How far can good vibes push the market? That’s a question investors should think about, especially if events pan out as investing legend Leon Cooperman believes they will.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The billionaire hedge fund manager does not see the current rally in stocks as anything sustainable, and cautions that it is built more on positive sentiment than on anything solid. Moreover, he holds a pessimistic outlook regarding the S&P 500‘s ability to not only reach but also surpass its peak level of 4,800 achieved back in January 2022 for several years.

Diving into specifics, Cooperman observes that the rise in stocks this year is not attributed to improved fundamentals, but rather to improved sentiment. Investors are feeling optimistic about stocks at the moment, leading them to buy in, even though corporate profits aren’t keeping up. Cooperman cautions that this kind of optimism cannot last, and when it eventually falters, it will coincide with the Fed’s rising interest rates. This combination may bring about a recession in 2024.

“There’s a lot of crazy things going on in the market. I’ve never seen moves on such insignificant news as we’re seeing in the market today,” Cooperman has said, and he adds, regarding a prospective recession, “If we have one it may come next year, when people run out of money and the Fed keeps raising rates.”

This isn’t to say that there aren’t good investments to make right now, and Cooperman stays heavily invested in stocks that he describes as ‘good values.’ We ran a couple of his big holdings through the TipRanks database to see what the Street’s stock experts make of these choices. Let’s take a closer look.

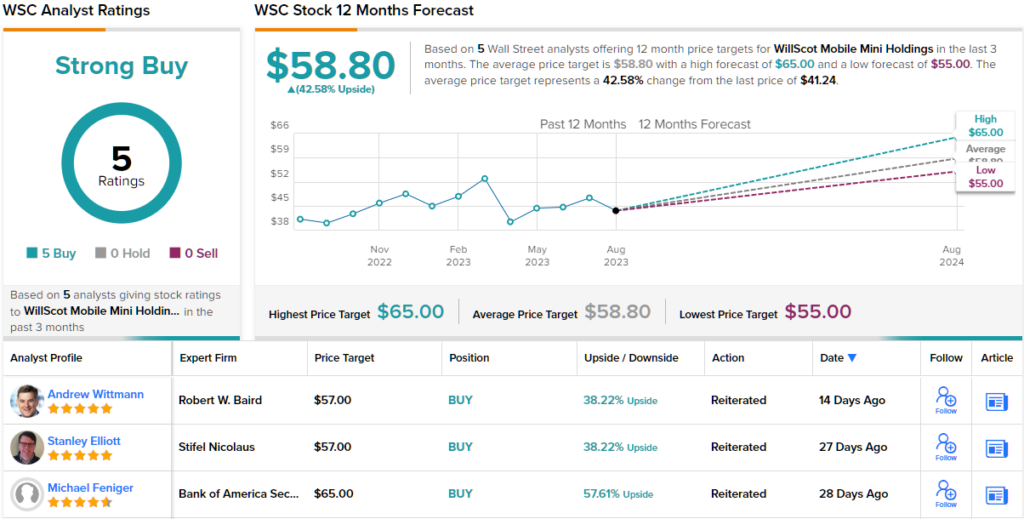

WillScot Mobile Mini Holdings (WSC)

We’ll start with WillScot Mobile Mini Holdings, an office space company with a twist. WillScot focuses on temporary building spaces, including prefabricated office, classroom, and storage units. It’s an interesting niche, and Leon Cooperman clearly sees potential in it – evident from his significant stake in WSC, totaling 1,698,951 shares. At current valuations, his holding in WillScot is worth $70 million.

Among WillScot’s primary products are portable offices, prefab offices, and office trailers. These structures are quick to assemble, easy to install in desired locations, and offer modular capabilities, enabling the creation of prefabricated office complexes larger than 1,000 square feet. Building upon this foundation, WillScot has also developed and introduced a line of prefab classrooms suitable for K-12 and post-secondary settings. The company’s product range extends to specialty temporary buildings, including blast-resistant security structures, as well as portable toilet and washroom facilities. Additionally, the company offers a series of steel storage units designed to withstand all weather conditions.

WillScot has long had a habit of expanding through acquisition, and earlier this month the company announced that it acquired both the California-based Cold Box and the Ohio-based A&M Cold Storage. These moves will enhance WillScot’s ability to provide cold storage options, and bring the firm approximately 3,500 new assets, including climate-controlled containers and walk-in freezers. In September of last year, WillScot acquired Allied Office Trailers and Storage Containers, a move that brought more than 8,000 mobile offices and portable storage units into WillScot’s fleet of rentable assets.

Earlier this month, WillScot released its financial results for 2Q23, and the stock promptly fell 12% from the peak it reached the previous day. The company’s results were not bad – rather, they simply did not meet high revenue expectations which had been prompted by several years of COVID-era and post-COVID successes.

WillScot posted a revenue of $582 million, showing marginal year-over-year growth. However, it fell short of forecasts by nearly $698K. On the profit front, the company’s non-GAAP EPS stood at 44 cents per share, surpassing estimates by 3 cents per share. We should also note that the Q2 EPS was up 11 cents y/y, and the 1H23 EPS, at $1.46, was a full 90 cents per share higher than the 1H22 figure.

Citing WillScot’s recent record of success, Stifel 5-star analyst Stanley Elliot describes the post-earnings weakness in the stock as a chance to buy in. He writes, “Given WSC’s strong track record, we believe the in-line revenue and guidance reiteration likely spooked investors amid high expectations. We believe softer unit on rent metrics indicates some sequential softening (largely retail), but is largely due to unsustainable utilization given the strength in 2022 on top of a much larger fleet from recent M&A.”

Summing up, Elliot says, “Overall, we remain pleased with execution on VAPs, tuck-ins, and efficiency gains that have enabled WSC to more than double fleet and rate while maintaining 17% ROIC on a TTM basis. We believe weakness in the shares in response to the print presents an attractive opportunity for longer-term investors.”

Elliot quantifies his bullish stance on WillScot with a Buy rating and a $57 target price that implies the shares will increase by 38% over the next 12 months. (To watch Elliot’s track record, click here)

Overall, the bulls are definitely running for WSC, as the stock’s Strong Buy consensus rating shows – it is backed up by 5 unanimously positive analyst reviews. The shares are trading for $41.24 and the $58.80 average price target suggests a one-year upside potential of ~43%. (See WSC stock forecast)

Mr. Cooper Group (COOP)

The second pick from Cooperman that we’re looking at is the Mr. Cooper Group, a firm based in Dallas, Texas, and operating in the mortgage loan servicing industry. Leon Cooperman doesn’t appear to be concerned about the softness in the real estate sector or the reduced homebuying activity due to higher mortgage rates. His investment in the Mr. Cooper Group amounts to $240.8 million, equivalent to 4,249,000 shares.

The Mr. Cooper Group takes a customer-first approach to the mortgage business, in its servicing, loan origination, and transaction activities. The company’s work is focused mainly on single-family residences in the US housing market, and its one of the US’ largest home loan servicers. The company’s Xome brand is on the tech side, and provides data enhanced tech solutions to buyers, sellers, real estate agents, and mortgage loan providers.

By the numbers, Mr. Cooper Group is huge on every measure. The company boasts over 4.3 million customers, has originated $3.8 billion in home loans, and its Xome brand subsidiary has facilitated sales of more than 114,000 homes totaling $18.8 billion. The Mr. Cooper Group is the largest non-bank mortgage servicer in the US, the 3rd largest servicer of any type; it is ranked among the top 30 mortgage loan originators in the US real estate market.

That foundation supported some solid numbers in 2Q23. The company’s total revenue, at $486 million, beat expectations by $73.22 million. On the bottom line, the company’s non-GAAP EPS, of $1.66 per share, was 45 cents better than had been anticipated.

For analyst Kevin Barker, who covers the stock for Piper Sandler, these facts add up to a sound investment. The 5-star analyst writes, “This was another solid quarter for COOP as earnings were better than expected, the company increased guidance for servicing income, and there are a series of one-time gains in 2H23 that will drive TBV higher. The Servicing segment produced higher fees, lower than expected amortization, and higher net interest income. Meanwhile, the Origination segment saw margins tick higher as the competition abated in the correspondent market. Management seemed upbeat on the outlook for the rest of the year and into 2024 with ROEs expanding well into the double digits. Overall, a good quarter and our thesis on COOP remains intact.”

Looking ahead, Barker gives COOP shares an Overweight (i.e. Buy) rating with a $72 price target that suggests a one-year gain of 27%. (To watch Barker’s track record, click here)

Overall, COOP holds a Moderate Buy rating from the analysts’ consensus, based on 5 recent analyst reviews with a breakdown of 3 to 2 favoring Buys over Holds. The average price target among these analysts stands at $67, implying that the stock will gain 18% over the next 12 months from the current trading price of $56.67. (See COOP stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.