Let’s begin on a positive note: apparently, a broad financial crisis has been averted; we will not see another Lehman go down. Indeed, there are still many vulnerabilities within the smaller banks that will probably depress the value of their shares for months to come. But thanks to decisive action by the regulators, and the helpful swiftness of JP Morgan (JPM) in taking over troubled banks, markets now seem convinced that the financial system will stand even if some bricks fall out.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

As banking systems run on trust (and liquidity, but that’s for later reference), this conviction is as good as gold. However, “all is not well in paradise.” Let’s dwell a little on the problems of the regional banking turmoil and their effects on stock investing.

How Did We Get into This Mess?

Silicon Valley Bank, Signature Bank, and First Republic Bank have all collapsed within less than two months. When adjusted for inflation, their total assets exceeded those of the 25 banks that failed at the height of the financial crisis in 2008/09 – and that’s after discounting for the decline in the value of those assets, which was one of the main culprits for their demise.

While some of the troubled lenders have brought the suffering on themselves through poor risk management, others were innocent bystanders, hit by the 90 mph fastball of rising rates.

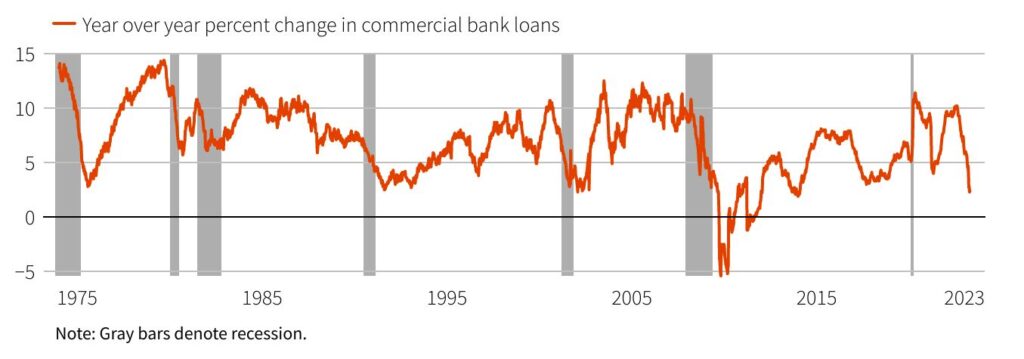

Not only has the Federal Reserve hiked its interest rates by a large percentage, but at an outstanding speed – the rates jumped by 5% within little more than a year. This meteoric surge has left smaller, less capitalized lenders with little chance to adjust. Their longer-duration (i.e., more sensitive to rate increases) assets fell in value. At the same time, shorter-duration liabilities didn’t decrease as much, leaving them with depleted equity.

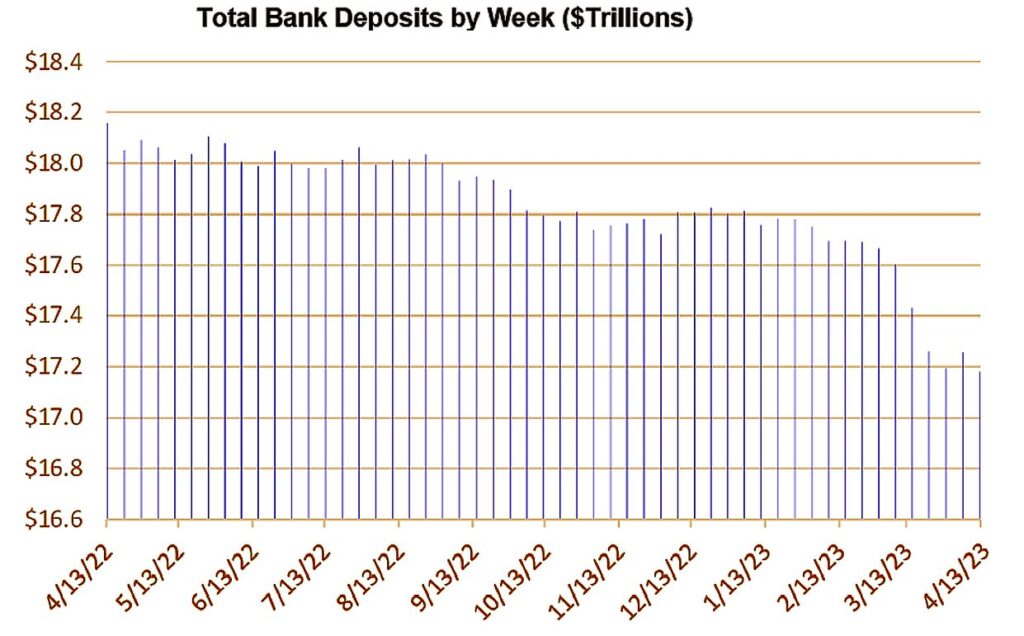

The deposits had been fleeing the banking system even before the triple downfall of SVB, Signature, and FRB, but their collapse considerably hastened the process. As interest rates rose, savers discovered attractive options elsewhere; banks, who suddenly became risky in the eyes of their clients, couldn’t match the yields offered by virtually risk-free Treasuries or money market funds. A hit to sentiment posed by the turmoil in regional banks accelerated the deposit flight from smaller financial institutions, exacerbating the liquidity and solvency issues.

Even if the Federal Reserve has delivered its last hike for this cycle, we haven’t seen the end of banking troubles yet. There’s an issue of commercial real estate unraveling right in front of our eyes as rising interest rates depress the value of the properties, raising the odds of defaults. CRE loans represent about a quarter of U.S. bank loans on average; that figure is higher for regional and local lenders, who are unable to diversify into investment banking or other profitable venues, like large institutions.

Deposit Flight and Credit Crunch Go Hand-in-Hand

Smaller and regional banks play a vital role in the U.S. economy, as they provide most of the lending to all its participants. According to Goldman Sachs (GS) economists, small and medium-sized lenders (those with assets under $250 billion) provide:

- 80% of commercial real estate lending.

- 60% of residential property lending.

- Roughly half of lending to companies and individuals.

Deposit flight and asset-duration mismatches depress banks’ liquidity and threaten their solvency, forcing them to restrict lending to all these entities. Tighter lending and higher cost of financing equal a credit crunch: a situation where individual and corporate access to credit is substantially curtailed. This credit starvation is the main reason economists give a high chance of a recession beginning in the second half of 2023.

The credit crunch means lower consumer credit, which depresses demand and makes funding for companies more scarce. Without access to lending, firms won’t be able to expand or refinance existing loans, which would lead to a rise in default rates. Rising default rates will then haunt the banks’ books, leading to declining asset values and market uncertainty.

Cash-Strapped Small Caps are a No-Go

The immediate investing conclusion that comes to mind is that banking sector troubles are not over. Indeed, it’s probably not a good time to “buy the dip” in regional bank stocks, even if the KBW Nasdaq Regional Banking Index’s 32% year-to-date decline might seem tempting. But that’s not the only verdict; there’s more.

According to Bank Of America (BAC), a recession and a credit crunch could spur the U.S. corporate default rate to 8%, i.e., company debt defaults amounting to about $1 trillion. While this is a worst-case scenario, a credit crunch will certainly lead to higher default rates. While we don’t know how many companies will default, we can establish who is more vulnerable to credit scarcity.

Smaller companies are the first in the line of fire, as they need constant access to credit to continue their activity. With their higher vulnerability to the domestic economy’s health and local consumer demand changes, they are also the first to feel the banks’ lower propensity to lend since they are much riskier customers than large, established firms.

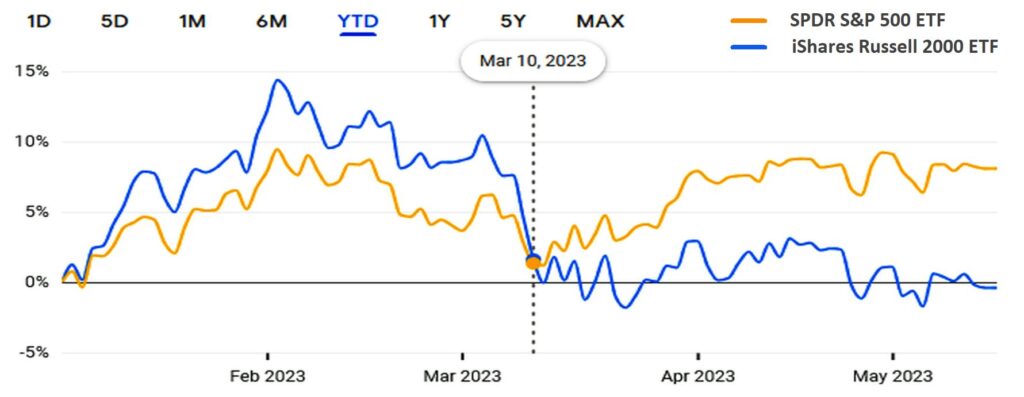

Investors have been decreasing exposure to small-cap stocks since the second half of 2021, but the outflows began in earnest with the onset of the banking turmoil in March. The difference in investor sentiment towards large and small firms can be seen in the performances of the ETFs on the corresponding indexes.

While SPDR S&P 500 ETF (SPY) is up north of 8% year-to-date and almost 7% since the SVB collapse on March 10th, the iShares Russell 2000 ETF (IWM), which follows the small-cap index, is flat YTD and down 2% from the start of the regional banking crisis.

Obviously, if the economy is moving towards a recession, then this is not yet the real “dip” for small caps, as the worst may still be ahead.

Counting the Winners on One Hand

It’s quite clear now that investors should look for stocks of companies with strong cash balances and low debts, which allow them to survive and even grow in difficult financing and economic environments.

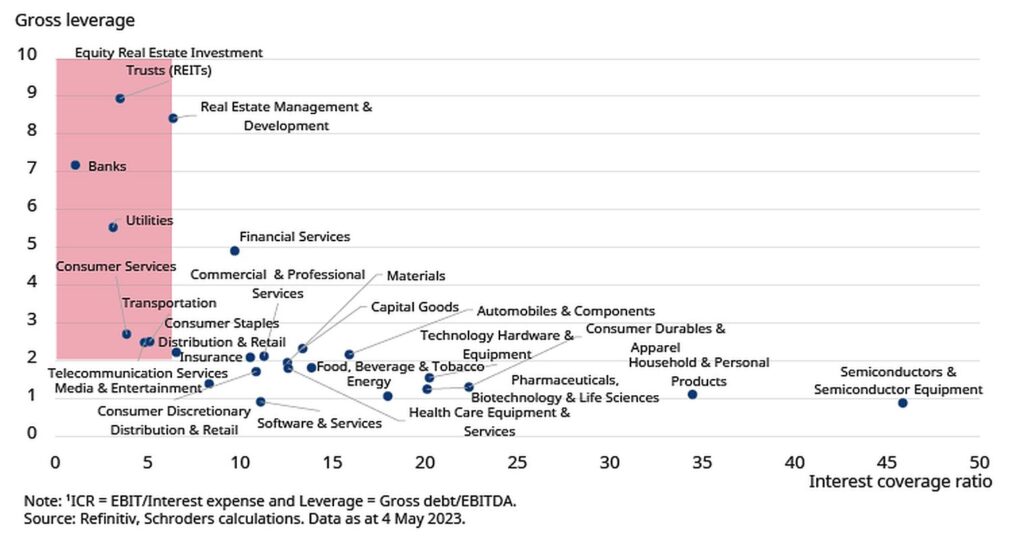

Although companies with stellar cash flows and strong debt profiles can be found in any industry, on average, some S&P 500 (SPX) sectors are more vulnerable than others:

As companies deal with the increased cost of debt in today’s environment, those with greater leverage and/or lower interest coverage ratios may start to feel the strains. Even though the likelihood of ultimate default may be modest, the market separates firms based on relative risk. That means companies with weaker fundamentals – especially if they have higher-than-average valuations – are more vulnerable to sell-offs due to risk-off sentiment.

Since the Federal Reserve is now expected to pause or even stop increasing interest rates, the market’s attention turns to various economic issues affecting companies’ well-being. In a low-growth economic environment, firms that can continue expanding their activity (which is reflected in their revenues and EPS) become increasingly more attractive than their peers. In these circumstances, companies that can sustain earnings growth become a defensive investment.

Growth as a Defensive Investment

Interestingly, while Growth stocks are usually perceived to be riskier since they need constant credit to fuel growth, many companies in this segment are actually way less indebted than their non-technology counterparts. For lack of a better definition, let’s concentrate not on typical “growth” companies—non-profitable cash-burners promising high future returns—but on those who are also growing their earnings.

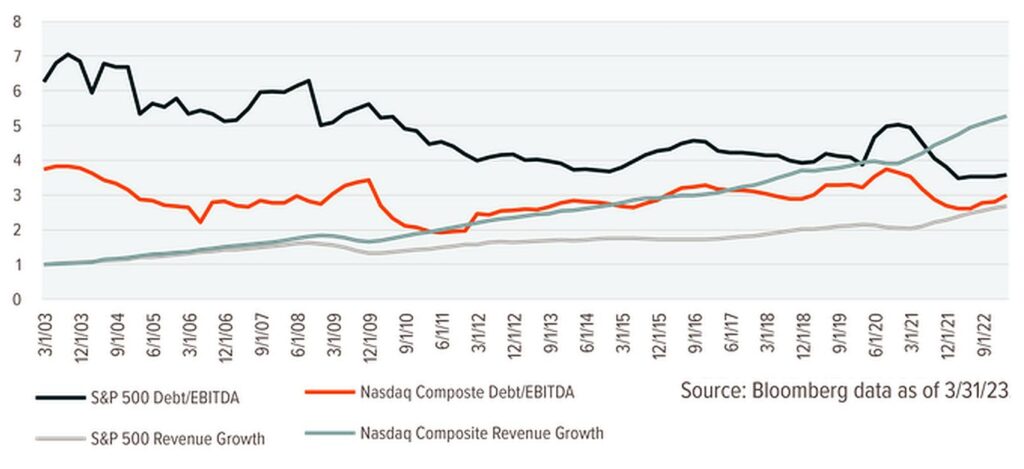

The Nasdaq Composite’s (NDAQ) outperformance versus the S&P 500 by more than 10% year-to-date underscores investor preference for growth that isn’t fueled by debt. Although Growth stocks are also not totally immune to the credit contraction, it looks like the credit recession winners would be easier to find among the Nasdaq constituents:

The main problem for stock-picking investors now is that the Growth sectors—IT, Healthcare, Communication Services, and some of the Consumer Discretionary stocks—have had a good run this year, with valuation multiples reaching high above their long-term averages. On the other hand, sustained growth in a low-growth environment may attract even more investors who are ready to buy at a premium, so the Growth rally may have more room to run.

Still, investors should be careful not to fall for overvalued stocks, as high valuations may limit their upside potential. Still, with the right tools, investors may find stocks of all types and sizes that tick all the boxes, like Axcelis Technologies (ACLS), Vertex Pharmaceuticals (VRTX), Applied Materials (AMAT), UnitedHealth (UNH), The Descartes Systems Group (DSGX), and many more profitable, fairly valued, low-debt companies, which can help a stock portfolio weather the credit crunch and the recession.