At first glance, the troubles impacting the consumer economy appear to condemn casino and resort operator Caesars Entertainment (NASDAQ:CZR) to certain doom. However, given the sustained sentiment of revenge travel – the heightened desire to seek experiences denied during the pandemic – and strong overall demand for casino entertainment, top Wall Street analysts are giving Caesars a chance. These top analysts expect nearly 50% upside from the stock. Therefore, I’m cautiously bullish on CZR.

What are Top Analysts Saying about CZR Stock?

As stated above, top Wall Street analysts are bullish on CZR stock. In fact, the stock has a Strong Buy consensus rating based on six Buys and one Hold rating assigned by these analysts in the past three months. Also, the average CZR stock price target is $70, implying 48.6% upside potential.

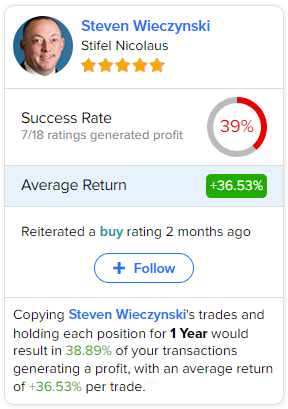

Five-star-rated Stifel Nicolaus analyst Steven Wieczynski is one of CZR’s bulls. He reiterated a Buy rating around two months ago, giving the stock a $74 price target, implying over 56% upside potential from here. He believes that the fundamentals of Vegas and regional casinos “remain solid with no signs of the consumer slowing.” He also expects free cash flow to be strong, which will help the company reduce its debt.

This is a notable rating because Wieczynski is the most profitable analyst (on a one-year time frame) covering the stock, as his CZR recommendations have returned an average of 36.53% each.

Risks and Rewards

Fundamentally, consumers still appear to gravitate toward experience-based expenditures, even amid rising pressures. Therefore, it’s possible that CZR stock may rise, as analysts expect, even through the middle of next year. However, it would be difficult to assess a longer-term view.

Financially, though, Caesars needs to show something positive for stakeholders. In the quarter ended June 2023, the company posted revenue of $1.58 billion. Unfortunately, this figure fell 44% against the year-ago tally of $2.82 billion. Thus, investors shouldn’t exclusively focus on the revenge travel narrative and analyst ratings while ignoring the financials.

The Takeaway: CZR Stock

Although Caesars presents a risky narrative due to the troubled consumer economy, top Wall Street analysts are optimistic about its chances. Since these analysts are known for their ability to generate solid returns through their recommendations, their influence carries greater weight. That said, you want to be careful about CZR stock because its “Strong Buy” thesis depends on a consumer phenomenon that can always fade unexpectedly. Therefore, I am bullish, albeit cautiously.