Boeing (BA) stock has suffered in 2024 as high-profile safety incidents relating to its civil aviation operations compounded prior concerns about build quality and safety mechanisms. However, the company’s misery has now extended to include thousands of striking workers demanding higher pay and benefits. Meanwhile, the company’s debt position is worsening by the day. Despite positive earnings forecasts for 2025, I’m bearish on Boeing.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Boeing Worker Pay Demands

As most investors and members of the general public will know, it’s been tough sledding for Boeing in recent years. Amid continued quality concerns and delivery delays, Boeing’s ongoing labor dispute has reached a critical juncture. The company recently presented its “best and final offer” to striking workers, but the effort appears to be in vain. Every week there seems to be a new reason to be pessimistic on Boeing.

The recent proposal included a 30% pay raise over four years, up from the previous 25% offer. It also promised a doubling of the ratification bonus to $6,000. However, the International Association of Machinists and Aerospace Workers (IAM) has rejected Boeing’s ultimatum, refusing to hold a vote by the company’s September 27 deadline. Representatives of the striking workers earlier claimed that the proposal was made absent negotiation with the union.

The strike, involving 33,000 workers, has halted production of several aircraft models and is costing Boeing a large sum each day. According to the union, key issues remain unresolved, including the restoration of a traditional pension plan eliminated a decade ago.

A Review of Boeing’s Quality Issues

As the standoff continues, the union and Boeing face mounting pressure. Boeing has implemented cost-cutting measures including furloughs for non-union employees, while striking workers risk losing their company-provided health insurance by the end of the month.

However, these strikes and layoffs seem likely to only compound production and quality issues. In recent years, the company has faced criticism for prioritizing production speed over quality, with workers reporting inadequate training and pressure to cut corners. A six-week FAA audit revealed serious production issues, including improper documentation, insufficient quality inspections, and the use of unauthorized tools.

These problems led to incidents such as the door plug detachment on an Alaska Airlines (ALK) flight in January 2024. Recent incidents have also included the LATAM Airlines 787 mid-air drop in March 2024, and the engine loss incident on a Southwest Airlines 737-800 flight in April 2024. All of these compound the fallout from the deadly accidents from 2018 and 2019. With mounting quality concerns, mitigation efforts had already resulted in delivery delays.

Is Debt a Concern for Boeing?

Issues keep compounding for Boeing, and its growing debt pile is one of these. As of the second quarter of 2024, the company’s long-term debt jumped back above $50 billion recently, after several quarters in the $47 billion – $48 billion range. This increase was due to the issuance of new debt. Some investors have floated concerns about the company’s financial stability.

Moreover, Boeing’s bonds are trading near junk level and are at risk of losing their investment-grade status, which would cause higher yield spreads for the company. The company’s cash flow has also been negatively impacted, with operating cash flow landing at -$3.9 billion for the second quarter of 2024.

Should Investors Trust the Forecasts?

While I’m bearish due to all this headwinds, many analysts are forecasting a swift return to profitability. The current consensus estimates suggest that Boeing will achieve $3.44 of EPS profitability in 2025. That earnings level would imply that Boeing is trading at a forward P/E ratio of 44.2x. From there, analysts expect earnings will surge to $13.09 in 2027; a two-year forward P/E of just 7.26x.

Personally, I’m doubtful about the merits of these forecasts given the reputational damage Boeing has suffered, as well as a slower order book than its peer Airbus (EADSF). Airbus itself is suffering from production delays, but its problems seem to pale in comparison to the strife its American counterpart is going through.

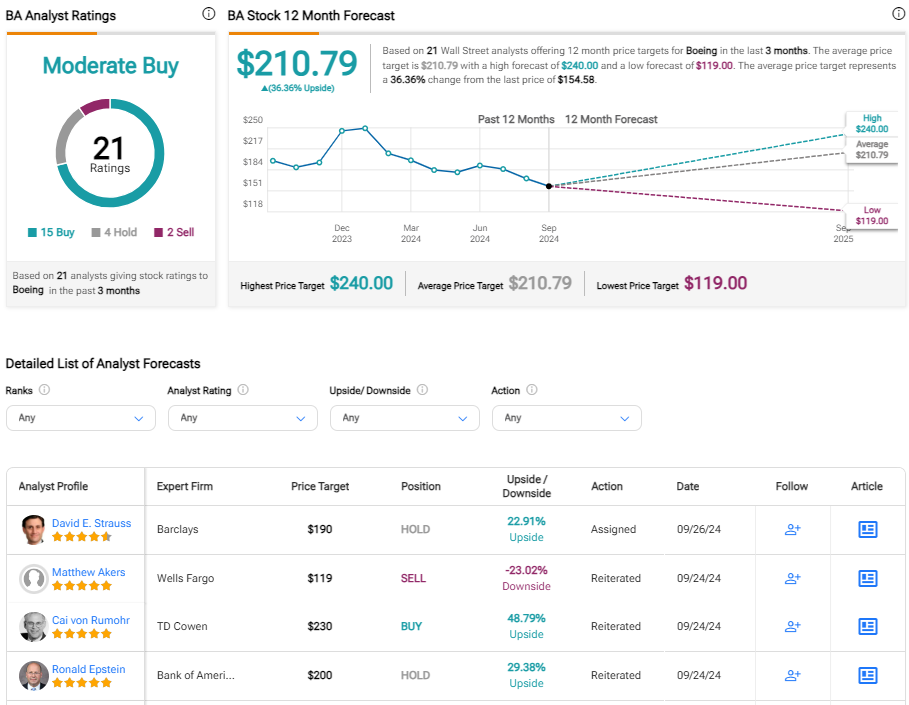

Is Boeing Stock a Buy According to Analysts?

On TipRanks, BA comes in as a Moderate Buy based on 15 Buys, four Holds, and two Sell ratings assigned by Wall Street analysts in the past three months. The average Boeing stock price target is $210.79, implying a ~35% potential upside. The majority of analysts are expecting BA stock to rebound above $200 per share over the next year.

The Bottom Line on Boeing Stock

I recognize that Boeing trades far below its average share price target, but BA stock is not an investment for those with an uneasy stomach. Quality concerns, pay issues, and a worsening debt position all contribute to my skepticism over whether the company can regain its footing anytime soon. For me, there’s simply too much risk and potential downside from investing in BA shares. I don’t want to be an owner here, despite the high barriers to entry in the industries in which it operates.