It’s hardly an argument anymore – electric vehicles (EVs) are the future and are expected to be increasingly visible on the roads over the next several years.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

That said, recent times have seen this fledgling industry challenged; the tough economic backdrop has made for a difficult operating environment amid signs of waning demand. Not to mention, there’s plenty of competition, with legacy OEMs and new startups alike, vying for a piece of the cake. But that, in turn, opens up opportunities for investors, both for the casual one and the big fish.

Hardly any fish come bigger than Israel Englander. The Millennium Management founder and CEO oversees $58 billion in assets and has a net worth of 11.8 billion, and its looks like the billionaire has been busy loading up on some EV stocks recently – specifically on shares of the undisputed heavyweight of the sector and the company seen by many as its main challenger – Tesla (NASDAQ:TSLA) and Rivian (NASDAQ:RIVN), respectively.

So, let’s see why Englander finds them both appealing right now. At the same time, we ran these tickers through the TipRanks database, to get a wider feel for general Street sentiment toward these names. Let’s see what the data and some analyst commentary show us.

Tesla

Say EVs, then naturally Tesla is the first name that comes to mind. This is the industry trailblazer, the company that changed the game and remains at the forefront of the EV revolution.

Say what you like about Elon Musk, EVs probably would not be the talk of the town without the Tesla CEO’s vision and drive. Musk forged ahead with his world domination plans even as the industry laughed off his seemingly ridiculous ambitions of turning the auto industry on its head. But no one’s laughing now, with Tesla valued above any other automaker, even though its sales are still nowhere near the industry’s true big hitters.

And while Tesla’s rise once seemed unstoppable, the company has had its fair share of issues recently, not least a dud of a Q3 report, which showed the company coming up short on both the top and bottom line. In the quarter, Tesla generated revenue of $23.35 billion, representing an 8.9% year-over-year uptick, yet missing the consensus estimate by $790 million. Auto gross margins (GM ex credits) also disappointed, hitting 16.3%, thereby falling shy of the Street’s 17.6% forecast. The end result was Adj. EPS of $0.66, a figure $0.07 below the analysts’ forecast.

Tesla also issued a warning of difficult times ahead, but Israel Englander evidently has faith in Tesla’s long-term prospects. He bought 407,695 shares in Q3, upping his stake considerably with his total holdings now standing at 523,087 shares. These currently command a market value of $122.66 million.

While Tesla is still seen primarily as an automaker, its ambitions are much bigger than that. The opportunities that lie elsewhere form a major part of RBC analyst Tom Narayan’s bullish thesis and could fuel the company’s next leg of growth.

“We think Tesla could be embarking on a strategic transition from being a car-maker to becoming a tier 1 supplier,” Narayan wrote. “First, we expect all North American automakers to eventually join its Supercharger network. Next, we could envision Tesla selling power electronics to other OEMs like Lucid with Aston Martin or Mercedes with Ferrari. Tesla is the biggest maker of these components in the world. We also could see Tesla selling batteries to other OEMs especially given its 200gwh expansion underway subsidized by the IRA. These efforts could be a profit center or could be sold competitively, so the company can sell FSD (full self-driving), which we think ultimately is the prize.”

These comments underpin Narayan’s Outperform (i.e., Buy) rating on TSLA shares, while his $301 price target makes room for 12-month returns of 28%. (To watch Narayan’s track record, click here)

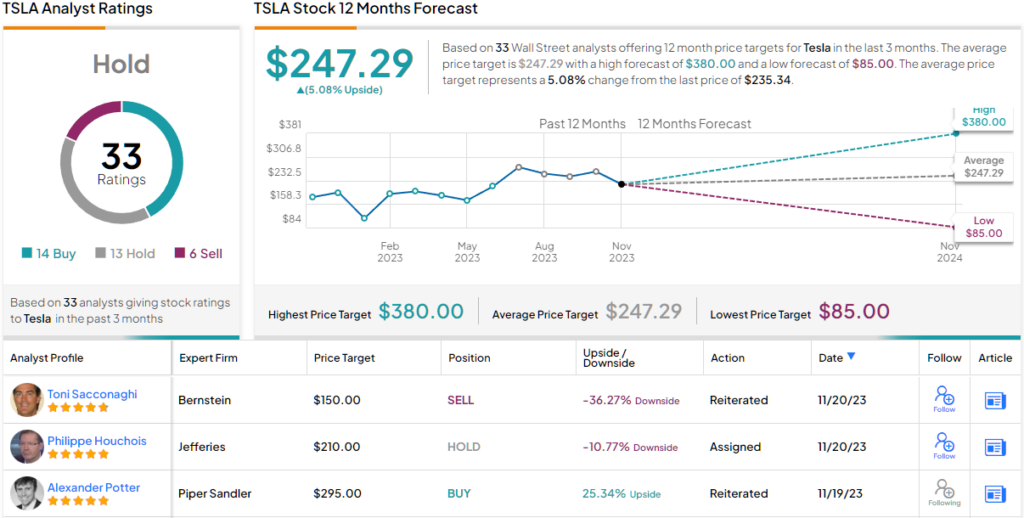

However, not all on the Street are quite as confident on Tesla. Based on a mix of 14 Buys, 13 Holds and 6 Sells, the stock claims a Hold (i.e. neutral) consensus rating. The forecast calls for 12-month returns of a modest 5%, given the average price target stands at $247.29. (See Tesla stock forecast)

Rivian Automotive

There’s no doubt Tesla remains the top player among EV manufacturers, but there’s no guarantee it will maintain its position as the segment leader indefinitely. Several contenders are eyeing its throne, with Rivian being perhaps the most promising among them.

Backed by Amazon and Ford, Rivian made a significant impact when it entered the market at the end of 2021, quickly becoming the largest U.S. company by market capitalization, despite not generating any revenue yet.

However, the company faced production issues and operated in a challenging economic environment with high inflation and interest rates, causing its story to sour, leading to a share price meltdown. Nevertheless, while some other EV startups have failed to recover, Rivian has recently shown concrete signs that it may have turned the corner.

While the broader EV market has experienced declining demand this year, Rivian’s Q3 results indicated the opposite trend as the company delivered 15,564 vehicles, a 23% increase compared to the previous quarter and well above the 6,584 units delivered in 3Q22. The figure also exceeded Wall Street’s expectations of 14,973 units.

Rivian also surpassed expectations both in terms of revenue, reporting $1.34 billion, a 150% year-over-year increase, and beating the forecast by $30 million. Furthermore, the company’s efforts to cut costs and enhance efficiency are yielding positive results. Consequently, the adjusted EPS of ($1.19) exceeded Wall Street’s estimate of ($1.34). Additionally, the EV manufacturer raised its production guidance for 2023, aiming to produce 54,000 units this year, up from the previous target of 52,000 units.

Meanwhile, it appears that Englander is showing confidence in the developing story. He purchased 2,583,728 shares in Q3, bringing his total ownership in Rivian to 4,437,356 shares. At the current share price, these shares are valued at approximately $69.75 million.

The company also gets the support of Truist analyst Jordan Levy, who notes Rivian’s improving fundamentals.

“Through higher volumes, new technology rollouts and supplier cost downs, RIVN has managed to chip away >$100K/vehicle in gross profit losses over the last 12 months,” Levy explained. “While RIVN still has a ways to go before achieving its YE24 positive contribution margin target & street ’24 production estimates likely need to continue to come down, several quarters of strong execution give us heightened confidence in RIVN’s trajectory. Ultimately once the fog of market EV pessimism clears & rate headwinds subside, we expect RIVN shares to begin to more closely reflect the progress the company has & continues to make.”

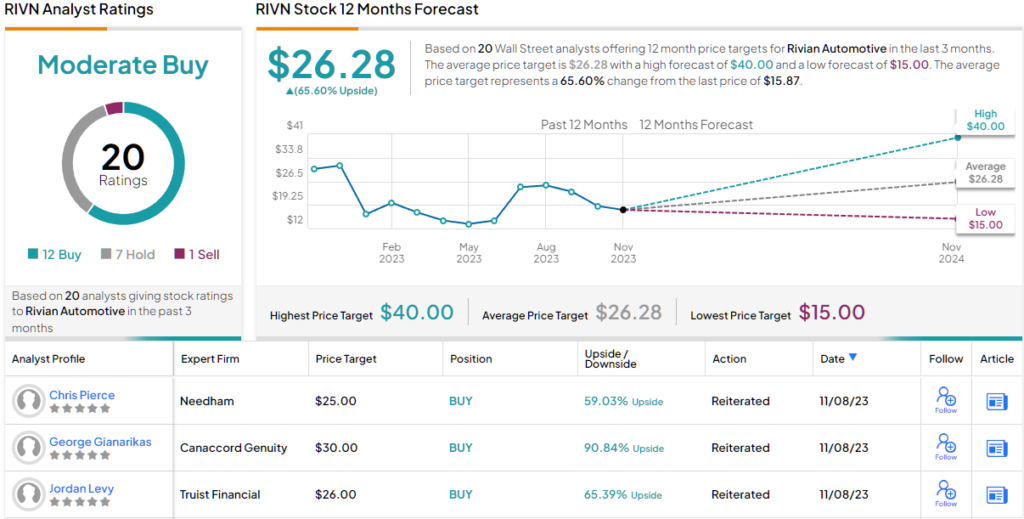

Quantifying his bullish stance, Levy has a Buy rating on RIVN shares backed by a $26 price target. Should the figure be met, a year from now, investors will be pocketing returns of 65%. (To watch Levy’s track record, click here)

Elsewhere on Wall Street, the stock garners an additional 11 Buys, 7 Holds, and a single Sell, for a Moderate Buy consensus rating. The $26.28 average target is just a touch above Levy’s objective and set to generate one-year gains of ~66%. (See RIVN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.