The Federal Reserve might have completed its round of rate hikes, based on recent statements made by the agency’s officials. Those statements conveyed the message that there is presently no urgent necessity to push the Fed funds rate beyond its existing range of 5.25 to 5.50% – the highest level since July 2001.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

A number of Fed officials pointed to the surge in government bond yields as a sign that the economy is slowing down sufficiently to curb inflation without necessitating further intervention from the Fed.

“I actually don’t think we need to increase rates any more,” Atlanta Fed President Raphael Bostic opined. “I think we are at a good place in that regard.”

If that is the case, that could be good news for the stock market, and the task for investors is to identify the stocks worth leaning into in this setting. But which strategy can help investors find the stocks poised to blast off on an upward trajectory? One approach is to sift through stocks that have received recommendations from analysts at prominent financial institutions, such as the financial powerhouse, Goldman Sachs.

The analysts at the banking giant see an opportunity in two names that have recently experienced a downturn but are expected to have better days ahead, with a potential upside of up to 130%. For a fuller picture of their prospects, we also ran these names via the TipRanks database. Here are the details.

Geron Corporation (GERN)

Let’s first head to the biotech space and take a look at Geron, a late-stage clinical biopharma company primarily focused on developing innovative therapeutics for the treatment of blood cancers. Geron has gained significant attention and recognition for its pioneering work in the field of telomere biology. Researchers at Geron introduced an innovative method involving oligonucleotides, which are brief, synthetic DNA or RNA strands, to impede the functioning of telomerase, an enzyme responsible for preserving telomeres and facilitating the ongoing growth of cancerous cells.

Investors seeking opportunities in biotech know that it’s all about upcoming catalysts, and Geron has a big one coming up next year.

The company’s flagship product candidate is imetelstat, a telomerase inhibitor that has shown promise in clinical trials for hematologic malignancies, such as myelodysplastic syndromes and myelofibrosis. Following encouraging Phase 3 results for the study targeting transfusion-dependent anemia in patients with lower-risk myelodysplastic syndromes (MDS), the company’s marketing application for imetelstat has been accepted by the FDA, and a PDUFA date has been set for June 16, 2024.

The shares, however, have been on the decline in recent times, falling by ~53% since June’s yearly high. This decline has occurred in the backdrop of another development – the recent FDA approval for the label expansion of Reblozyl, advanced by Bristol Myers Squibb and Merck as a first-line option for anemia in adults with MDS.

Nevertheless, Goldman Sachs analyst Corinne Jenkins does not see this factor impeding imetelstat’s success. She claims that investors should seize the opportunity now that shares are at such a low level.

“Based on our review of the data, conversations with KOLs, and regulatory precedent, we maintain our view that imetelstat is likely to be approved in this setting, where we estimate $1.5B in unadjusted peak sales (PoS: 90%),” Jenkins said. “Further, the recent approval of Reblozyl in frontline LR-MDS across a broad population (RS+/-) does not negate the blockbuster opportunity for imetelstat in the second-line setting, in our view. Thus, we see the recent pullback in shares as presenting a buying opportunity for the stock.”

These comments underpin Jenkins’ Buy rating while her $4 price target makes room for big upside of ~130% in the year ahead. (To watch Jenkins’ track record, click here)

It looks like all other analysts feel the same way. The stock claims a Strong Buy consensus rating, based on a unanimous 5 Buys. Moreover, the $4.80 average target is even more bullish than Jenkins will allow and set to generate 12-month returns of ~173%. (See GERN stock forecast)

Shoals Technologies Group (SHLS)

Let’s pivot now to the solar sector and get the lowdown on Shoals Technologies, a company specializing in advanced electrical balance of systems (EBOS) solutions for the solar and renewable energy industry. Since being founded in 1996, Shoals has emerged as a global leader in the design, manufacture, and deployment of critical components and systems that help maximize the efficiency and reliability of solar power generation. The company’s product portfolio includes a wide range of combiner boxes, junction boxes, and other electrical solutions that play a pivotal role in connecting and managing the various components of solar arrays.

Shoals Technologies has experienced significant growth and expansion over the years, capitalizing on the rising demand for clean energy solutions. That was certainly the case in the latest earnings report, for 2Q23. Revenue climbed by 62.2% year-over-year to $119.21 million, in turn beating the consensus estimate by $3.8 million. Likewise, on the bottom-line, adj. EPS of $0.14 edged ahead of expectations by $0.01.

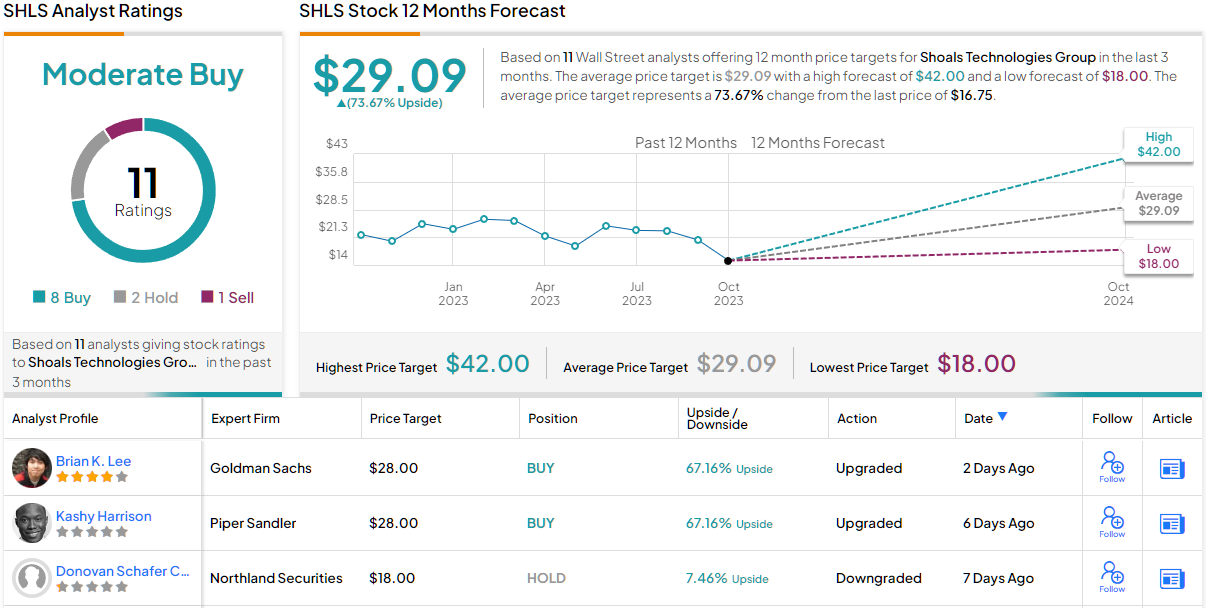

Nevertheless, despite these results and even accounting for a recent recovery, SHLS shares are down by 43% since the early year peak. However, Brian Lee Goldman analyst identifies reasons for the drop and sees other signs that point to a continued recovery.

“Looking ahead,” says Lee, “we’re tactically more bullish given (i) overhang from recent warranty expense issues appear to be priced in and we now see margin upside risk skewed to the upside, and (ii) US utility scale solar fundamentals remain among the best in our solar coverage group and we still see multiple catalysts on the horizon heading into what should be a robust 2024 growth backdrop. With SHLS trading at ~20X NTM P/E, valuation is at historical lows and we see risk-reward as hard to ignore, despite some of the idiosyncratic and macro challenges that have weighed on the stock, of late.”

Quantifying his stance, Lee rates SHLS a Buy to go alongside a $28 price target. The implication for investors? Upside of 67% from current levels. (To watch Lee’s track record, click here)

The majority of Wall Street analysts agree with Lee’s take although not all are on board. Based on a mix of 7 Buys, 3 Holds and 1 Sell, the stock receives a Moderate Buy consensus rating. Going by the $29 average target, in 12 months’ time, investors will be sitting on gains of 73%. (See SHLS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.