Just because something hasn’t happened yet doesn’t mean it isn’t about to. That essentially is the view of the legendary investor Stanley Druckenmiller regarding the prospect of a looming recession. Unlike other financial prognosticators, Druckenmiller hasn’t flip-flopped on the issue and has remained adamant that a recession is on the way.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

“To me the probabilities haven’t changed,” Druckenmiller has said, “it has been pushed out relative to expectations, but in no way does the fact that it hasn’t started yet change the probability whether it’s gonna be hard or soft.” In fact, Druckemiller not only thinks a recession is all but inevitable but that the dreaded hard landing is a more likely possibility.

That doesn’t mean Druckenmiller, who has a net worth of $6.4 billion and is famous for being an asset manager that has never had a down year, is turning his back on the markets. He still thinks that should a recession materialize, “pockets of the market” will do well, and he remains heavily invested in certain names.

We ran a couple of his big holdings through the TipRanks database to also see what the Street’s stock experts make of these choices. Turns out they’re betting on their continued success too; both are rated as Strong Buys by the analyst consensus. Let’s see why both Druckenmiller and the analysts are both backing these names’ chances.

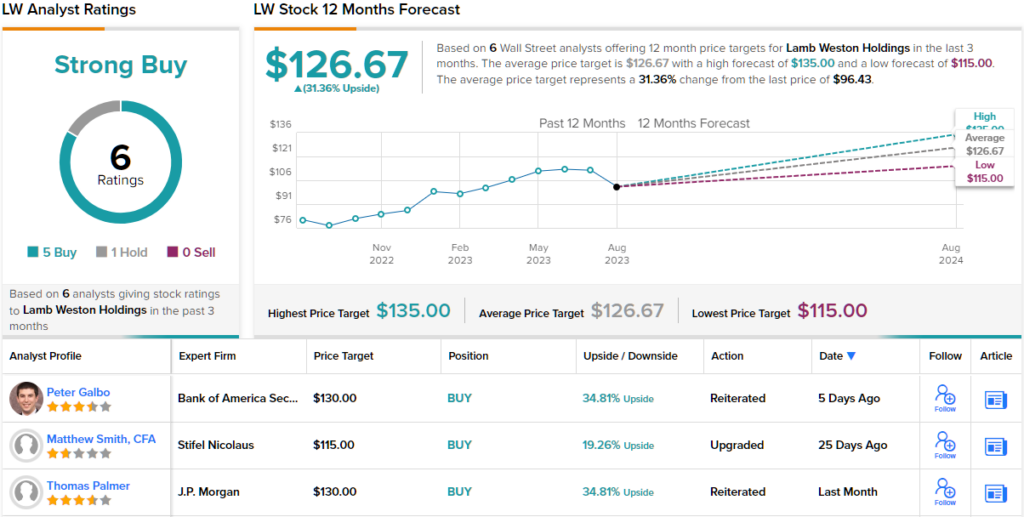

Lamb Weston Holdings (LW)

Druckenmiller is evidently convinced that during a recession, people are still going to be eating plenty of spuds. The first stock Druckenmiller has a big stake in is Lamb Weston, a company with ‘a passion for potatoes’ and is one of the world’s biggest players in the frozen potato industry. Druckenmiller is currently holding 2,066,610 shares of Lamb Weston, which command a market value of over $199.1 million.

Lamb Weston has a strong presence in various markets and specializes in producing a wide range of frozen potato offerings, including French fries, potato wedges, hash browns, and other potato-based appetizers.

The past couple of years have seen both revenue and net income jump substantially and more evidence of a business firing on all cylinders was on tap in the recently reported fourth quarter of fiscal 2023 report. Revenue rose by 47% year-over-year to reach $1.7 billion, beating the Street’s call by $40 million. At the other end of the scale, adjusted net income jumped by 90% to $178 million. The result of which was adj. EPS of $1.22, a figure that also beat the forecast – by $0.17.

Looking ahead to fiscal 2024, the company guided for net sales between $6.7 billion to $6.9 billion (compared to consensus at $6.77 billion) and diluted EPS in the range between $4.95 and $5.40. The Street was expecting $5.01.

Despite all that goodness, and perhaps due to elevated expectations amidst a previous high valuation, the shares fell in the aftermath of the report’s release and have been in a downtrend since. However, Jefferies analyst Rob Dickerson poses a rhetorical question for investors with a simple answer.

“Would you be a buyer of the shares? Short Answer: Yes,” says the analyst. “We see the potential for earnings upside as the year progresses, volume growth could meaningful accelerate by FY25E, and we do not have concerns about eroding pricing power as industry capacity comes online. The valuation also looks attractive to us. On forward P/E and EV/EBITDA, the LW shares are trading at near record-low multiples.”

These comments underpin Dickerson’s Buy rating while his $135 price target suggests shares will rise by 40% in the months ahead. (To watch Dickerson’s track record, click here)

Most analysts agree with the Jefferies view. The stock claims a Strong Buy consensus rating, based on 5 Buys vs. 1 Hold. At $126.67, the average target implies shares will appreciate by 31% over the one-year timeframe. (See LW stock forecast)

Option Care Health (OPCH)

For our next Druckenmiller-backed name, we’ll turn to the healthcare space and take a look at Option Care Health. This company is a provider of comprehensive and personalized infusion therapy services to patients across the US. In fact, it is the country’s largest home infusion company.

With a strong focus on patient well-being, Option Care Health offers a range of advanced therapies that encompass various medical conditions, including immunodeficiency disorders, chronic diseases, and other complex conditions that require intravenous or injectable treatments. Option Care has licenses for all 50 states, and in 45 of those has home infusion operations. These are supplemented by 157 ambulatory infusion suites.

On the financial side, over the past few years, the company has seen consistent revenue growth and that was the case again in the latest quarterly readout – for 2Q23. Revenues came in at $1.07 billion, amounting to a 9.1% year-over-yeear uptick. Adj. EBITDA of $110.1 million increased by 29.2% from the $85.2 million generated during the same period last year. Both figures came in above Street expectations. For the full year 2023, Option Care anticipates net revenue between $4.2 billion to $4.3 billion and adj. EBITDA in the $415 million to $425 million range.

While Druckenmiller had some OPCH stock among his holdings beforehand, he upped his fund’s stake considerably in Q2 with the purchase of 3,587,359 shares. The total holdings now stand at 4,391,174 shares, which currently command a market value of almost $153.7 million.

The company also has a fan in J.P. Morgan analyst Lisa Gill, who is impressed by the recent performance and sees more good stuff on the way.

“1H23 was supposed to be a challenging period for OPCH in terms of comparative margins; however, the company has acquitted itself well, we believe that cost savings y/y will flow through to the back half, making the updated adj. EBITDA margin doable in our view,” the 5-star analyst said. “The company continues to deliver impressive results and we believe it will continue to be a beneficiary of the ongoing shift in sites of care and robust pipeline of therapies… We have been consistent that we see OPCH as a beneficiary of new therapy areas, and we see this as a key driver in the chronic infusion growth algorithm.”

To this end, Gill rates OPCH shares an Overweight (i.e., Buy), backed by a $46 price target. The implication for investors? Upside of 31% from current levels. (To watch Gill’s track record, click here)

Summing up, all 4 other analysts who have recently reviewed this stock are on the same page – giving it a ‘Buy’ rating unanimously, resulting in a ‘Strong Buy’ consensus rating. The forecast calls for 12-month returns of 18%, considering that the average target price is $41.40. (See OPCH stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.