American ingenuity has long been the driving force behind the US economy, and few sectors embody this better than biotech. With over 500 biotech firms operating in the US, developing new medical technologies, drug therapies, surgical instruments, and techniques – the list is only limited by imagination.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

These brilliant vistas come with risks, though, including biotech’s famously high overhead costs, its long lead times to new product introduction, and the burden of regulatory requirements and approvals. The potential rewards are real, but this is a sector for risk-friendly investors.

Investors like Joseph Edelman. Edelman is a veteran hedge fund manager, who since 1999 has grown his Perceptive Advisors firm from $6 million in seed money to more than $8 billion in assets under management today. Edelman has always been willing to bet on scientific innovation, and his firm has long focused its investments on the biotech sector.

Edelman has recently been loading up on the small- and mid-cap biotech firms that Perceptive Advisors favors. He’s been buying large tranches of stock in these companies this year, establishing himself as a major shareholder and owner.

His choices are an interesting set, and should draw investors’ attention, so we’ve opened up the TipRanks database to pull up details on two of them. Here they are, presented along with commentaries from the Street’s analysts.

CymaBay Therapeutics (CBAY)

We’ll start with CymaBay Therapeutics, a company specializing in chronic liver diseases. CymaBay is currently in the human clinical trial stage, and investor interest is primarily focused on its leading drug candidate, seladelpar. This new drug is being studied concurrently for potential treatments of primary biliary cholangitis (PBC), non-alcoholic steatohepatitis (NASH), and primary sclerosing cholangitis (PSC), which are all serious chronic liver diseases. Currently, there is no effective approved treatment for each of these conditions.

Seladelpar offers potential to fill that treatment gap. The drug, which has both Breakthrough Therapy and Orphan Drug designations from the FDA, is an orally dosed peroxisome proliferator-activated receptor δ (PPARδ) agonist, a drug specially designed to treat autoimmune conditions of the liver. The drug is undergoing early stage clinical trials in the treatment of NASH and PSC, but its ‘main event’ is its indication against PBC.

CymaBay recently completed the ENHANCE study, a Phase 3 trial evaluating seladelpar as a treatment for PBC, and published results, announced earlier this month, showed efficacy and safety results in a 3 month study. The results were positive, with 78.2% of patients achieving the composite endpoint at a 10mg dose and 57.1% at 5mg. Two secondary endpoints also showed clinically significant results.

The next catalyst for seladelpar will be the RESPONSE study, which is another Phase 3 trial evaluating seladelpar’s safety and efficacy in the treatment of PBC. This trial spans over 52 weeks, providing longer-term data. Currently, the study has 193 enrolled patients, and the release of top-line data is expected in 3Q23.

As PBC patients complete the RESPONSE study, they are being rolled over to the ASSURE trial, a Phase 3 open-label, long-term trial of seladelpar, with the intent to collect definitive data that will support registration for regulatory approval. There are currently more than 200 patients enrolled in the ASSURE study.

A biotech with a promising drug candidate and exciting catalysts on the horizon is bound to turn heads, and Joseph Edelman is keeping a close eye on CymaBay. In fact, Perceptive Advisors has already scooped up 4,569,969 shares of the company this year, bringing their total investment in CymaBay to 5,278,962 shares worth $52.1 million. This means the fund now owns a hefty 5.6% stake in the firm.

Edelman is not the only bull on CBAY. Piper Sandler’s 5-star biotech expert Yasmeen Rahimi has also given CBAY her approval, and in her comments draws particular attention to RESPONSE as the key catalyst for investors to watch.

“We maintain our conviction that 52-week RESPONSE is one of the most de-risked late-stage readouts of the year and think Street may be under-appreciating seladelpar’s market opportunity in PBC. Thus, CBAY continues to be one our best ideas as we anticipate upward momentum in the stock heading into data and post-readout,” Rahimi opined.

Along with these comments, Rahimi gives CBAY an Overweight (i.e. Buy) rating, and her price target, set at $19, implies an 92% upside for the year ahead. (To watch Rahimi’s track record, click here)

Overall, all 10 of the recent analyst reviews on this stock are positive, showing that the bulls are out in force – and giving CBAY a unanimous Strong Buy consensus rating. The stock is selling for $9.87 and its $13.89 average price target suggests a 12-month upside potential of ~41%. (See CBAY stock forecast)

Cerevel Therapeutics (CERE)

The next Edelman choice is Cerevel, a company established in 2018 that specializes in the field of neuroscience. Cerevel’s focus is on the treatment of various neurological disorders, including psychosis associated with schizophrenia or Alzheimer’s disease, Parkinson’s disease, and epilepsy. Each of these conditions affects the central nervous system in a unique way, and Cerevel is leveraging its expertise in advanced biochemistry, neurocircuitry, and central nervous system receptor pharmacology to drive the discovery and development of new drug therapies in the field of neurology.

Currently, Cerevel has 10 ongoing research tracks, including 4 at preclinical stages and 6 at various stages of human clinical trials. Two drug candidates, emraclidine and tavapadon, are leading the pipeline and deserve a second look from investors. Emraclidine shows potential as a treatment for psychosis, while tavapadon is being developed for Parkinson’s disease. Each is the subject of multiple trials, giving the company plenty of shots on goal.

The most likely shot, the center forward charging the net, is the set of emraclidine trials, led by the Phase 2 EMPOWER-1 and EMPOWER-2 trials of the drug as a treatment for schizophrenia and related psychosis. In these trials, the drug is under study as a once-a-day dose without need for titration, a potential advance in schizophrenia treatment, as schizophrenic patients are known for their frequent inability or unwillingness to adhere to medication instructions. Data for EMPOWER-1 and -2 are expected for release in 1H24. Emraclidine is also the subject of a 52-week open-label extension study, EMPOWER-3, for which enrollment is continuing.

In an additional trial, demonstrating emraclidine’s flexibility, Cerevel initiated a Phase 1 study in 4Q22 to assess the safety, tolerability, and pharmacokinetics of emraclidine in the treatment of psychosis induced by Alzheimer’s disease. Notably, this indication has received Fast Track designation from the FDA.

In another significant development, Cerevel is studying tavapadon as a treatment for Parkinson’s disease. This drug, which is a D1/D5 partial agonist, is currently undergoing evaluation in three Phase 3 trials, namely TEMPO-1, TEMPO-2, and TEMPO-3, along with an open-label extension study, TEMPO-4. Tavapadon is being assessed as both a monotherapy and an adjunctive treatment in combination with L-dopa. Data from TEMPO-1 and TEMPO-2 trials are expected to be released in 2H24, and data from TEMPO-3 is anticipated in mid-2024.

Once again, Joseph Edelman is attracted to a biotech with plenty of upcoming catalysts. He owns 6.4% of this company, or 10,088,385 shares worth $282.4 million. This stake includes the 3,576,658 shares he has bought so far this year.

Also bullish is Stifel analyst Paul Matteis, who writes of the company: “Ultimately what’s most important for CERE is that the Emraclidine pivotal program remains on track for 1H24 readouts… Meanwhile, while less important to our thesis, tavapadon readouts are now in 2024, as is the Dementia Related Apathy readout (initially guided for 1H23, now 2H24). The way this sets up, however, assuming no more delays we may get 7 clinical readouts in 2024, making that a huge year for CERE, and again the majority of the valuation remains emraclidine which is on track.”

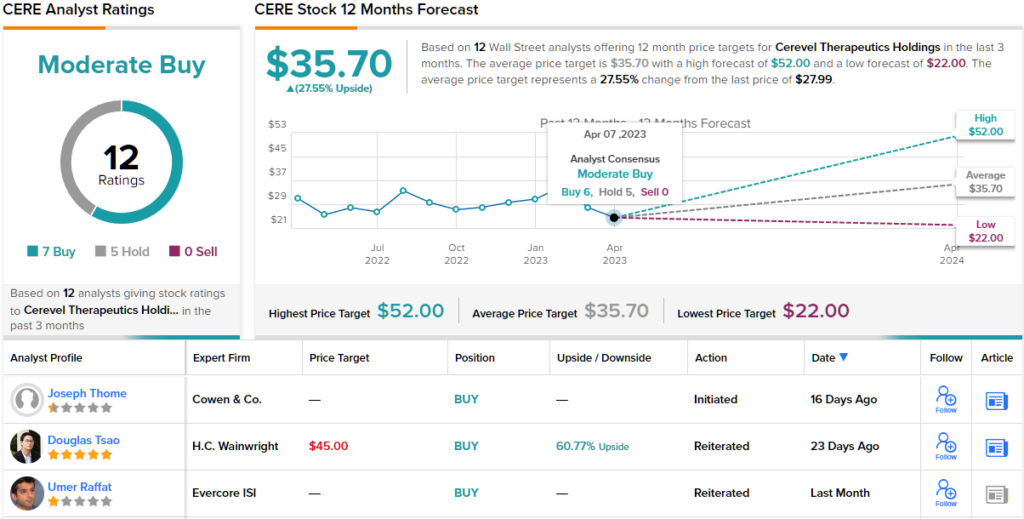

Based on that stance, Matteis feels confident to give CERE shares a Buy rating and a $52 price target that indicates the extent of his confidence – projecting an 86% one-year upside potential. (To watch Matteis’ track record, click here)

Looking at the consensus breakdown, 7 Buys and 5 Holds have been published over the last three months. Therefore, CERE gets a Moderate Buy consensus rating. The current trading price is $27.99 and the average target of $35.70 suggests ~27.55% one-year upside from there. (See CERE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.