Say ‘electric vehicle’ these days, and Elon Musk is probably the first association that will come to mind. After all, he’s a headline machine – but his Tesla company has proven that the EV market can be profitable for automakers and investors alike.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But cars aren’t the only game in town for investors who want to buy into the EV sector, and worthwhile stocks don’t need to have Tesla-level prices. EVs are bringing a range of supporting technologies and infrastructure with them, from battery manufacturers to charging companies, and savvy investors can find affordable opportunities in that supportive network.

Today, we’ll look into the charging companies. While they may not exude the same appeal as the car makers, those cars won’t get very far without the charging infrastructure that their support companies will make available. In fact, the EV charging infrastructure market is expected to reach more than $207.5 billion by 2030.

We can get a taste of the opportunity here by looking at some of those pure-play charging stocks. Using the TipRanks platform, we’ve pinpointed two such names; each boasts a ‘Strong Buy’ rating from the analyst community, and offers plenty of upside potential. We’re talking more than 50% here.

Beam Global (BEEM)

The first stock we’ll look at is Beam Global, a company that works in clean energy products for EV charging. Beam has charging products in operation across 13 US states, in 96 cities. Chief among these products is the EV ARC, the first off-grid, permit-free, rapid-deployment EV charging system.

The system is designed for off-grid use, drawing power from its incorporated solar panels, and is sized to fit in or around standard parking spaces – any parking lot can become an EV charging spot. No major construction work is needed for deployment, and so no local zoning or permitting is required, either.

This past November, the company reported a quarterly record of $6.6 million in total revenue for Q3 of fiscal year 2022, for a 227% year-over-year increase. These gains were fueled by a series of recent wins the company has had in scoring new contracts, including a $29.4 million order from the US Army; an $11.6 million order from the Veterans Affairs Department; and a $5.3 million order from the City of New York.

In the weeks since the Q3 release, Beam has announced additional positive news, including, in January, contract order extensions with the State of California and the Federal Government totaling over $6.6 million. On a smaller scale, also in January, Beam received an order from Dallas County Texas worth $500,000 for 6 off-grid EV ARC systems.

A common factor in these new orders is the ability of the company to deploy the product quickly and put it into action with a minimum of fuss. That’s the main takeaway investors should understand about Beam, according to Northland analyst Abhishek Sinha.

“Rapid deploy ability & scalability, lower total cost of ownership, invulnerability to blackouts, being agnostic to an EV Charging company, having a patented solar tracking and storage solution altogether make BEEM’s products very differentiated versus what the market has to offer. Arguably, BEEM’s products are lot more expensive ($60K/unit) vs a normal Level 2 charger ($2-4K /unit). However, after factoring in the cost for construction work (digging, trenching, electrical set up) and electricity costs, BEEM’s products come out less expensive. In every instance where BEEM has deployed its units so far, the cost of its unit was less than the avoided cost of construction work that would have been required to deploy the chargers in the location where they have been deployed,” Sinha explained.

Summing up, Sinha wrote, “Given the recent rout in the EV Charging space, we believe BEEM offers a differentiated proposition and an attractive entry point.”

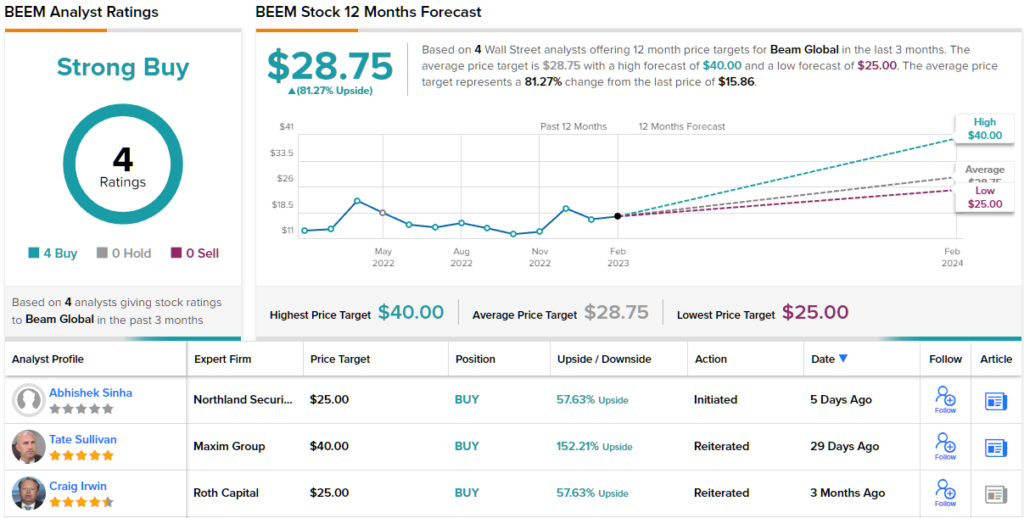

To this end, Sinha gives BEEM shares a $25 target price, suggesting a solid 58% upside potential over the next 12 months. His bullish target supports his Outperform (i.e. Buy) rating. (To watch Sinha’s track record, click here)

So, that’s Northland’s view, what does the rest of the Street make of BEEM’s prospects? All are on board, as it happens. The stock has a Strong Buy consensus rating, based on a unanimous 4 recent Buys. Moreover, the $28.75 average target, suggests shares have room for ~81% growth in the year ahead.

(See BEEM stock forecast)

Wallbox N.V. (WBX)

The next company we’ll look at, Spanish-based Wallbox, has created a set of smart and adaptable EV charging solutions. The company’s product line includes a range of chargers compatible with a wide variety of customer needs: commercial and residential, Type 1 and Type 2 vehicle charger connections. The residential charger installation models even have the added feature of bi-directional operability, allowing customers to discharge a fully charged EV’s power back into the home – or even onto the power grid.

Wallbox saw record revenues in its last reported quarter. In that report, for 3Q22, the company posted a top line of 44.1 million Euro (US$47.3 million), for a 140% increase year-over-year. The company’s gains were supported by several factors, including the sale of some 67,000 chargers – a total that was up 93% y/y.

In addition, Wallbox saw an increased footprint in the US market. The company started up the production lines at its new facility in Arlington, Texas during Q3, and saw revenue growth in the North American segment hit a whopping 535% for the quarter. Finally, Wallbox recorded the first orders for its new Hypernova 400 kilowatt DC fast charging station – and product designed specifically to meet the current subsidy requirements of the US government.

It’s interesting to note that the massive growth in EV charging – which is exemplified by Wallbox’s North American results – presents an opportunity for merger and acquisition activity in this sector. EV charger companies, large and small, will be looking to increase scale and expand product portfolios to meet an insatiable consumer demand – and M&A, if the money is available, is a quick path to that end. The recent acquisition of Volta by Shell, for $169 million in cash, is a good example, as it makes Volta’s network of charging stations with on-site advertising available for Shell to expand upon.

In fact, Canaccord analyst George Gianarikas sees the desire of larger firms to expand through the exploitation of smaller firms – by lucrative contract arrangements or M&A – as a net positive for Wallbox, and predicts that the company will build on its relationship with BP.

“We see the strategic focus on EV charging as positive for Wallbox as the company remains a prime asset given its differentiated and best-in-class products suite… In addition to U.S. NEVI opportunities, we believe this BP contract remains a strong tailwind for Wallbox over the next several years,” Gianarikas opined.

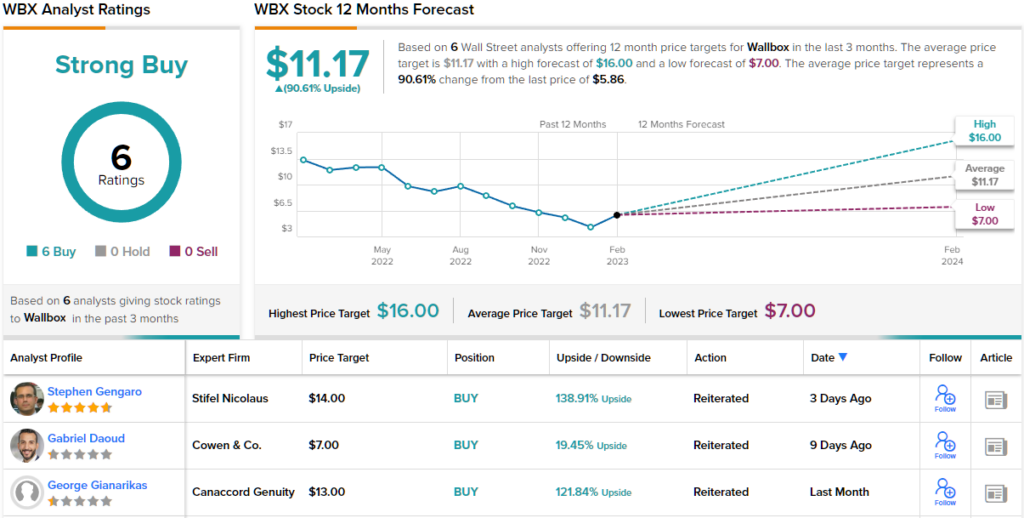

These comments provide solid support for Gianarikas’ Buy rating on WBX stock, and his $13 price target implies a one-year upside potential of 122%. (To watch Gianarikas’ track record, click here)

Are other analysts in agreement? They are. Only Buy ratings, 6 to be exact, have been issued in the last three months. Therefore, the message is clear: WBX is a Strong Buy. The stock is priced at $5.86 and its $11.17 average price target indicates room for ~91% growth ahead. (See WBX stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.