With a history of decades-long investing success, billionaire Ken Griffin knows a thing or two about market behavior. Recently, the Citadel Investment Group Founder and CEO offered some of his thoughts on the state of the stock market and where the economy is heading.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

While Griffin believes inflation has already peaked, he thinks the Fed has yet to truly put the “genie back in the bottle.” He also thinks unemployment is about to rise and expects a recession will likely materialize “sometime in the middle to back half of 2023.” Furthermore, says Griffin, the recent FTX fiasco will see people “lose billions of dollars,” the “absolute” travesty of an event having shaken trust in the markets.

Meanwhile, against this messy backdrop, Griffin has been busy padding his fund’s portfolio, and recently he loaded up on two stocks. We dipped into the TipRanks database to get the lowdown on both. Turns out Griffin is not the only one showing confidence in these names. Both are rated as Strong Buys by the analyst consensus. Let’s see why they are drawing plaudits right now.

The Trade Desk (TTD)

We’ll start with a major player in the ad tech space. The Trade Desk runs the world’s biggest independent demand-side platform (DSP) for online ads. Ad agencies, advertisers and trading desks can place bids on programmatic ads thanks to DSPs. When compared to sell-side platforms (SSPs), which assist publishers in selling their own ad inventories, they are at the other end of the advertising supply chain.

While ad titans such as Google will offer packages which include DSPs, SSPs, and various advertising products in what is known as ‘walled gardens,’ companies that don’t wish to be beholden to one giant entity would rather use the services of an independent platform such as The Trade Desk.

The advertising space is sensitive to the economic backdrop, with ad budgets fluctuating according to the strength of the economy. As such, the segment has been under pressure in recent times. Nevertheless, The Trade Desk has shown its quality by handling the roughshod conditions well, as was evident in its latest quarterly report – for Q3.

In the quarter, revenue increased 31% year-over-year to $395 million, while beating the Street’s forecast by $8 million. Adjusted net income rose 45% to $129 million, translated to $0.26 per share, trumping the $0.23 consensus estimate.

Looking ahead, the company expects its Q4 revenue to be “at least” $490 million, compared to the analysts’ expectation of $509.13 million.

This digital ad giant has proved of interest to Ken Griffin, who increased his fund’s stake in TTD by 204% in Q3, with the addition of 980,622 shares. His holding is currently worth over $71 million.

Griffin is not the only one showing confidence in this name. Scanning the Q3 print, Truist 5-star analyst Youssef Squali is unequivocal in his praise.

“TTD reported another strong quarter as its execution remains exceptional amid a challenging macro, reflecting material market share gains,” Squali said. “Strength was broad-based but particularly skewed to CTV, which is likely to continue in 2023 given its rapid adoption both in the US/ int’l and with the expected massive growth in inventory from Netflix, Disney+ and others; augmented by growing shopper mktg budgets moving to the platform. We view the 4Q22 guide and 2023 commentary as appropriately conservative given the macro.”

“TTD remains one of our favorite stocks given its execution within a compelling and large TAM,” the analyst summed up

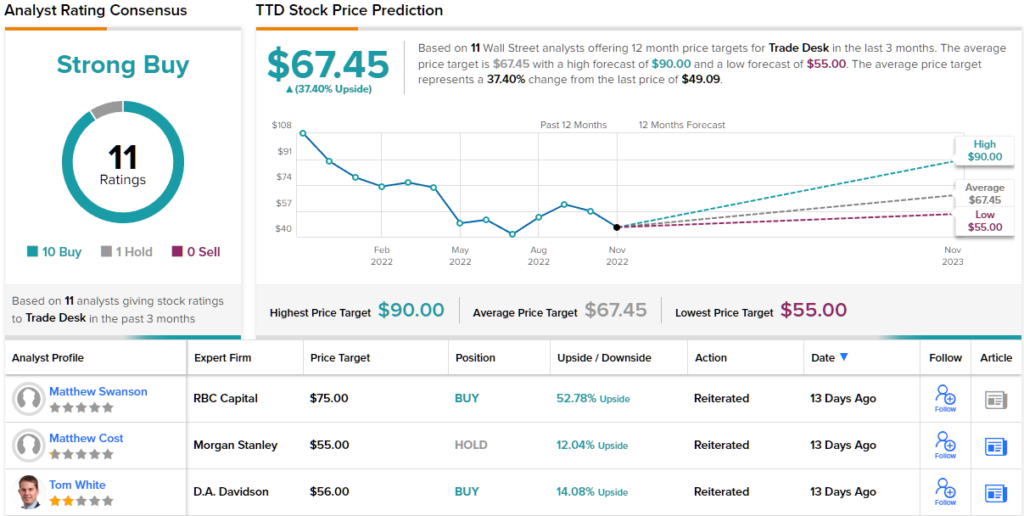

These comments underpin Squali’s Buy rating and $74 price target for the stock. The figure makes room for one-year gains of 51%. (To watch Squali’s track record, click here)

Looking at the consensus breakdown, 1 analyst remains on the fence, but all 10 other recent reviews are positive, naturally leading to a Strong Buy consensus rating. At $67.45, the average target suggests an upside potential of ~37% in the year ahead. (See TTD stock forecast on TipRanks)

Bunge Limited (BG)

The next stock Griffin has been leaning into is of an entirely different ilk. One of the biggest oilseed processors in the world, Bunge runs an integrated company that includes buying, processing, storing, and selling grains and oilseeds. The agribusiness assets are spread across Europe, Asia Pacific, South and North America. Additionally, Bunge operates a downstream food business, selling packaged vegetable oils, wheat flours, bakery mixes and dry milled corn products. It also holds a 50% stake in BP Bunge Bioenergia, a joint venture with British oil behemoth BP, via which it produces sugar and ethanol in Brazil.

The markets might have been in turmoil all year, but Bunge appears to be an outlier; in contrast to most names, the shares are up 11% in 2022. The company’s value proposition and global positioning have proven beneficial in a world rocked by geopolitical unrest and supply chain snags.

This was clear to see when the company reported Q3 earnings at the end of October. Revenue hit $16.76 billion, amounting to an 18.7% year-over-year increase and coming in $1.03 billion above the Street’s forecast. Likewise, at $3.45, adj. EPS came in $0.90 higher than the $2.55 expected by the prognosticators.

Griffin evidently thinks the company will continue to outperform. He upped his fund’s holdings significantly in the quarter, having bought 941,945 shares. At the current share price, Citadel’s total stake in BG is now worth $99 million.

Echoing Griffin’s activity, BMO 5-star analyst Kenneth Zaslow is a big BG fan and sees plenty to remain upbeat about.

“With its global footprint and risk management, BG is built for the current volatility and the ongoing shifts in trade flows. Second, with its geographic positioning and operational excellence (high capacity utilization rates), BG is among the best positioned to capitalize on the higher global crush margins created by a sustainably strong demand-driven operating environment (e.g., RD demand) and the ongoing global supply tightness (e.g., Ukraine war). Third, BG’s strong cash flow and exceptional balance sheet creates incremental optionality to return cash to shareholders (i.e., more buybacks),” Zaslow opined

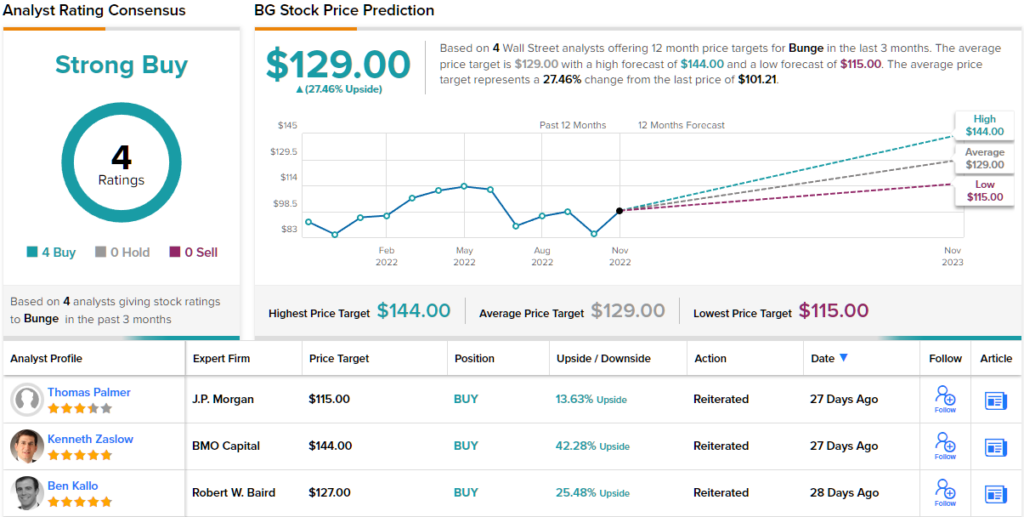

Accordingly, Zaslow rates BG shares an Outperform (i.e. Buy), backed by a $144 price target. The implication for investors? Upside of 42% from current levels. (To watch Zaslow’s track record, click here)

Over the past 3 months, 3 other analysts have chimed in with BG reviews and they say Buy, too, making the consensus view here a Strong Buy. Going by the $67.45 average target, the shares have room for growth of 39% over the one-year period. (See Bunge stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.