The assumption among most financial prognosticators is that a recession is most likely on the way, and one prominent name agrees it’s all but inevitable. Legendary investor Paul Tudor Jones sees a recession coming and even has an idea of when it will hit.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The Tudor Investment Corp founder and billionaire expects a recession will come into play this fall, mainly as a result of the surge in debt and asset prices in recent years. Such activities are usually followed by an economic downturn.

“Historically, it’s about a two year lag when that really really bites, and you go into recession,” Tudor Jones explained. “That would be third quarter this year, there’s a good chance that – based on our most recent financial episode – there’s a really good chance that we’re on the verge of looking like or actually going into recession.”

That’s not to say it’s time to walk away from the stock market. In fact, Tudor Jones has been padding the portfolio with the equites he sees as well-equipped to deal with an upcoming recession – he’s been pouring millions into several. We ran a couple of new additions to his stock collection through the TipRanks database to also gauge Street sentiment toward these names. Here are the results.

Abbott Laboratories (ABT)

During periods of economic downturn, healthcare stocks are often regarded as defensive investments due to their resilience and stability in the face of recessionary pressures. This holds true for Abbott Laboratories.

Founded all the way back in 1888, Abbott is a multinational healthcare firm renowned for its extensive range of products and services in diagnostics, medical devices, nutrition, and branded generic pharmaceuticals. With a rich history, a global presence in more than 160 countries, approximately 115,000 employees, and a market capitalization of $189 billion, Abbott has earned a reputation for innovation and holds a significant position in the industry.

Investors gave the thumbs up to the company’s latest quarterly results, despite the numbers showing a drop compared to the year-ago period. While revenue fell by 18.5% year-over-year to $9.7 billion, the figure just edged ahead of the consensus estimate. The company stated that the sales drop was due to an expected decline in COVID-19 testing-related sales compared to the previous year. On the bottom line, adjusted EPS declined by 40.5% from the same period a year ago to $1.03, but that figure exceeded the forecast by $0.05. Regarding the yearly outlook, the company maintained its forecast of adjusted EPS in the range of $4.30 to $4.50.

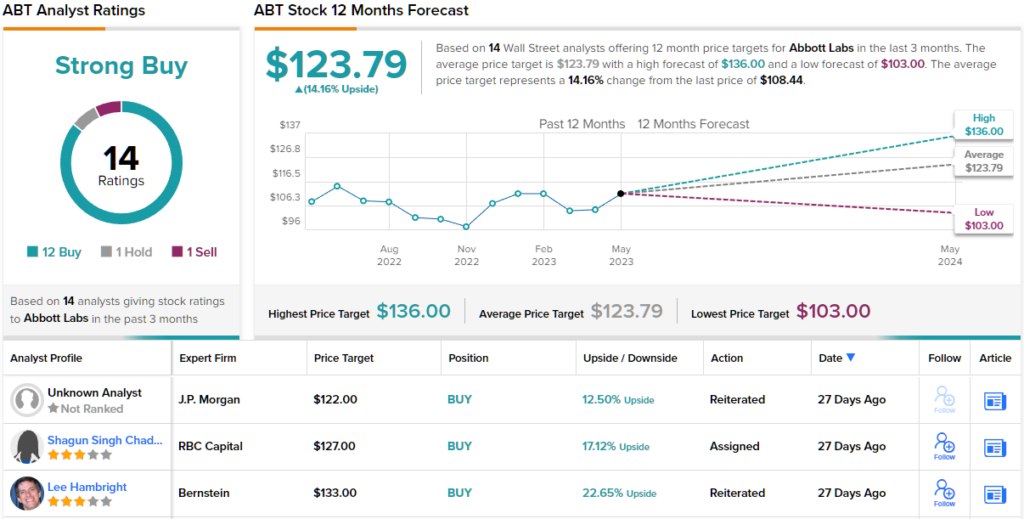

Tudor Jones must like what’s on offer here. He opened a new position in ABT during the first quarter, with the purchase of 139,628 shares. These are now worth $15.13 million.

The company also has a fan in Morgan Stanley analyst Cecilia Furlong. She says of the company: “Abbott possesses a strong balance sheet, supporting a faster organic growth profile in the base (ex-COVID Dx) business in 2023-2025, with 1Q results highlighting base business strength. Recent headwinds, including the infant formula recall, alongside macro pressures on supply and margins, continue to improve, and at current levels we remain constructive going forward on Abbott given its peer-leading organic growth profile (ex-COVID Dx), diversified business composition, continued core margin expansion opportunity post-COVID, and below-peer net leverage, creating optionality.”

Quantifying this stance, Furlong rates ABT shares an Overweight (i.e. Buy) while her $133 price target suggests share will appreciation of ~23% for the year ahead. (To watch Furlong’s track record, click here)

Elsewhere on the Street, the stock garners an additional 11 Buys, and 1 Hold and Sell, each, for a Strong Buy consensus rating. Going by the $123.79 average target, the shares will climb 14% higher over the coming months. As an added bonus, the company also has a dividend which it has regularly increased over the years. The current payout stands at $0.51 and yields 1.78%. (See ABT stock forecast)

Johnson & Johnson (JNJ)

From one healthcare giant to an even bigger one. With a market-cap over $411 billion, Johnson & Johnson is one of the largest healthcare corporations in the world. The company operates through three business segments: pharmaceuticals, medical devices, and consumer health.

In the pharmaceutical sector, Johnson & Johnson develops and markets a diverse portfolio of prescription drugs, with a focus on areas such as oncology, immunology, neuroscience, and infectious diseases. The company’s medical devices segment manufactures and sells a broad range of innovative medical equipment, including surgical instruments, orthopedic devices, cardiovascular products, and diagnostics. Additionally, Johnson & Johnson offers a variety of consumer healthcare products, such as over-the-counter medicines, baby care items, oral care products, and beauty and skincare brands.

The value proposition proved advantageous for the company in the most recently reported quarter, 1Q23. The company delivered revenue of $24.7 billion, reflecting a 5.6% year-over-year increase and surpassing the forecast by $1.09 billion. Moreover, the adjusted EPS of $2.68 exceeded the analysts’ anticipated $2.50.

Even better, the company raised both its sales and earnings outlook for FY23. Additionally, the dividend got a boost, seeing a 5.3% increase to $1.19 per share. The payout currently provides a yield of 2.81%.

Tudor Jones enters the frame here with the purchase of 216,183 shares in Q1, a new position in JNJ that is now worth more than $34.23 million.

Jones is not the only one backing JNJ’s cause. Hailing a ‘beat and raise’ quarter, Cantor analyst Louise Chen sings the healthcare giant’s praises and believes the stock is undervalued.

“The strength and durability of JNJ’s business segments remain underappreciated, in our view,” Chen said. “We continue to believe that upward earnings estimate revisions and multiple expansion to 15-20x 2023E EV/EBITDA now from ~13x, driven by above-market growth in its key franchises, should move JNJ shares higher.”

These comments form the basis for Chen’s Overweight (i.e., Buy) rating, while her $215 Street-high price target implies shares will rise by 36% over the next year. (To watch Chen’s track record, click here)

Looking at the ratings breakdown, based on a total of 5 Buys and 12 Holds, the analyst consensus rates the stock a Moderate Buy. The forecast calls for one-year returns of 13.5%, considering the average target stands at $179.52. (See JNJ stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.