Supply chain snags have been the bane of many industries over the last couple of years and you can add the solar segment to the list of those affected. That said, while costs of solar materials have seesawed as a result, that hasn’t affected demand, which last year increased significantly and is expected to further rise this year. The industry also stands to gain from supportive policies such as those included in the Inflation Reduction Act (IRA). Additionally, Russia’s invasion of Ukraine and the consequent energy crisis have also helped boost the solar story.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Of course, any segment projected to post some robust growth will attract investors and one big Wall Street name has been taking note.

Steve Cohen, the billionaire Chairman and CEO of global asset management firm Point72, built his fortune using a high-risk/high-reward strategy and he evidently thinks the solar industry is a place to be right now. He recently loaded up on two names operating in the sector, and we dived into the TipRanks database to get the lowdown on both.

Turns out it’s not only Cohen who thinks these stocks are worth a punt. According to the analyst consensus, both are rated as Strong Buys, too. Let’s see why so many think the future is bright for these solar stocks.

Sunrun Inc. (RUN)

The first solar stock piquing Cohen’s interest is Sunrun, the US’s largest residential solar installer. Since its founding in 2007, the business has mostly concentrated on a power purchase agreement (PPA) business model, in which Sunrun installs and maintains a solar system on a customer’s home before selling power to the customer at an agreed-upon rate for a 20- or 25-year term.

With the global energy crisis acting as a tailwind, throughout 2022, Sunrun posted consistent year-over-year growth as was also evident in the recently released Q4 results. The company’s net subscriber value rose from the prior quarter’s $13,259 to $16,569 while customers grew 21% vs. the same period last year. Revenue rose by 40% year-over-year to $609.52 million, beating the Street’s call by $20.63 million. The company also dialed in a surprise profit, with EPS of $0.29 coming in well ahead of the -$0.27 anticipated.

The residential solar market is anticipated to see a 7% addition to capacity in 2023, but Sunrun expects 10% to 15% growth although the company warned that financing solar projects has become more expensive due to rising interest rates and that will probably impact the profitability profile.

All told, Steve Cohen must see plenty to like here. Already holding a position, In Q4, he doubled down and bought 871,943 shares, increasing his stake by 103% to a total of 1,723,560. These are now worth almost $38 million.

Mirroring Cohen’s positive take, Morgan Stanley’s Stephen Byrd calls Sunrun a ‘Top Pick’ and thinks the market is not assigning the stock’s correct valuation.

Explaining his stance, the 5-star analyst wrote, “RUN is currently trading at a $5.1bn market cap, however, we estimate that the value of its existing customers is ~$2.7bn, or ~53% of the current market cap. This implies that the market is baking in $2.4bn of value creation from new customer contracts, or just three years of ~20% annual customer growth, and modest improvement in net subscriber value. We view this as highly punitive given the fact that only 4% of U.S households currently have rooftop solar and the growing demand/value proposition for the technology.”

To this end, the Morgan Stanley analyst gives RUN shares a $65 price target to back his Overweight (i.e., Buy) rating. That figure makes room for 12-month gains of a whopping 196%. (To watch Byrd’s track record, click here)

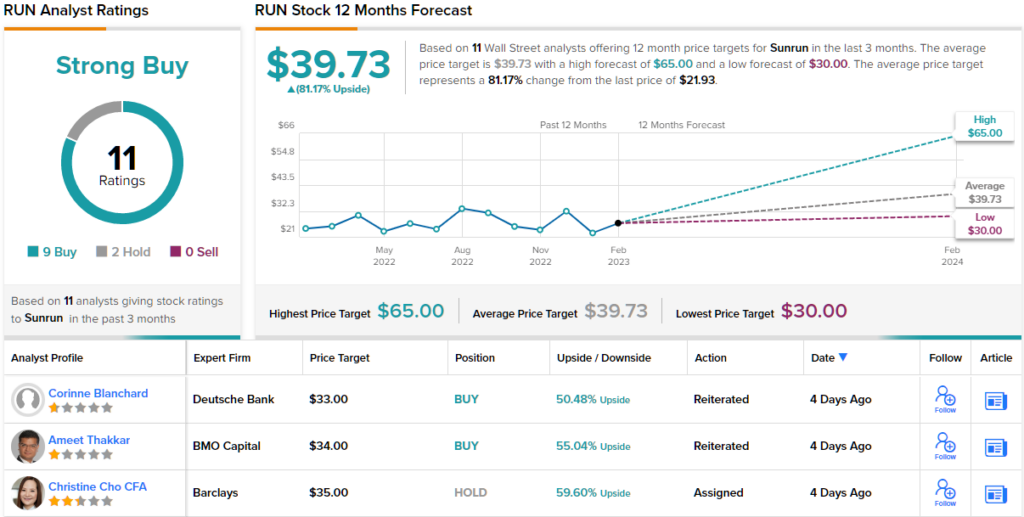

While Byrd is the Street’s biggest RUN bull, most are thinking along the same lines; based on 9 Buys vs. 2 Holds, the stock claims a Strong Buy consensus rating. Going by the $39.73 average target, the shares will climb 81% higher in the year ahead. (See RUN stock forecast)

SolarEdge Technologies (SEDG)

The next solar-themed stock Cohen has been loading up on is another leader in the field. SolarEdge Technologies is the world’s largest supplier of photovoltaic inverters. In fact, the company was the first to successfully make power optimizers a commercial success by producing a device that connects to the back of the solar panel via which the amount of power generated is increased, thereby helping lower the cost of energy the system produces.

Its Inverter expertise is also being applied to the creation of further smart energy products. By acquiring businesses that focus on different energy industry segments, including storage, batteries, grid services solutions, and electric vehicle charging, SolarEdge has expanded its portfolio of products.

The company is also reaping the benefits of growing demand in Europe, which now represents almost 60% of its total solar inverter volume. In the recently released Q4 report, driven by record revenues from the solar segment of $837 million, total revenue reached $890.7 million, amounting to a 61.4% year-over-year increase. Adj. EPS clocked in at $2.86, significantly higher than last’s year’s $1.10. Both the top-and bottom-line results beat Street expectations. Even better, for Q1, revenue is anticipated in the range between $915 million to $945 million, compared to consensus at $914.70 million.

It’s no wonder, then, that an investor like Steve Cohen would take an interest in a company like SolarEdge. In Q4, Cohen’s Point72 made a significant buy in SEDG shares, totaling 268,092 shares, which at the current share price are now worth over $79 million.

The billionaire isn’t the only fan. Guggenheim analyst Joseph Osha is impressed by the gains made in Europe, amongst other positive developments, and describes SEDG as a ‘Best Idea’ for 2023.

“In MW volume terms, Europe now represents 57% of total shipments, with 30% sequential growth for the quarter and 69% for all of 2022,” the 5-star analyst noted. “Those comparisons are probably too good to last – we show Europe at 44% volume growth for 2023 – but the results illustrate the extent to which SEDG is capitalizing on the surge in demand, particularly in Germany… Looking forward, the margin strength that we had been looking for has materialized, and our still-conservative model shows GAAP gross margin for 2023 at 30%, up from 29% previously.”

“It is clear to us that SEDG is the best way to invest in robust residential and commercial solar growth outside of the US, and at 28% of inverter volume the weaker US market should not be a problem in our view,” Osha summed up.

To this end, Osha rates the stock a Buy, while his $452 price target suggests the shares will climb ~53% higher in the months ahead. (To watch Osha’s track record, click here)

Most analysts agree with that assessment; SEDG’s Strong Buy consensus view is based on 15 Buys vs. 5 Holds. The forecast calls for one-year gains of 25%, considering the average target currently stands at $370.85. (See SEDG stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.