Few things fire up the imagination of wealth better than a gold mine. After all, while money doesn’t grow on trees, we can actually dig it up out of the ground. Our wealth-related metaphors often revolve around gold, with phrases like ‘things as good as gold’ and ‘an asset that’s like a gold mine.’ Indeed, gold stands as the ultimate symbol of riches and prosperity.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

While owning a gold mine might be a distant dream for many, investing in the stock of a gold mine presents an entirely feasible opportunity. Mining companies form an important segment of the stock market. They will focus on different resources, some seeking gold, some silver, some extracting base metals like copper or zinc. All can generate profits when managed effectively, and investors can find sound choices throughout the mining sector.

But we’re talking about gold. Barclays, the London-based banking giant, has released a report focusing on the North American mining sector, and particularly on American gold miners. The firm’s 5-star analyst, Matthew Murphy, notes the headwinds – a slow recovery in China, a downward trend in the Eurozone – but adds that he expects US mining firms to do well, supported by continued demand for gold.

“We expect most of our companies to have slightly better results in Q2, even amidst some deterioration of commodity prices. We remain more constructive on gold than copper as economic deceleration continues,” Murphy wrote.

At the bottom line, Murphy has several specific recommendations when it comes to gold mining firms. We’ve delved into the TipRanks database to uncover details on two of them, both sporting ‘Buy’ ratings and boasting double-digit upside potential.

Newmont Mining (NEM)

We’ll start with Newmont Mining, one of the world’s largest producers of gold. The company boasts a $34 billion market cap, and while it also produces silver, copper, lead, and zinc, its main activity is gold mining. Newmont, which is based in the state of Colorado, is active across both North and South America, and also has operations in Australia and the West African nation of Ghana.

While Newmont was the world’s largest gold producing company in 2022, in the most recently reported quarter, 2Q23, it experienced a 17% decrease in gold production compared to the previous year. This decline was primarily caused by the suspension of operations at the Penasquito mine in Mexico due to a workers’ strike. Additionally, the Cerro Negro mine in Argentina and the Akyem mine in Ghana also underperformed, contributing to the weaker-than-expected results.

As such, the company missed expectations on both the top-and bottom-line in Q2. Revenue fell by 12.4% year-over-year to $2.68 billion, in turn missing the consensus estimate by $220 million. Adj. EPS of $0.33 came in some distance below the $0.47 forecast.

The shares fell by 6% in the subsequent session, amounting to stock’s steepest daily drop since July 2022.

Nevertheless, Newmont is actively moving to expand its activities, and to that end, in May of this year, the company entered an agreement to acquire Australia’s Newcrest Mining Limited for about $19.5 billion. Newmont will acquire 100% of Newcrest’s shares and the move will give Newmont control of Newcrest’s portfolio of assets. The transaction is expected to close in Q4 and the combined entity will have the world’s largest concentration of Tier 1 mining operations.

Looking ahead, Barclays’ Murphy is impressed by the potential inherent in Newmont, and writes of the company’s prospects, “We forecast NEM’s average production to increase by ~40% for gold to 8.9Mozpa and ~300% for copper to ~390Mlbpa over the next five years, and expect nearly two-thirds of gold production (5Moz) to come from 10 Tier 1 assets (before considering any portfolio rationalization). We expect cash costs and AISC to increase marginally post-deal (~2-3%) to ~$740/oz and ~$1,015/oz, respectively, but to improve with time as NEM’s Full Potential optimization efforts are implemented.”

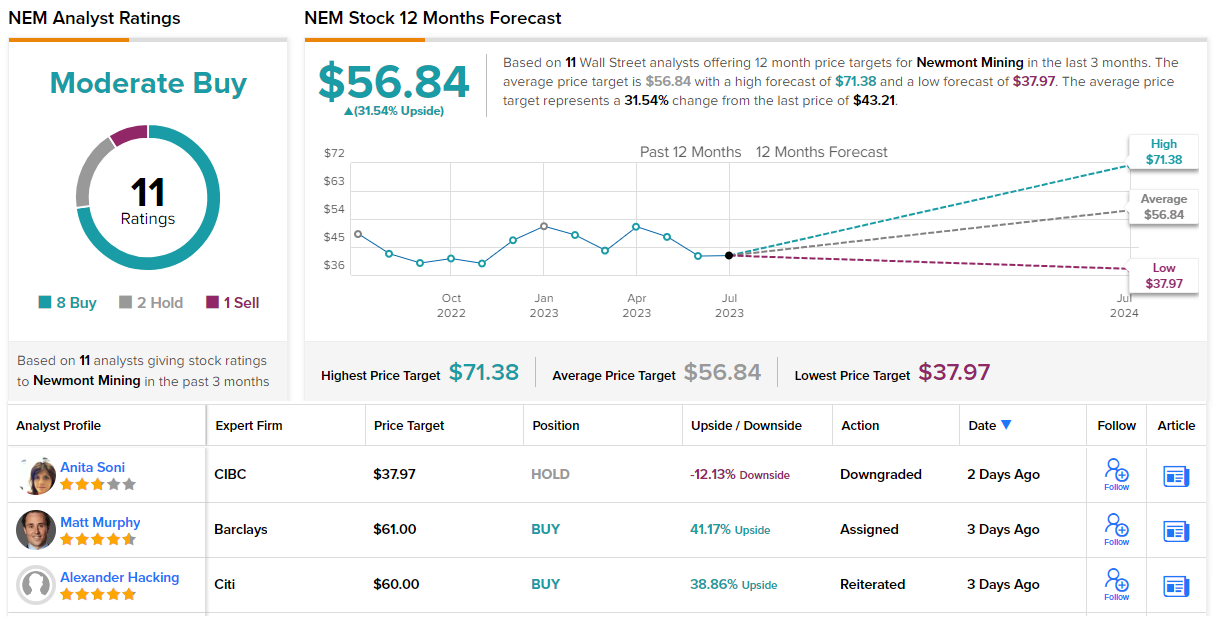

Murphy goes on to rate the shares as Overweight (a Buy), and he sets a $61 price target that implies a one-year gain of 41%. (To watch Murphy’s track record, click here.)

Wall Street is generally bullish on Newmont, although some analysts have reservations. The stock has 11 recent analyst reviews, breaking down to 8 Buys, 2 Holds, and 1 Sell, for a Moderate Buy consensus rating. The shares are selling for $43.21 and the $56.84 average price target suggests a 12-month upside potential of 31%. (See NEM stock forecast)

Agnico Eagle Mines (AEM)

For the second Barclays mining pick we’re looking at, we’ll turn to Toronto-based Agnico Eagle Mines. The firm has been in operation since 1957 and controls a series of mining projects in Canada, Mexico, Finland, and Australia, along with high-quality development projects in the US and Colombia. Agnico produced more than 3.1 million ounces of gold in 2022, at a production cost of $843 per ounce.

That production cost is an important metric for investors to consider – especially when set against the trading price of gold, which was near $1,800 per ounce at the end of last year. Gold is currently priced at ~$1,961 per ounce on the commodity markets.

Agnico will report Q2 earnings on Wednesday (July 26), but we can look to the Q1 results for a feel for its financials. Production numbers remained strong in the quarter and the company generated 812,813 ounces of gold, with total cash costs per ounce of $832 and an all-in sustaining cost (AISC) of $1,125 per ounce. Based on this, the company realized $1.51 billion in total revenues, beating the forecast by $21.6 million. EPS reached $0.58, also coming in ahead of expectations – by $0.09.

The company’s operating cash flow in the quarter came to $1.30 per share, and Agnico declared a 40-cent common share dividend for Q1. Agnico’s current dividend yields 3.2%, and the company has been keeping up regular payments since 1983.

Looking ahead, Agnico expects full-year gold production to reach between 3.24 million and 3.44 million ounces, with an AISC between $1,140 and $1,190.

In his coverage of this stock, analyst Matt Murphy sees several paths toward continued profitability, mainly from the Canadian mining operations. Murphy says of Agnico, “While we model the current plan for Canadian Malartic and Odyssey as a base case, we have played with nearby lower grade open pittable ore and further away (regional) higher grade underground reserve addition scenarios. Our preliminary estimate is that these scenarios could add some $1-3/sh to our NAV (3-9%), with low-grade open pits actually offering more upside under our current assumptions. We could also see a scenario with mine-life extension at the depth of East Gouldie; however, with a life already extending to 2042 and the exploration expense, that might add less value at present.”

Quantifying his stance, Murphy rates the stock as Overweight (Buy), and his price target of $61 suggests the stock will gain 17% in the coming months.

This stock has a Strong Buy rating from the analyst consensus, and it’s unanimous, based on 6 positive reviews in recent weeks. The shares have an average price target of $64.63 and a trading price of $52.09, implying an upside of 23% on the one-year horizon. (See AEM stock forecast)

To find good ideas for stocks recommended by top-performing analysts, visit TipRanks’ Analysts’ Top Stocks.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.