performance. If the company fails to meet these high expectations or if the market conditions deteriorate, the stock could experience more significant declines compared to its peers.

Carvana’s Has Several Growth Catalysts

Despite my caution regarding Carvana’s stock valuation, there are several bullish factors that still make the company an intriguing prospect. Carvana’s recent financial performance and strategic adjustments highlight its potential for continued growth. The strong performance in the used car market supports this optimism.

The used car market in the United States remains robust for a couple of key reasons. Firstly, leading automakers have significantly reduced their production targets for 2024, which has redirected buyers from new vehicles to the used car market. Secondly, lease volumes fell sharply during the pandemic years of 2020, 2021, and 2022, resulting in a historically low number of off-lease used cars available for sale today. As evidence of this strength, the Manheim Used Vehicle Value Index reached 201.6 in July. Although this is lower than the highs of over 250 seen in 2022, it remains well above the average index value of around 130 from 2008 to 2020. Elevated used car prices are expected to persist, potentially allowing Carvana to maintain high profit margins.

Furthermore, Carvana’s expansive national presence is a significant growth driver. Unlike traditional regional car dealers, Carvana has implemented a national strategy, aiming to dominate the market over the long term. Currently, Carvana covers approximately 82% of the American population by serving consumers in over 300 metropolitan areas. This extensive reach has enhanced Carvana’s brand visibility, enabling it to attract more customers without aggressive marketing expenses. Such scale contributes to enduring competitive advantages.

In addition to these factors, Carvana’s investments in technology underscore its long-term growth potential. The company’s focus on AI investments, development of an app-based inventory management system, and expansion of high-tech inspection and reconditioning centers are poised to give Carvana an edge over its competitors. These technological advancements are expected to drive efficiency and improve the customer experience, supporting the company’s ongoing market leadership.

While the company’s financial performance, market conditions, and strategic initiatives are impressive, the elevated stock price poses a risk.

Is Carvana a Buy, According to Wall Street Analysts?

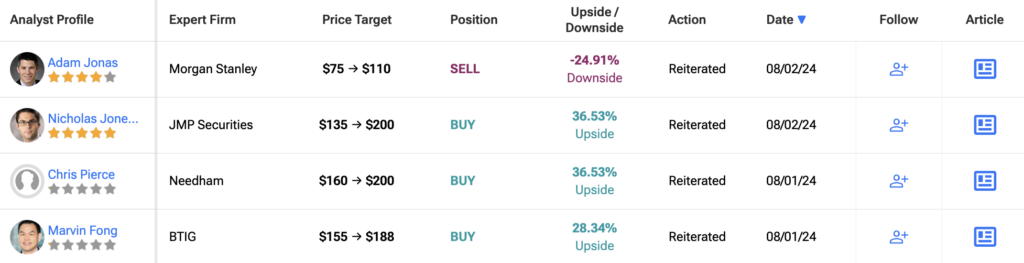

Given these strengths and the company’s overall strategic progress, it’s important to consider how Wall Street analysts are viewing Carvana’s prospects. Following its Q2 earnings report earlier this month, analysts have expressed notable optimism. Morgan Stanley analyst Adam Jonas, while not upgrading the stock, highlighted that the company has demonstrated strong operating leverage to achieve profitability for the first time in its history. JPMorgan analyst Rajat Gupta also believes Carvana is well-positioned for accelerated unit sales growth. After reviewing the Q2 earnings, Gupta raised his price target for Carvana to $185, significantly above the current market price of around $145.

Additionally, Oppenheimer analyst Brian Nagel expressed increasing optimism about Carvana’s future amid improving fundamentals. Following Carvana’s Q2 earnings, several other analysts have revised their price targets:

- Piper Sandler increased the price target by 44% to $151.

- DA Davidson increased the price target by 41% to $155.

- Wedbush Securities increased the price target by 25% to $150.

- Needham increased the price target by 25% to $200.

- RBC Capital increased the price target by 31% to $170.

These positive revisions have resulted in a notable increase in the consensus. Based on the ratings of 14 Wall Street analysts, the average Carvana price target is $163.83, which implies upside of 12% from the current market price.

The Takeaway: Carvana Excels as a Business, but Caution Is Advised

Carvana is proving to be one of the greatest turnaround stories in recent times, and investors have not been oblivious to the company’s success. Although Carvana is well-positioned to grow its share in the used vehicle market, the expensive valuation leaves little margin of safety for investors today. Wall Street analysts, however, believe Carvana stock still has more legs to move higher in the foreseeable future.