Beyond Meat stock (NASDAQ:BYND) may unfortunately be on a trajectory toward $0. Lacking a clear catalyst for a turnaround, the stock’s value could continue to diminish. It has dropped from ~$235 in July 2019 to just $8.35 today, with its remaining value likely to gradually evaporate. In this article, we explore the challenges that Beyond Meat has faced—challenges that appear likely to lead to further deterioration of shareholder value over time. Consequently, I hold a bearish stance on the stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

What’s Wrong With Beyond Meat?

Given such terrible share price losses, one can only wonder what’s wrong with Beyond Meat. I mean, on the surface, it may look like the company saw some commercial success. In recent years, Beyond Meat managed to partner with major names in the QSR (quick-service restaurant) space, including McDonald’s (NYSE:MCD), KFC, Taco Bell, and Pizza Hut (NYSE:YUM).

However, these high-profile collaborations failed to translate into a significant uptick in Beyond Meat’s sales. Notably, Beyond Burger’s trial run at McDonald’s failed to garner enough interest for a nationwide, let alone global, expansion. Taco Bell’s foray into plant-based meat products, predominantly featuring Beyond Meat, received “mixed reviews” and showed lackluster sales. Meanwhile, KFC discontinued its “Beyond Chicken” offering.

This highlights a crucial realization: Beyond Meat attained mainstream exposure and received an extensive opportunity from leading QSR brands, only to falter. The fundamental issue lies in a simple explanation—there is an insufficient demand for “fake” meat. While the company enjoyed a transient trendiness, it wasn’t more than a fad that quickly dissipated.

Disappointing Sales, Disastrous Losses

The narrative is vividly illustrated in Beyond Meat’s disappointing sales trajectory, preventing the company from realizing substantial economies of scale and expanding its profit margins, ultimately resulting in significant losses.

To provide context, Beyond Meat experienced a peak in sales during Fiscal 2021, reaching $464.7 million, buoyed temporarily by most of the aforementioned partnerships taking place at the time. However, with these partnerships quickly flopping, Fiscal 2022 witnessed a decline in sales, as they fell to $418.9 million. The current fiscal year paints an even bleaker picture, with last-12-months (LTM) sales as of Q3 plummeting to $349.6 million.

With Beyond Meat failing to achieve scaling economics, which could only be driven by higher sales, its margins never improved. In fact, rather than improving, the company’s margins have worsened due to declining sales, driving them into negative territory. Gross margins, which stood at 25.2% by the close of 2021, cratered to -5.7% by the close of 2022 and persist in negative territory. Remarkably, Beyond Meat now incurs greater losses for each additional patty sold.

When factoring in additional expenditures, encompassing administrative, marketing, R&D, and other capital expenditures, the company is bleeding money. Free cash flow for Fiscal 2021 and Fiscal 2022 amounted to negative $437.3 million and negative $393.5 million, respectively. Despite recent efforts by management to trim expenses, the LTM free cash flow remains deeply negative at $151.1 million. In the meantime, there is no plan or catalyst on the horizon that indicates a potential rebound in sales.

Why the Stock is Likely to Reach $0

If negative gross margins don’t already make a good reason for why the stock is likely to go to $0, the more technical explanation is that continuous losses will ultimately completely erode shareholders’ equity. Beyond Meat’s predicament, characterized by persistent losses and reliance on new capital injections, manifests in the following compelling observations:

- From the company’s initial public offering to its latest financial report, its balance sheet has endured a severe downturn, witnessing total debt surge from nearly $31 million to a problematic $1.22 billion.

- Simultaneously, the company’s outstanding share count has surged from 58.1 million to 64.5 million due to sustained dilution. The company’s ATM equity issuance program is set to sustain this trend.

- Beyond Meat’s cash reserves have fallen from $1.13 billion in Q1-2021 to a mere $217.5 million as of Q3 2023.

Even in the hypothetical scenario where management succeeds in mitigating negative free cash flow, the impending need for capital injection looms large.

I mean, how is it going to keep paying its employees, let alone repay its borrowings? At this point, who wants to invest in a business with negative gross margins and declining sales? Nobody. Even if there were daring investors willing to take the risk, it would merely offer Beyond Meat a short-term lifeline before the company finds itself in the same predicament.

Is BYND Stock a Buy, According to Analysts?

Turning to Wall Street, Beyond Meat stock features a Moderate Sell rating based on five Hold and five Sell ratings assigned in the past three months. The average BYND stock forecast of $5.83 implies 30.2% downside potential.

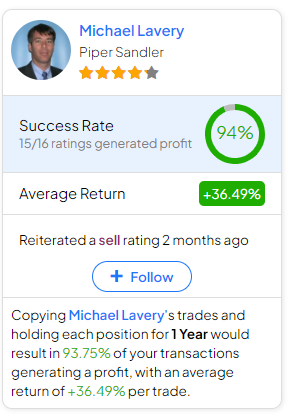

If you’re wondering which analyst you should follow if you want to buy and sell BYND stock, the most accurate analyst covering the stock (on a one-year timeframe) is Michael Lavery from Piper Sandler, with an average return of 36.49% per rating and a 94% success rate. Click on the image below to learn more.

The Takeaway

Overall, Beyond Meat’s downward spiral appears relentless, with the stock possibly heading towards $0. Despite high-profile partnerships, the company failed to translate exposure into sustained sales, facing lackluster demand for plant-based products.

Disappointing sales trajectories, disastrous losses, and negative gross margins signal a troubling future. With escalating debt, dilution, and dwindling cash reserves, the outlook is bleak. Without a clear catalyst for recovery, the path to potential insolvency seems inevitable, reinforcing my bearish stance on Beyond Meat’s prospects.