With the macro backdrop currently a combination of debt ceiling negotiations, data pointing to cooling economic activity amidst expectations of a recession, investors could benefit from a guiding hand to block out the background noise and point toward the equities primed to gain from here.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

One way to keep ahead of the game is by riding the coattails of Wall Street investing legends. Ones such as Steve Cohen. Using a high-risk/high-reward strategy, the billionaire Chairman and CEO of global asset management firm Point72 has amassed a fortune estimated to be ~$17.5 billion, and as of the end of last year, the hedge fund boasted of $27.2 billion in assets under management.

So, when it comes to stock picking, keeping an eye on Cohen’s latest purchases is undoubtedly worthwhile.

We’ve done just that and, using the TipRanks database, we’ve pulled up the details on two new positions that recently made their debut in Cohen’s portfolio. What’s interesting is that Cohen isn’t the only one seeing potential in these stocks; both have earned a Strong Buy rating from the analyst consensus. Let’s take a closer look.

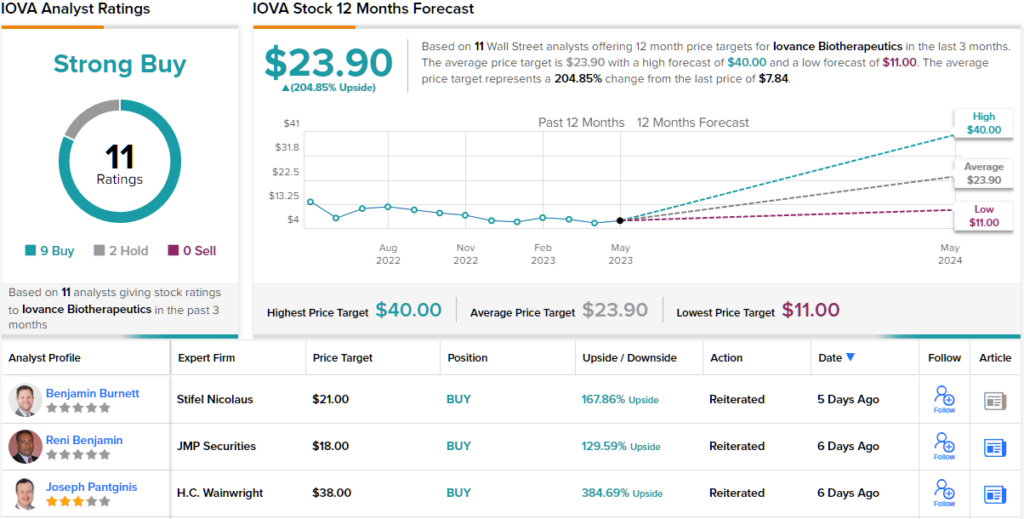

Iovance Biotherapeutics (IOVA)

A high-risk/high-reward strategy will naturally lead to the biotech sector; that’s where the first Cohen-backed stock we’ll look at belongs. Iovance Biotherapeutics is a clinical-stage biotech company focused on the development of novel cancer immunotherapies. They achieve this by developing personalized cell therapies using tumor-infiltrating lymphocytes (TILs), which are T-cells that migrate from the bloodstream into a patient’s tumor, where they recognize and attack cancer cells.

Iovance’s pipeline is led by Lifileucel, which is being tested in several programs, the most advanced of which is as a therapy for patients with advanced melanoma, specifically those who have failed anti-PD-1/L1 therapy and targeted therapy. In March, the company announced that it had completed the rolling Biologics License Application (BLA) submission to the FDA based on the positive clinical data from the C-144-01 clinical trial.

Cohen must think the drug’s chances of success are pretty high. He opened a new position in Q1 with the purchase of 8,800,059 IOVA shares. These are currently worth almost $69 million.

Given the FDA’s 60-day decision goal, Stifel analyst Benjamin Burnett anticipates an update regarding the BLA by the end of this month. Due to the fact that there are no approved treatments for melanoma in this setting, Burnett is confident in the outcome.

“Regulatory situations are inherently opaque, but we’re optimistic that the clinical data, which we think are good, especially when considering the setting, will be sufficient to support approval,” Burnett said. “We don’t have an edge on the potency assay controversy (the company had issues developing its potency testing), but we lean positive here based on mgmt’s portrayal of prior FDA discussions, and given that they have internal regulatory expertise.”

“We’re also optimistic into the launch as we think expectations are low, given precedence set by just about every other cell therapy launch, but as IOVA owns their own manufacturing facility, plans to onboard 40 treatment centers within a few months of approval, and has already established CMS pricing, we think the launch could set up favorably for the stock,” the analyst added.

How does this all translate to investors? Burnett rates IOVA shares a Buy and backed by a $21 price target. There’s potential upside of a hefty 168% from current levels. (To watch Burnett’s track record, click here)

Most on the Street back Burnett’s stance. The stock garners a Strong Buy consensus rating, based on 9 Buys vs. 2 Holds. Other analysts appear to think the stock is significantly undervalued, too; going by the $23.90 average price target, a year from now, investors could be pocketing gains of ~205%. (See IOVA stock forecast)

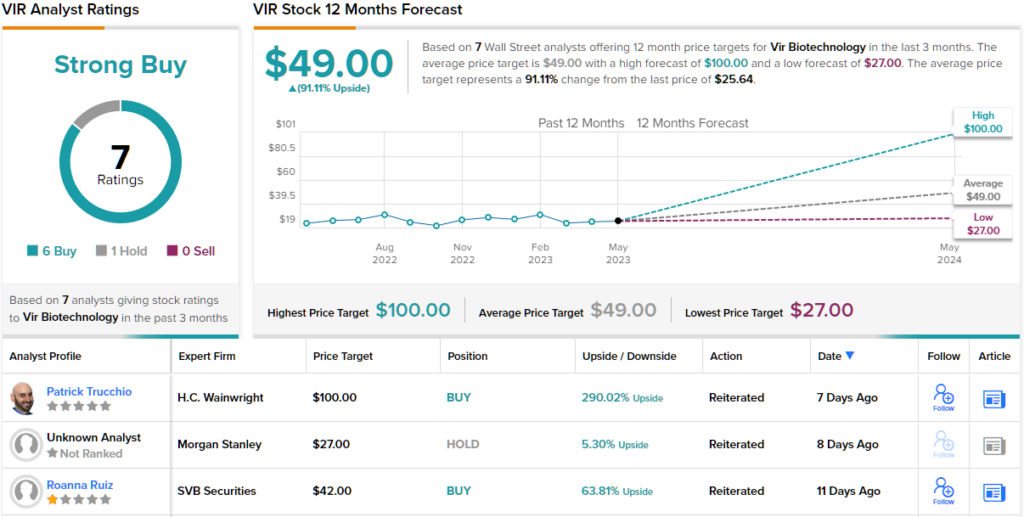

Vir Biotechnology (VIR)

Next up is Vir Biotechnology, a commercial-stage immunology company with the lofty aim of creating ‘a world without infectious diseases.’ It intends to achieve this by developing monoclonal antibodies and T-cell therapies designed to target specific pathogens and enhance the body’s immune response to them.

The company has a diverse pipeline of drug candidates that target a range of infectious diseases, including hepatitis B, influenza and HIV. And over the coming months, the company will report several important updates regarding the pipeline’s activity.

Data from the ongoing Phase 2 prevention of illness due to Influenza A (PENINSULA) study evaluating VIR-2482 is anticipated in mid-2023. This is the first Phase 2 outpatient study to assess the part a monoclonal antibody plays in the prevention of influenza A illness. Initial data from the Phase 1b trial assessing the safety of VIR-2482 in adults over 65 and receiving a flu vaccine are also anticipated half-way through the year.

From the Hepatitis B Virus (HBV) research path, multiple trials assessing the potential for VIR-2218 and VIR-3434 to attain a functional cure for chronic HBV are underway with data anticipated in 2023.

Additionally, in the second half of 2023, a data readout is expected from the Phase 2 SOLSTICE trial assessing VIR-2218 and VIR-3434 as monotherapy and in combination for the treatment of people living with chronic HDV (Hepatitis D Virus). This is the most aggressive type of viral hepatitis.

Cohen must fancy his chances here, too. During Q1, he bought 1,683,100 VIR shares, in what amounted to a new position. At the current share price, this purchase is now worth over $43.1 million.

Mirroring Cohen’s confidence, H.C. Wainwright analyst Patrick Trucchio lays out the bull-case: “With cash and investments of $2.3B more than sufficient to fund clinical trials through key Phase 2 readouts, we find VIR, our top pick for 2023, to be highly attractive ahead of the next expected readouts, particularly in CHB and flu… Not risk-adjusted, we estimate VIR-2218 could generate aggregate revenues of $15B-plus over the next 15 years; risk-adjusted, we estimate VIR-2218 is worth $28 /share.”

Trucchio is bullish indeed. Along with a Buy rating, his $100 price target makes room for 12-month returns of a strong 290%. (To watch Trucchio’s track record, click here)

Most of Trucchio’s colleagues agree. With 6 Buys vs. 1 Hold, the stock claims a Strong Buy consensus rating. The forecast calls for one-year gains of 91%, considering the average target clocks in at $49. (See VIR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.