We’ve seen the markets take a breather recently and that is hardly surprising considering the year-to-date rally. Stocks charged out the gate in 2023 as if in a hurry to consign 2022’s annus horribilis to the history bins.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Observing the sharp and abrupt shift in sentiment, BlackRock’s bond chief Rick Rieder has called the surge “extraordinary.” However, Rieder, who handles around $2.4 trillion in assets, is not quite ready to get the bull outfit on just yet.

Given the widespread compression in profit margins, equities are generally “just ok” and that is why Rieder says he would “rather buy income — both debt and equity — I’d rather buy stable income much more so.” Even getting more specific, Reider would plump for companies with “quality income.”

That’s just not BlackRock talk. Walking the walk, the investment giant has more than a 7% stake in two names that offer just that; stocks showing a strong profitability profile, making them ideal names to own whatever the macro backdrop. We’ve opened the TipRanks database to also see how these names fare amongst the Street’s stock experts. Here’s the lowdown.

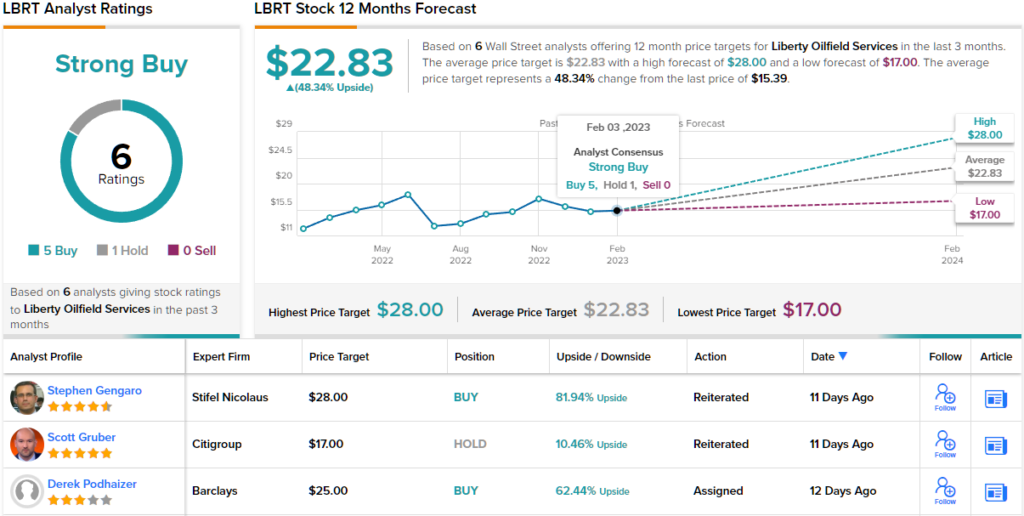

Liberty Energy Inc. (LBRT)

Stocks got slammed in 2022, that is already well-established, but not all got beaten to a pulp. The energy sector was one of the few to make hay and you can add Liberty Oilfield Services to the list of stocks that outperformed – the shares gained 65% over the course of the year.

Liberty is a North American oilfield services company that provides onshore oil and natural gas exploration and production companies with what it terms “innovative suites” of completion services and technologies. It offers high-quality hydraulic fracturing, engineering, and wireline services; in a nutshell, Liberty is a pure-play pressure pumping firm.

And that value proposition has served it well in recent times as was evident in the company’s latest quarterly report for 4Q22. Revenue increased by 78.4% year-over-year to $1.22 billion. Net income reached $153 million, improving on the $147 million generated in Q3. The result was fully diluted earnings per share of $0.82 and that led to a record fully diluted earnings per share of $2.11 for the full year.

In further pleasing news, the company raised its existing share repurchase authorization to $500 million, an increase from the $250 million originally authorized when the program began in July.

With the profitability profile established, turning to Blackrock’s involvement, the fund giant currently owns 13,292,031 shares, amounting to a 7.3% stake in LBRT, and worth over $203 million at the current share price.

Weighing in from Stifel, 5-star analyst Stephen Gengaro highlights the various reasons investors should get behind this stock with a ‘compelling valuation.’

“We believe rising U.S. completion activity in 2023 coupled with tight pressure pumping supply and demand fundamentals support strong growth for LBRT. We expect rising profitability, strong FCF, and an increase in cash returns to shareholders as LBRT executes its buyback program and distributes dividends. We believe the shares offer a compelling risk/reward trading at only 2.3x estimated 2023 EBITDA,” Gengaro opined.

Gengaro isn’t just predicting a strong future, he’s backing his stance with a Buy rating and a $28 price target that makes room for 12-month gains of a handsome 82%. (To watch Gengaro’s track record, click here)

Most on the Street agree with that thesis; barring one fence sitter, all 5 other recent analyst reviews are positive, making the consensus view here a Strong Buy. (See LBRT stock forecast)

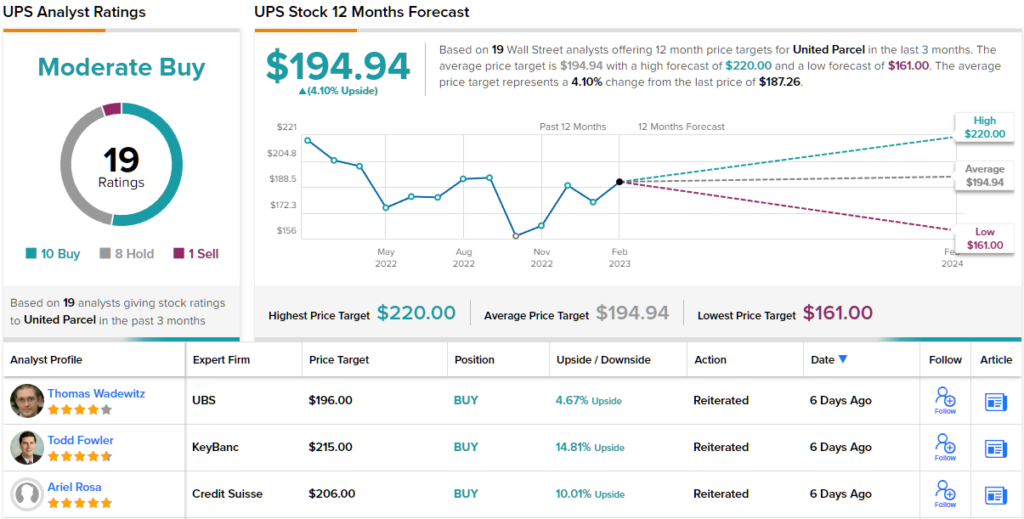

United Parcel Service (UPS)

We’ll now switch gears and move over to UPS, one of the world’s largest shipping couriers. With a footprint in 220 countries and territories and a workforce of ~500,000 people offering a wide range of logistics solutions for its customers, the delivery giant’s revenue haul topped $100 billion in 2022.

However, in Q4, a 2.7% year-over-year drop to $27 billion saw the topline come in $1.03 billion short of consensus expectations. At 27.9 million, average daily package volume also came in below the 28.2 million anticipated, while total package volume for the quarter reached 1.76 billion, missing the Street’s 1.78 billion forecast.

Nevertheless, the company remains solidly profitable, as adj. EPS came in at $3.62, trumping the Street’s call for $3.59. Cash from operations clocked in at $14.1 billion and free cash flow reached $9.0 billion.

For 2023, the company anticipates revenue will be in the range between $97 billion and $99.4 billion and sees consolidated adjusted operating margin hitting the range between 12.8% to 13.6%.

And for the 14th year in a row, the Board approved a raise to the company’s quarterly dividend. With a 6.6% increase, UPS will pay a first-quarter 2023 dividend of $1.62, which will generate a yield of 3.4%. Furthermore, the Board also gave the green light for a new $5 billion share repurchase authorization, succeeding the existing authorization.

Blackrock comes into the picture here with 7.9% ownership. This translates to a holding of 57,900,388 shares. Right now, these are worth just under a whopping $11 billion.

For Deutsche Bank analyst Amit Mehrotra, the UPS bull case is based on the company making all the right moves. Explaining his stance, Mehrotra writes: “With respect to 2023 estimates, we think the disclosures triangulate to EPS of about $11.60 per share versus consensus of about $12 per share. But we note this reflects over $900 million of below the line non-cash pension income headwinds in 2023, which we estimate is about 3x what was contemplated in consensus on a net basis. This is because UPS is reinvesting the entirety of above the line pension tailwinds ($420 million) into initiatives aimed at improving service, productivity and time in transit. This is exactly the right strategy to drive sustainable value creation, in our view, and it’s remarkable that operating profits for 2023 are roughly in line with consensus despite this incremental investment.”

To this end, Mehrotra rates UPS shares a Buy along with a $220 price target, which implies ~17% upside potential in the year ahead. (To watch Mehrotra’s track record, click here)

Overall, the consensus rating here is a Moderate Buy, based on 19 analyst reviews that include 10 Buys, 8 Holds, and a single Sell. (See UPS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.