The price of oil has been volatile in the past 12 months. WTI, the US benchmark price, peaked above $90 at the end of September and fell just below $70 in December. Currently, it’s at $82 per barrel, a high price that is a boon to an industry that is also generating record-level production. The IEA is predicting that, by 2030, crude oil production in the US will increase by 2.1 million barrels per day over last year’s baseline.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Additionally, the high-demand environment for energy, especially as the summer driving season intensifies, creates a favorable scenario for investing in energy stocks. Share prices have declined alongside the dip in crude oil prices, presenting investors with an opportunity to buy into a sector with attractive valuations and solid near-term prospects.

This has Stephens analyst Michael Scialla recommending energy stocks. He’s forecasting solid upside potential, up to ~46% in one case, for two names in particular. We’ve used the TipRanks platform to look up the broader take on Scialla’s picks. Here they are, along with the analyst’s comments.

SM Energy Company (SM)

The first stock on our list is SM Energy, an independent exploration and production firm in the oil and gas sector. This firm, based in Denver, Colorado, traces its roots back more than a century and focuses on the acquisition and development of high-quality energy assets across the ‘lower 48.’ Currently, SM’s main operational assets are in Texas, where the company holds a net-acre position of ~111,000 in the famous Midland Basin in the western part of the state and another ~155,000 net acres in the Eagle Ford and Austin Chalk formations to the south. SM’s assets include crude oil, natural gas, and natural gas liquids.

Compared to its peers, SM’s holdings are not the largest – but the company has focused on acquiring top-tier assets, with the aim of maximizing value through applying the latest in hydrocarbon extraction technologies. The company had 1,323 net producing wells at the end of 2023, generating 152 Mboe/d in average net production. SM’s proven reserves, as of the end of last year, came to approximately 605 MMBoe. These reserves broke down to 38% crude oil, 42% natural gas, and 20% natural gas liquids.

In its last quarterly results, reported for 1Q24, SM reported a total top line of $559.9 million. This was down 2.4% year-over-year, but it beat the forecast by just over $3.2 million. At the bottom line, the company’s non-GAAP earnings came to $1.41 per share. Not only did this beat expectations by 13 cents per share, it was up from the $1.33 reported in the prior-year quarter.

SM’s success in developing high-end production numbers from its assets was the trigger that caught analyst Scialla’s eye. The Stephens energy expert writes of this company, “An early mover in identifying and developing core assets in areas that industry previously deemed non-core, SM offers investors differentiated option value as it pushes the boundaries of resource plays in the Midland Basin and South Texas. SM’s Rockstar acreage in Howard County, which was believed to be located east of the Midland Basin core when the company acquired it in 2016 and 2017, has yielded some of the most prolific oil producers in the play over the past 5 years.”

The analyst goes on to outline this company’s potential for solid returns going forward, saying of it, “With ~40% of the production mix in the form of natural gas and more than 85% of next year’s projected output unhedged, SM has meaningful exposure to a potential rebound in 2025 natural gas prices. In addition, an under-leveraged balance sheet positions the company to ramp returns to investors, in our view.”

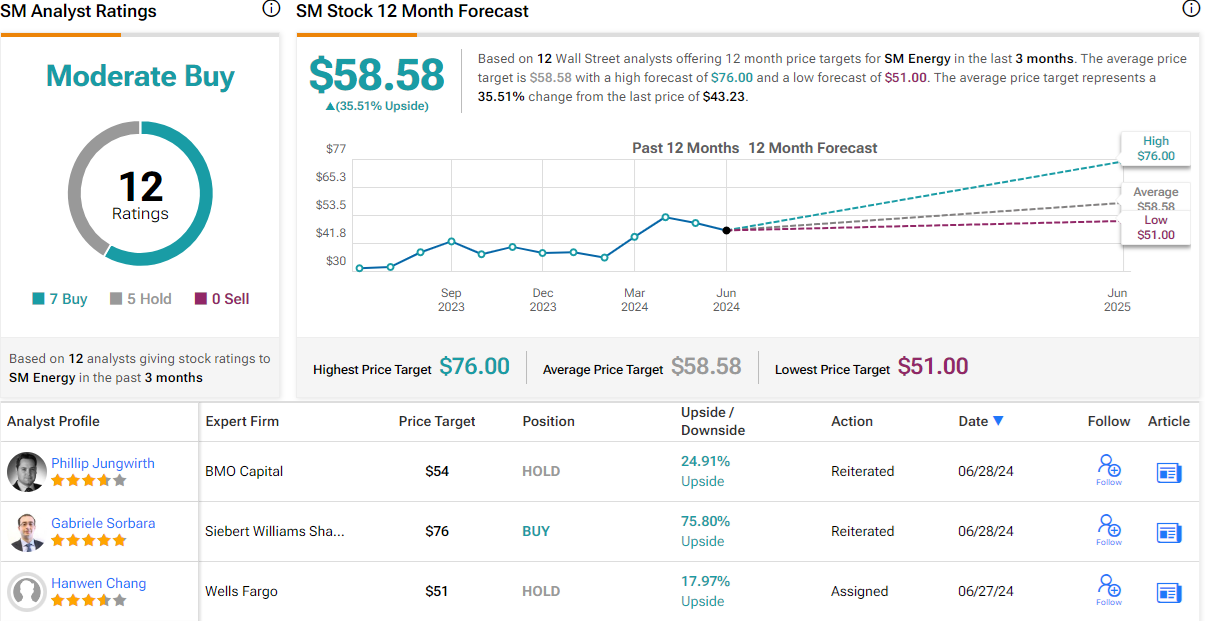

For Scialla, this stance backs up an Overweight (Buy) rating on SM, complemented by a $63 price target suggesting a 46% one-year upside potential. (To watch Scialla’s track record, click here)

Overall, SM Energy gets a Moderate Buy consensus rating from the Street, based on 12 recent analyst reviews that include 7 Buys and 5 Holds. The shares are priced at $43.23 and their $58.58 average target price implies a gain of 35.5% in the next 12 months. (See SM stock forecast)

Matador Resources Company (MTDR)

The second company we’ll look at, Matador Resources, is another player in the oil and gas exploration and production sector. Matador acquires energy assets in the US, with a particular focus on oil and natural gas shale formations – the same formations that brought us the fracking revolution earlier this century – along with other unconventional energy plays. Currently, Matador has active operations in three main areas: the Wolfcamp and Bone Spring plays of the Delaware Basin straddling the New Mexico/West Texas border; the Eagle Ford shale of South Texas; and the Haynesville shale and Cotton Valley energy plays in the northwest of Louisiana.

As a business strategy, Matador has focused on unconventional energy plays, using high-efficiency methods to maximize the extraction of hydrocarbon resources from these assets. In addition to operational efficiencies, Matador follows disciplined financial practices to maintain a strong balance sheet to ensure that both equity and debt capital serve the larger purpose of cost-efficient operations.

Matador’s operational execution exceeded the high end of guidance in the company’s 1Q24 report. Total production was reported as 149,760 Boe per day, compared to the top-end guidance number of 146,500 Boe/d. Of this, 84,777 barrels per day was oil production, and 389.9 MMcf per day was natural gas. The guidance numbers for oil and gas were 84,000 and 375 at the top ends.

Beating the forecast on production led to beating the forecast on revenues and earnings. Matador’s top line came to $787.7 million, more than $46 million over the estimates – and more than 40% better than the year-ago figure. Matador reported a non-GAAP earnings-per-share of $1.71, up from $1.50 in 1Q23 and 18 cents per share over expectations.

Scialla, in his coverage of Matador, is appreciative of the company’s strategy, particularly how it targets robust production from a low cost of operations. He says, “A pioneer in the Northern Delaware Basin, MTDR offers investors differentiated organic growth from a robust, low-cost drilling inventory. We forecast 2024 organic production growth of 19% y/y versus our midcap peer average of 3%. The company’s ‘brick-by-brick’ approach to building its land position is a core tenet of its value proposition and contributes to its strong margins. MTDR’s 2024 CF/Boe and FCF/Boe estimates are among the best in our mid-cap peer group.”

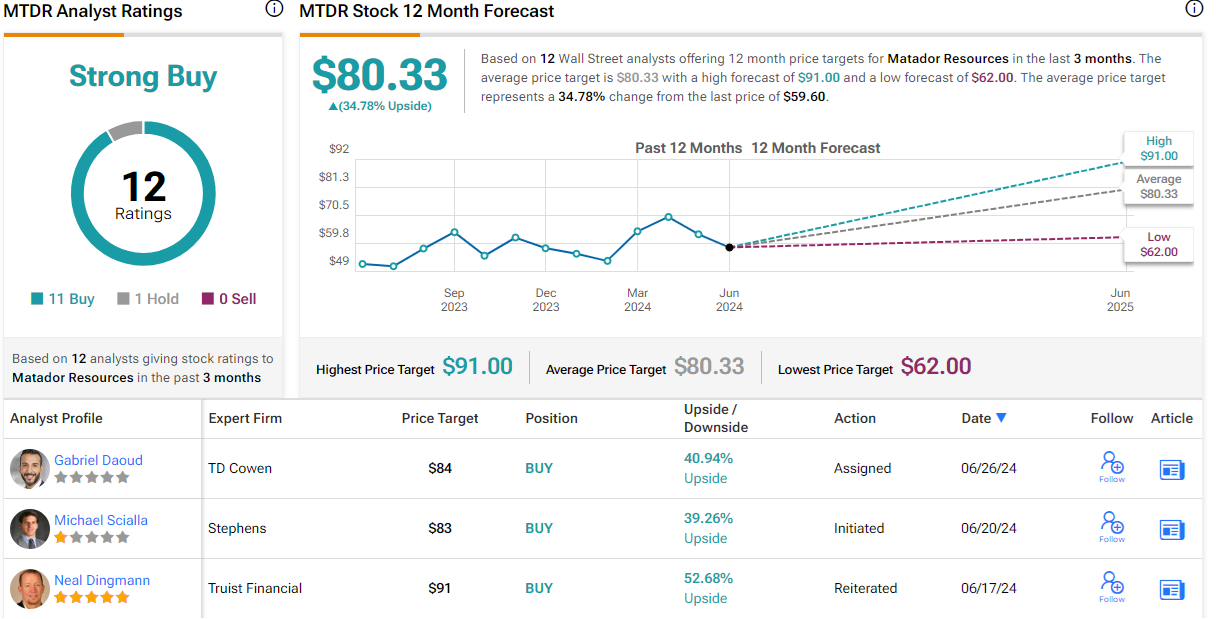

Based on this stance, Scialla rates MTDR as Overweight (i.e. Buy). He sets a price target of $83, showing his confidence in a 39% upside for the year ahead.

Matador’s dozen recent analyst ratings include 11 to Buy and 1 to Hold, for a Strong Buy consensus rating. The shares are priced at $59.60 and their $80.33 average price target implies that the stock has a one-year gain of 35% in store. (See MTDR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.