While last year wasn’t a particularly good year for stock investors, at least one man closed it out with a smile. Ken Griffin, the billionaire founder of the Citadel hedge fund, didn’t just outperform the markets last year – he managed to outperform them by a margin of $16 billion. It was the highest annual profit ever seen by a Wall Street hedge fund, and reflected the 38% return generated by Citadel’s flagship fund.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Now we all know that past performance is no guarantee of future gains – but it’s only human to want to follow a winner, and Griffin’s success in a truly bearish market has, for now, set him head and shoulders above the ordinary.

Recent regulatory filings show that Griffin has moved heavily into high-yield dividend stocks, the stock market’s traditional defensive play.

Using TipRanks database, we’ve pulled up the details on two of Griffin’s moves, both Buy-rated equities with dividend yields exceeding 6%. We can turn to the Wall Street analysts to find out what else might have brought these stocks to Griffin’s attention. Let’s take a closer look.

New York Community Bancorp (NYCB)

We’ll start with New York Community Bancorp, a major name in the banking industry. NYCB recently acquired Flagstar Bank, and is now one of the largest regional banks in the US. The bank offers a full range of services to retail and commercial customers, including mortgage origination and services.

The company announced its 4Q22 and full year results on January 31, and saw an immediate positive effect on its stock. The financial release showed a bottom line of 30 cents per diluted share for Q4, exactly the same result as one year earlier – but well above the 20 cents expected. Full-year EPS came in at $1.26 per diluted share, compared to $1.20 in 2021.

On the balance sheet, the bank had $90.1 billion in assets, compared to $63 billion at the end of 4Q21. The total included $25.8 billion in assets accrued during the Flagstar acquisition.

Also in January, NYCB declared its next dividend payment, for February 16. The payment, of 17 cents per common share, annualizes to 68 cents and gives a yield of 7.1%. The company has held its dividend at 17 cents per share since 2016, and has a history of payments going back to 1994.

Ken Griffin clearly sees this bancorp as sound investment, as his recent Q4 filings show that he bought in big. In fact, Griffin expanded his existing position in NYCB by over 12.4 million shares – or a whopping 13,215%. His ownership stake in the company is now worth over $119 million.

Griffin isn’t the only one bullish on this stock. Covering NYCB for RBC, 5-star analyst Jon Arfstrom takes a bullish stance, writing: “We view core trends as favorable with strong organic loan and deposit growth, better than expected margin expansion, and stable credit quality. Additionally, the company announced a material restructuring of the Flagstar mortgage business that should help drive improvement in the expense base and efficiency over time. Overall, we believe the outlook is reasonable, though dependent on successful execution of the Flagstar integration and restructuring activities.”

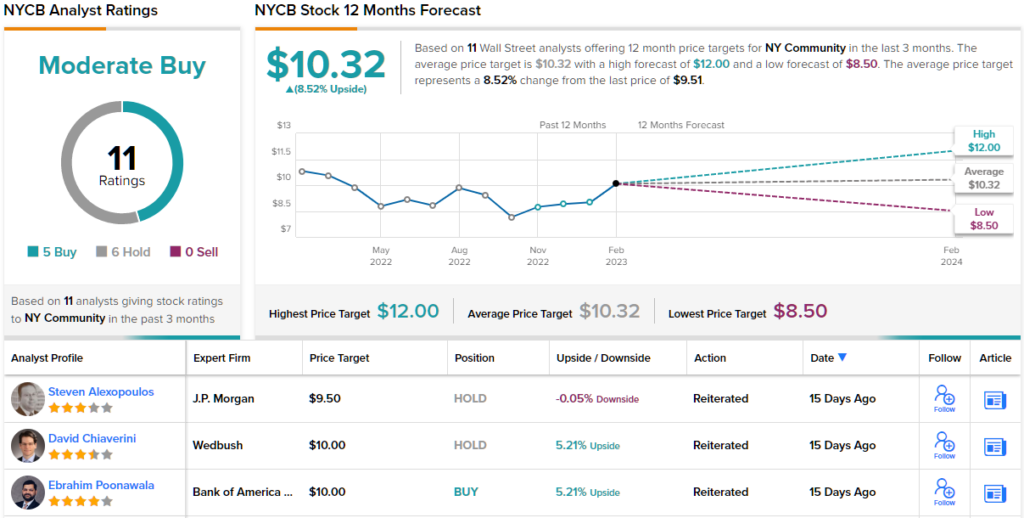

Looking forward, Arfstrom sets an Outperform (i.e. Buy) rating on NYCB shares, along with a $12 price target. Based on the current dividend yield and the expected price appreciation, the stock has ~33% potential total return profile. (To watch Arfstrom’s track record, click here)

Panning out to a bigger picture, we find that 11 analysts have weighed in on NYCB recently; their reviews include 5 to Buy and 6 to Hold, for a Moderate Buy consensus rating. (See NYCB stock forecast)

Newell Brands Inc. (NWL)

From banking we’ll switch to consumer staples. Newell Brands may not be a name you know – but it’s almost certain that you’ve used the company’s products. Newell is the manufacturer and distributor of well-known brands such as Paper Mate and Parker pens, X-Acto knives, Sharpie markets, Rubbermaid containers, Baby Jogger strollers, and even Mr. Coffee.

While Newell has its hands in a variety of aspects of everyday life, it has been subject to inflationary pressures over the past year. As prices rose, consumers began to cut back on non-essential items – at the same time, companies like Newell also faced pressure in their own purchasing offices as the costs of raw materials went up.

The result, in the company’s recently reported 4Q22 results, was a year-over-year decline in sales. Quarterly net sales dropped 18.5% to $2.3 billion; core sales were down by 9.4%. The company also saw the non-GAAP EPS decline from 53 cents in Q3 to just 16 cents for Q4. However, the Q4 EPS did beat expectations by wide margins; analysts had been looking for just 11 cents per share.

At the same time, Newell has kept up its highly reliable dividend payment. The company this month declared its next payment for March 15, at 23 cents per common share. Newell has held the dividend at this level since 2017, and the annualized payment of 92 cents is now yielding 6.1% – about triple the average dividend yield found among S&P-listed firms.

It’s clear that Ken Griffin saw something worthwhile in Newell Brands; he had an open position on the stock, and loaded up on another 2,285,158 shares in Q4. This expanded his holdings of NWL by more than 300%, and gave him over $45 million interest in the company.

Griffin isn’t the only bull here. In her coverage of this consumer staples company, J.P. Morgan analyst Andrea Teixeira sees it clearing a path forward.

“We remain positive in the long run as we think post 1H23 (with sequential progress in 2Q23), the company will start to show the benefits from the restructuring (project OVID and Project Phoenix introduced back in January – see our note), which along with the recent leadership shuffle announced in December is set to allow better execution of this roadmap. Admittedly, the company is seeing greater than originally expected pressure in some more discretionary categories or those more exposed to low-income consumers (e.g., small appliances, home fragrances), but we expect most of the slack to be picked up elsewhere in the 2H23 (e.g., Commercial Solutions, and sell out in Learning & Development),” Teixeira opined.

“While investors may just ‘wait-and-see’ given uncertainty over the trajectory of the consumer from here, we think current valuation is too cheap to ignore,” the analyst summed up.

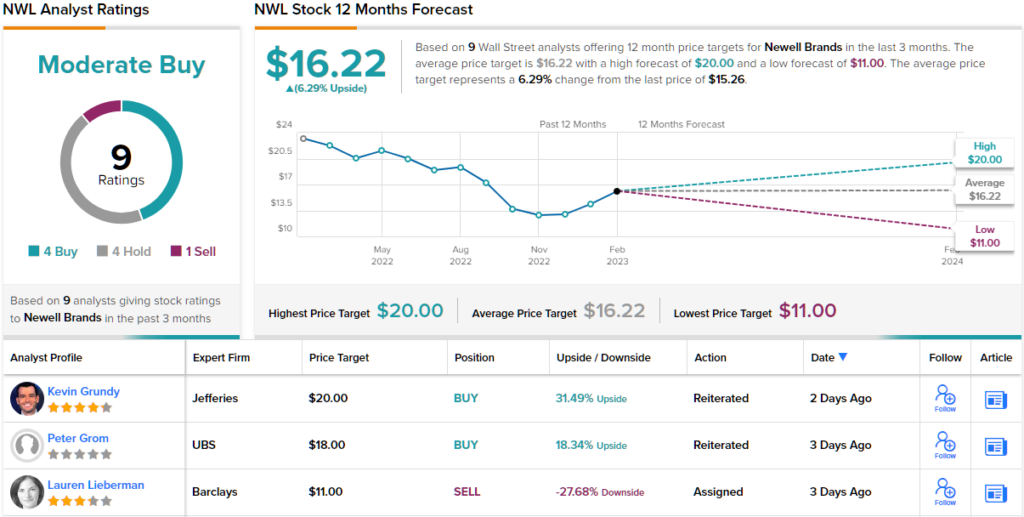

In Teixeira’s view, Newell’s opportunities are worth an Overweight (i.e. Buy) rating, and her $18 price target suggests it has room for 18% share appreciation in the year ahead. (To watch Teixeira’s track record, click here)

Overall, Newell Brands has 9 recent reviews from the Wall Street analysts, and these reviews are split 4 each to Buy or Hold, with 1 to Sell – all adding up to a Moderate Buy consensus rating. (See NWL stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.