While markets have seen sound gains year-to-date, with the S&P 500 up more than 7% and the NASDAQ an even better 15%, plenty of indicators are sending out contrary signals. Inflation remains high, but there’s doubt that the Fed could keep boosting interest rates without sparking another banking crisis, and there’s real worry that the combination of high inflation, high rates, and an unstable banking sector may bring about a recession in the near term.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Watching current conditions, billionaire hedge manager Paul Singer believes that the difficult macro environment will only present more and harder challenges going forward. Singer is already known for his accurate forecasts of past crises – the 2008 financial collapse and the post-COVID inflation spike – a record that gives his current prognostications a high level of authority.

What Singer sees now is a high-risk environment in which the world’s central banks are highly likely to make the wrong decision, no matter what they do. Describing the situation, Singer says, “I think that this is an extraordinarily dangerous and confusing period… Valuations are still very high. There’s a significant chance of recession. We see the possibility of a lengthy period of low returns in financial assets, low returns in real estate, corporate profits, unemployment rates higher than exist now and lots of inflation in the next round…”

So what to do? Singer, through his activist investor firm, Elliott Investment Management, has been making big investments in two stocks that have shown they can keep posting gains; both of which have shown strong 12-month gains, and Singer has bought in for over half a billion dollars in each. We’ve used TipRanks, the world’s biggest database of analysts and research, to see what Wall Street analysts have to say about whether these stocks make compelling investments. Let’s examine the findings.

Marathon Petroleum (MPC)

Accounting for one of his biggest holdings in his portfolio (10.5%), and worth $1.47 billion, the first Singer-backed stock we’ll look at is Marathon Petroleum, one of the oil industry’s major names.

Marathon is North America’s largest petroleum refining company, boasting a market cap of $57 billion and more than $177 billion in annual operating revenues. Significantly, despite a fall in oil prices through the second half of 2022, Marathon was able to outperform the equity markets by a wide margin; the company’s stock was up 60% in the last 12 months, compared to the near-7% drop in the S&P 500 over that same period.

Marathon’s refining operations back up this performance. From its headquarters in Findlay, Ohio, Marathon oversees a continent-spanning refining network of 13 active refineries that can process 2.9 million barrels of oil per day. In addition, the company has a nationwide network of branded gas stations and is a major producer and distributor of petrochemicals such as naptha, benzene, butane, xylene, and propylene, as well as fuel-grade coke for industrial purposes.

Marathon saw some solid gains in its last reported financial quarter, 4Q22. The company’s top line of $40.1 billion beat forecasts by over $4.6 billion and gained more than 12% year-over-year. At the bottom line, Marathon’s EPS, reported at $6.65, was $1.02 higher than expected and more than 5x higher than the year-ago quarter’s figure of $1.30. The company managed to achieve these gains even as revenues and earnings have been sliding since the peak reached in 2Q22.

Along with the top and bottom line beats in Q4, Marathon continued its policy of generous capital returns to shareholders. For the full year 2022, the company returned a total of $13.2 billion to its shareholders, a total that includes $11.9 billion in stock buybacks and $1.3 billion in common share dividend payments. The most recent dividend, paid out on March 10, was set at 75 cents per common share; at its annualized rate of $3, it yielded an above average 2.28%. Even after these significant capital returns, Marathon finished 2022 with $11.8 billion in cash and other liquid assets available on the books.

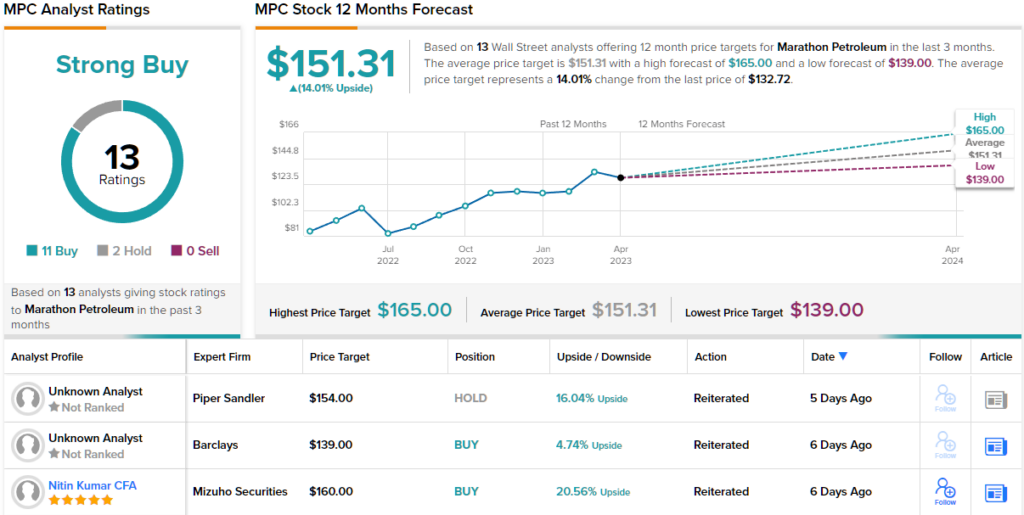

This stock has caught the eye of Raymond James analyst Justin Jenkins, who holds a 5-star rating from TipRanks. Jenkins writes of MPC: “The evolution of Marathon Petroleum continues to unfold in a positive direction — as dramatic cash returns to shareholders and asset base improvements continue to become more apparent. 4Q22 results show MPC is a top-tier refining operator with commercial excellence as MPC was again able to capture strong refining margins. Capital allocation remains disciplined toward shareholder returns, renewables investments, and optimization capital in refining/ midstream…”

“While MPC has executed on its capital allocation and shareholder return goals, excellent operations, a supportive refining macro, and continued emphasis on returns by management drives MPC to be our top refining pick even after dramatic outperformance over roughly the past two years,” the analyst added.

To this end, Jenkins rates MPC shares a Strong Buy, along with a $165 price target to show his confidence in an upside potential of 24% for the next 12 months. (To watch Jenkins’ track record, click here)

Keeping with the bullish outlook, MPC shares also have a Strong Buy consensus rating based on 13 recent analyst reviews. These include 11 Buys, that outweigh the 2 Holds. Shares are trading for $132.69 and their $151.31 average price target implies a 14% gain by year’s end. (See MPC stock forecast)

Pinterest, Inc. (PINS)

Singer’s next big holding is Pinterest, which takes sixteenth place in his portfolio (5.5%) with a value just north of $785 million.

Pinterest is a social media platform that functions as a visual bulletin board. Similar to other social media sites, Pinterest users publish and share their own content with friends or the public. However, what sets Pinterest apart is its focus on visual content such as pictures, graphics, and videos. This content is organized into categories, making it easier for users to browse.

Furthermore, Pinterest has expanded into e-commerce, allowing users to create digital storefronts where customers can search and browse merchandise.

As a social media platform, Pinterest has appealed primarily to women, who make up approximately two-thirds of the company’s user base. The user base also skews young, with the 18-25 age group growing faster on the platform than the over-25s. While Pinterest has been working to expand its appeal to male users, the company’s most recent acquisition activity – its June 2022 of the AI-powered online shopping platform THE YES – expands its ability to cater to its largest demographic of younger women.

Shares in Pinterest have gained 20% over the past year, a substantial outperformance compared to the overall stock market, and shows that Pinterest has staying power.

While the stock has outperformed, the company has been showing a mixed bag in its financial results. For 4Q22, the last quarter reported, Pinterest had a top line of $877.2 million. This was up 3.6% year-over-year, but about $9.5 million short of analyst expectations. The bottom line figure, a non-GAAP EPS of 29 cents, was 1 cent ahead of the forecast, but was far down y/y. The EPS result fell 20 cents, or 40%, from the year-ago quarter.

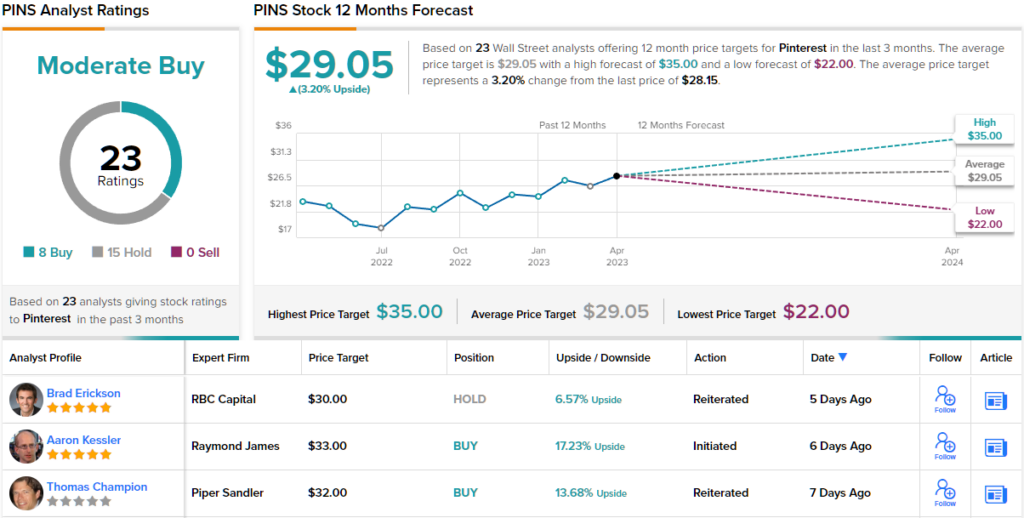

Wolfe 5-star analyst Deepak Mathivanan doesn’t appear worried about the mixed earnings, but rather, focused more on the solid outperformance.

“PINS remains one of our top picks for FY23. Admittedly, the top-line sensitivity is likely to be higher NT given exposure to discretionary verticals. However, we think the LT thesis centered on product enhancements, engagement growth, and monetization gains are still fully intact. New product launches and partnerships are likely to be positive catalysts for the stock through the remainder of the year. Shares trade at 23x FY24 EBITDA, a premium relative to ad peers, which we think is justified given the potential for upside to our year estimates,” Mathivanan opined.

These comments underpin the analyst’s Outperform (i.e. Buy) rating on PINS, and his $33 price target implies a potential one-year upside of 17%. (To watch Mathivanan’s track record, click here)

Overall, PINS has a Moderate Buy consensus rating, based on 23 reviews that include 8 Buys and 15 Holds. The average price target of $29.05 suggests a modest 3% gain from the current trading price of $28.15. (See PINS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.