Duolingo (NASDAQ:DUOL) has everything a growth investor would want, except it also has a high valuation to keep things interesting. The educational app is branching beyond languages into subjects like math and music. Duolingo is riding on the tailwinds of innovations in education and can generate multi-bagger returns. It’s the go-to app for people who want an interactive way to learn a new language.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

I am bullish on Duolingo’s long-term prospects but am watching from the sidelines for now. A good dip or a better valuation may tempt me to initiate a position.

Strong Revenue and Earnings Growth

Duolingo is rapidly expanding and gaining market share. The company posted 43% year-over-year revenue growth in the third quarter and increased its bookings by a higher percentage. Total bookings were up 49% year-over-year, while subscription bookings increased by 54% year-over-year.

In another positive development, Duolingo flipped to profitability. The company reported net income of $2.8 million in the third quarter compared to an $18.4 million loss in the same period last year.

The switch to profitability is an exciting moment for growth investors. Many software companies that become profitable expand their margins rapidly. A higher net income reduces a stock’s P/E ratio and makes it more enticing for long-term investors.

Users continue to flock to the platform based on a 47% year-over-year increase in monthly active users. Additionally, daily active users went up by 63% year-over-year. These metrics indicate a financially robust company that is gaining more traction.

Valuation Concerns

Duolingo’s recent profits have resulted in a forward P/E ratio of 95x. It’s a lofty valuation that may scare away some investors. Some growth investors also consider a stock’s price-to-sales ratio. Its P/S ratio is currently 17.5, but it’s not the best metric for determining a stock’s value.

Duolingo doesn’t offer much of a margin of safety at its current price. While the stock has dropped by roughly 30% from its 52-week high of $245.87, it’s up 92% over the past year.

The educational app’s stock seems like a long-term buying opportunity for investors who have a five-to-10-year time horizon. The company has maintained 42-43% year-over-year revenue growth for several quarters, and profit margins should expand considerably this year. Further, a 115% year-over-year increase in net income indicates that valuation concerns can go away in a few quarters.

Expansion Into Multiple Subjects

Duolingo made a big announcement near the end of 2023 that expanded the company’s total addressable market. The company used Duocon 2023 as a platform to promote its multi-subject future. Less than a month after the conference, Duolingo launched math and music on its app.

The firm can expand into many subjects and reach more users in the process. Not everyone wants to learn a new language, but some people may use Duolingo in the future to learn about American History, science, math, and other core subjects.

Incorporating broader subjects complements Duolingo’s existing business model very well. Someone may decide to learn Spanish through Duolingo after going through some music lessons. Active users who are learning a new language may sharpen their skills in non-language subjects.

Duolingo is operating its enterprise in a profitable manner. The company has the resources to tap into more subjects and attract more users to its app. These investments can help Duolingo generate more revenue growth and attract new users when it reaches market saturation for people who want to learn new languages.

Giving people more things to do can also increase the number of daily active users. This user base saw higher year-over-year growth than monthly active users. Daily active users also help the company increase revenue and profits.

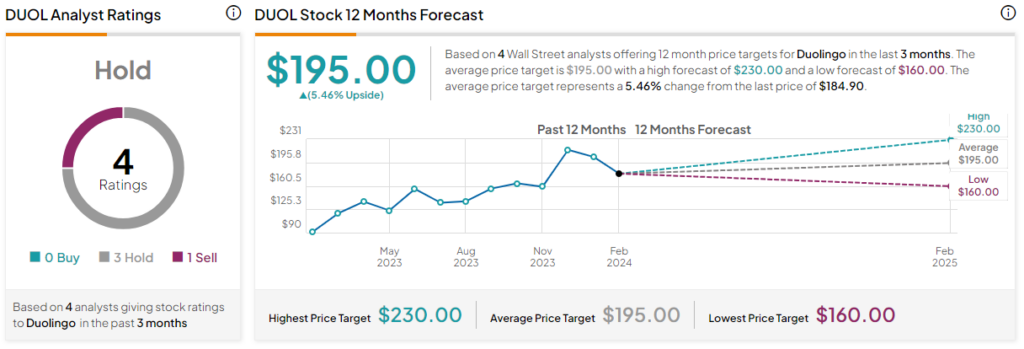

Is DUOL Stock a Buy, According to Analysts?

Duolingo is currently on hold, according to analysts, but it hasn’t had much coverage from analysts in the past three months. The stock has only been publicly traded since mid-2021 and has an $8 billion market cap. DUOL currently has four ratings, which include one Sell and three Holds, giving it a Hold consensus rating. That’s not the best group of ratings for a growth stock, but the average DUOL stock price target still suggests modest upside of 5.5%.

Two analysts gave no price targets and suggested that investors hold the stock. One hold came in with a $230 price target, while the analyst with a sell rating suggested a $160 price target. The higher price target suggests an upside of roughly 24%.

The Bottom Line on Duolingo Stock

Duolingo offers enticing growth prospects due to rising revenue, expanding profit margins, new subjects, and a growing user base. The stock checks a lot of the boxes that growth investors look for.

The only concern is the DUOL’s 95x forward P/E ratio. If the valuation was lower, the stock would be a compelling pick in the near term. However, it becomes more enticing if you have a five-to-10-year horizon for the investment. Therefore, Duolingo looks like a promising buy-the-dip opportunity overall.