If you’re going to be forever known for one thing, being the ‘man who broke the Bank of England’ is a description many would sign up for. That is how George Soros is regularly introduced, and the story involves how he bet against the British Pound in 1992 and pocketed $1 billion from the trade in a single day.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Of course, Soros’ legendary reputation does not rest solely on that headline-grabbing act, and the billionaire investor has had a decades-long career of almost unmatched investing success. So, when Soros decides the time is right to load up on some equities, it’s only natural for investors to want to see what’s inside his shopping bag.

We’ve taken a step to get that process started and have opened up the TipRanks database to get the lowdown on two of his recent new positions. It’s not just Soros who thinks these names are ripe for the picking right now – both are rated as Strong Buys by the analyst consensus. So let’s take a deeper look and find out why you might want to follow in Soros’ footsteps.

AerCap Holdings (AER)

The first Soros-backed name we’ll look at is global aircraft leasing company AerCap Holdings. With over 1,740 aircraft in its portfolio, AerCap is one of the world’s largest aircraft leasing companies, serving more than 300 customers in over 80 countries. The company’s portfolio consists of a wide range of aircraft types, including new and used commercial passenger and cargo aircraft which are leased to leading airlines including Emirates, Etihad, El Al and South African Airways, amongst many others. The company’s offerings also include over 300 helicopters and a fleet of more than 900 owned, managed and serviced engines.

Over the past year, quarterly revenues have been steadily rising and that was the case again in the most recently reported quarter – for 1Q23. Revenue rose 4.5% year-over-year to $1.87 billion, beating the Street’s call for $1.77 billion. Likewise, on the bottom-line, Adj. EPS of $2.34 came in above the $2.03 forecast. AER also authorized a new $500 million share repurchase program and noted that 99% of its new aircraft order book are placed through 2024.

This must have all been welcome news for Soros. During Q1, the billionaire opened a new position in AER by purchasing 535,425 shares. At the current share price, these are worth over $30 million.

Scanning the Q1 print, Barclays analyst Mark DeVries also finds plenty to like here.

“1Q results showed the positive momentum of AER’s leasing business and its capital return strategy (selling assets at +18% GOS and buying back stock at ~15% discount to book value),” the 5-star analyst said. “Improving global air traffic and an aircraft supply shortage all point to a continuation of positive trends for the air lessors, which should result in improving lease rates and higher GOS margins. Management updated its FY EPS guide to the high end of the previous range $7.00-7.50/sh (ex GOS), which we continue to believe is on the conservative side. With the shares trading at ~0.80x P/B, we continue to find the risk/reward attractive…”

With an outlook like that, it should be no surprise that DeVries sides with the bulls on this stock. His comments come with an Overweight (i.e. Buy) rating, and a $78 price target that indicates potential for ~39% share growth on the one-year time horizon. (To watch Devries’ track record, click here)

DeVries’ thesis gets the Street’s full backing. All 5 recent analyst reviews on AER are positive, making the consensus view here a Strong Buy. Going by the $75.40 average target, investors will be sitting on gains of 34% in 12 months’ time. (See AER stock forecast)

Teck Resources (TECK)

Next up on our Soros-endorsed list is Teck Resources, a leading Canadian mining and mineral development firm. The company produces coal, copper, zinc, and other metals and has operations and projects in Canada, the United States, Chile, and Peru. Teck has shown a commitment to sustainability and, in recent years, made significant investments in renewable energy, setting a goal to be carbon neutral by 2050.

Despite being one of the largest diversified resource companies in the world, Teck felt the impact of lower prices, soft sales of copper and zinc, and higher expenses in its most recently reported quarter.

In Q1, revenue fell by 18% year-over-year to C$3.79 billion, while missing the consensus estimate by C$240 million. The company just fell short of expectations on the bottom-line, delivering an adjusted profit of C$1.81 per share vs. the Street’s C$1.82 estimate. On the other hand, the company stuck to its previously announced 2023 production guide.

In any case, Soros must like what’s on offer here. During Q1, he opened a new position in TECK, purchasing 497,854 shares, which are currently valued at ~$21.67 million.

Adding to recent developments, a consortium led by Pierre Lassonde, an experienced Canadian mining veteran, proposed last week to buy Teck Coal, the firm’s coal division. In an interview, Lassonde said Teck is keen on moving forward with the proposal and that should happen over the next 8-12 weeks.

Teck has yet to respond to the news, but mulling over the scheme, Morgan Stanley analyst Carlos De Alba believes that, if confirmed, the proposal “highlights the attractiveness of Teck’s coal business” and thinks the offer compares well to a prior proposal.

“As we mentioned before,” the 5-star analyst reminded investors, “the complexity and long duration of the previously proposed coal spin-off, which kept the two businesses interlinked for several years, resulted in mixed support from investors. We believe an outright sale of the coal business could be viewed more positively by investors, as it would provide a clean exit from coal and result in Teck being a pure-play base-metals company with high growth potential, in particular for copper.”

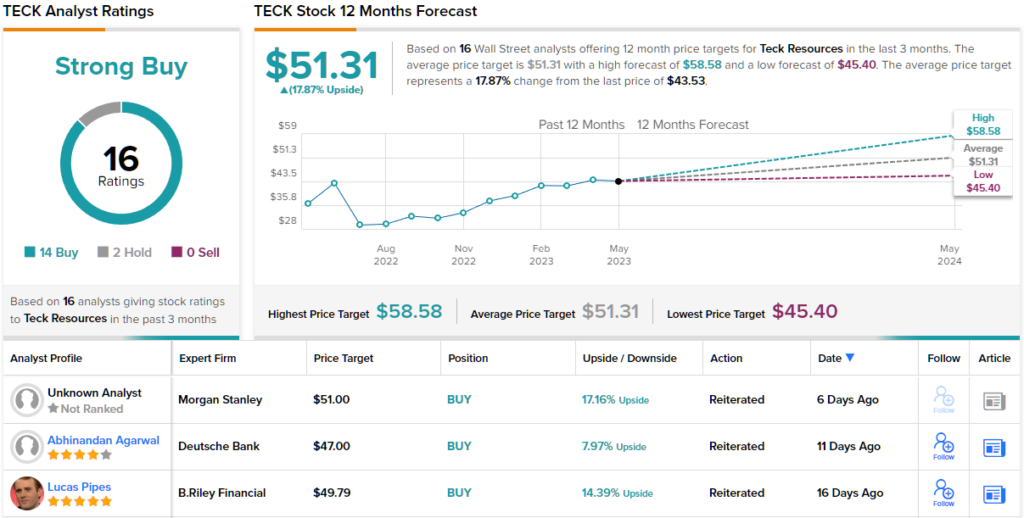

Whether that happens or not, remains to be seen. For now, De Alba rates TECK shares an Overweight (i.e., Buy) while his $51 price target implies one-year share appreciation of 17%. (To watch De Alba’s track record, click here)

Looking at the ratings breakdown, based on 14 Buys vs. 2 Holds, the analyst consensus rates TECK a Strong Buy. The Street’s $51.31 average target is almost identical to De Alba’s objective. (See TECK stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.