It must have sounded like a good idea at the time, but Anheuser-Busch’s (NYSE:BUD) decision to run a promotional campaign for its Bud Light beer with the help of transgender ‘influencer’ Dylan Mulvaney backfired spectacularly. Conservative America did not like that idea at all, and decided to boycott the drink, thereby no longer making it the US’s best-selling beer.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

As sales plummeted in the wake of the controversy, BUD shares went into a tailspin, falling by 20% in May with the company also laying off over 300 U.S. employees as a result.

Nevertheless, despite the drop in US sales it’s the sort of hoopla that is confined to the domestic market and a strong performance in other markets managed to offset some of the US slack. In total, organic volume in Q2 fell by 1.4% year-over-year with the North American drop of 14% countered by robust growth in the Asia Pacific region.

Meanwhile, one beer lover has evidently decided to put the well-known advice of his friend to good use. Bill Gates and Warren Buffett are close buddies, and it looks like the Microsoft founder has embraced Buffett’s famous ‘be fearful when others are greedy, and greedy when others are fearful’ quote.

During the second quarter, his Bill & Melinda Gates Foundation Trust initiated a new position in BUD, acquiring 1,703,000 shares. As of now, these shares hold a market value of approximately $95 million.

Morgan Stanley analyst Sarah Simon is also backing the drinks giant and notes that success elsewhere offers protection from the negative US situation.

“After successful execution through Covid, 2023 has seen ABI suffer substantial market share loss in the US, driven primarily by consumer boycotts of its Bud Light brand,” Simon said. “While this makes for very negative headlines, ABI’s exposure to emerging markets limits the impact of the US share loss. After one-off costs in 2023, we see profitability growth resuming in 2024, with strong cash flow growth driving leverage to the target 2.0x, allowing for both an increase in the payout ratio as well as the resumption of share buybacks from 2026. Current valuation fails to reflect this upside, in our view.”

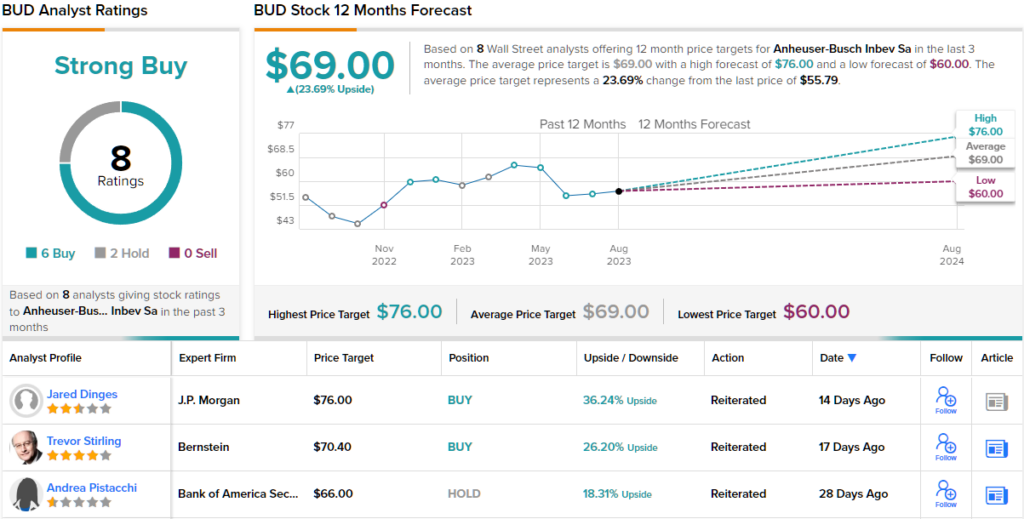

Accordingly, Simon has an Overweight (i.e., Buy) rating for the shares to go alongside a $68.50 price target. The implication for investors? Potential upside of 23% from current levels. (To watch Simon’s track record, click here)

Most other analysts echo Simon’s sentiment. 6 Buys and 2 Holds add up to a Strong Buy consensus rating. Given the average price target of $69, the upside potential comes in at ~24%. (See BUD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.