Get ready for long-term gains – that’s the message from Bank of America. In a recent note, the bank lays out just why it believes that the S&P 500 will hit 5,000 by next year. That would represent a gain of about 9.5% from current levels.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The bank’s chief equity technician, Stephen Suttmeier, sees the market in a secular bull phase – that is, a long-term upward trend lasting one or two decades. In his view, the secular trend started back in 2013 and is likely to hold until the latter years of this current decade. Backing his claim, Suttmeier explains how the multi-year chart of our current secular bull market closely matches charts of similar trends in the 1950s and 1980s.

But it’s not just an overall secular trend that Suttmeier believes is supporting the markets. He also explains how the current Presidential election cycle is working to give stocks a boost.

“The S&P 500 can continue its winning ways in the second half after achieving a solid first half. When the S&P 500 has an above-average first-half return during Presidential Cycle Year 3, the second half of the year tends to be stronger than the typical second half, with an average second-half return of 3.9%,” Suttmeier said and went on to add that 4th years of the Presidential term have also, in general, seen sound results.

All of this indicates that BofA sees stocks on the cusp of a further rally. The bank’s stock analysts are running with that theme and are pointing investors toward two names they believe are set to push higher from here – and by higher, we mean primed to more than double in value over the next year. Let’s take a closer look.

Reneo Pharmaceuticals (RPHM)

First up is Reneo Pharmaceuticals, a clinical-stage pharmaceutical company working on new treatments for rare genetic diseases. Reneo is focused on metabolic diseases, rare genetically-based disorders stemming from mitochondria, the energy production units of living cells. The company has two main research tracks, one on primary mitochondrial myopathies (PMM), and the other on long-chain fatty acid oxidation disorders (LC-FAOD).

These mitochondrial diseases are rare, difficult to treat at best, and currently have few or no effective treatment options. This makes them an open field for researchers like Reneo. The company has developed a new drug candidate, mavodelpar, which has potential to treat both PMM and LC-FAOD conditions, and the firm has initiated clinical trials on both tracks.

The leading track is the pivotal STRIDE study of mavodelpar in the treatment of adults with PMM. The company completed enrollment of the study during 1Q23, with 213 patients – surpassing the target enrollment of 200 patients. The company also has 100 patients enrolled in the STRIDE-AHEAD open label extension study, with more than 50 patients reaching the 6-month milestone in the clinical study. Topline results from this study are expected in 4Q23.

Also of note, Reneo received Fast Track designation from the FDA for mavodelpar, in the ‘genotype of long-chain fatty acid oxidation disorder (LC-FAOD).’ This is an important regulatory milestone in the development of new drugs for these rare diseases.

The promising prospects of mavodelpar caught the attention of Bank of America analyst Jason Zemansky, who finds the drug candidate’s impact on Reneo’s risk/reward profile to be highly favorable.

“In our view, lead asset mavodelpar’s upside has been overlooked by the Street ahead of its pivotal phase 2 readout—potentially leading to a first approval by YE24e/ early 2025e in Primary Mitochondrial Myopathy (PMM), with several additional indications poised to follow. Supported by positive commercial dynamics common in the rare/ orphan disease space (e.g., good pricing support, high unmet need, limited competition), we forecast an impressive launch trajectory with blockbuster potential – with a road to profitability as early as 2026e. Together with longer-term pipeline optionality, we see very attractive risk/reward for shares at current levels,” Zemansky opined.

To this end, Zemansky rates Reneo shares a Buy, and his $23 price target implies a robust 268% potential upside for the next 12 months. (To watch Zemansky’s track record, click here)

Overall, there are 4 recent analyst reviews on file for Reneo, and they are unanimously positive – giving the stock its Strong Buy consensus rating. The shares are priced at $6.23, with an average target price of $22.75 to suggest ~265% gain for the year ahead. (See RPHM stock forecast)

Bluebird Bio (BLUE)

The second BofA pick we’re looking at is Bluebird Bio, a clinical-stage biopharma taking its first steps toward commercialization. The company is working on new gene therapy treatments for rare genetic diseases – diseases that have chronic and highly negative impacts on the quality of life and have few or no effective treatments available. For gene therapy research firms, with their lead times measured in years and their high overheads, getting a drug to market is something of a ‘Holy Grail.’ Bluebird has achieved that and, in addition, has an active research pipeline.

Bluebird currently has three main tracks, featuring two recently approved drugs and one still undergoing clinical trials. The approved drugs are Skysona, a gene therapy treatment for early, active cerebral adrenoleukodystrophy (CALD), and Zynteglo, another gene therapy designed to treat the genetically based blood disorder beta-thalassemia. The third program is a drug candidate still in the clinic, lovotibeglogene autotemcel (also called lovo-cel), which is a new approach to gene therapy for the treatment of sickle cell disease.

On the commercialization side, Zynteglo and Skysona received their FDA approvals for use in August and September of last year. In Q1 of this year, Skysona had already begun to generate revenue, of $400,000, and the first commercial infusion of the drug was completed in March. The company has completed cell collection for 3 patients, and expects that 5 to 10 patients will start on the drug this year. Bluebird has also made 6 patients starts – that is, cell collections – for Zynteglo, and completed the first commercial infusion of that drug, with an expectation of a revenue stream from it in the 2Q23 report.

Turning to the clinical program, the lovo-cel track, the company submitted its Biologics License Application for the drug to the FDA in April of this year and on June 21 announced that the FDA had accepted the BLA for review with a PDUFA date of December 20, 2023. Lovo-cel is a ‘potentially transformative’ gene therapy for sickle cell disease (SCD); it is based on a one-time dose, for use in patients ages 12 and up, designed to treat the underlying cause of the condition by inserting a functional gene into the affected cells.

The high potential of lovo-cel forms the core of the BofA view on this stock, as set forth by analyst Jason Gerberry. He suggests two main factors pointing toward success for this stock: “1) Under-appreciated sickle cell disease (SCD) gene therapy product – we expect BLUE’s lovo-cel to gain timely approval on the December Food and Drug Administration (FDA) action date (Prescription drug User Fee Act-PDUFA). While BLUE has had some timeline-related setbacks along its path to lovo-cel approval, we believe that the drug’s data are equal to/more robust than data of its closest competitor, and we forecast peak sales approaching $1bn. 2) Lovo-cel approval and launch as catalyst – a recent biologics license application (BLA) acceptance mitigates further timeline risk, in our view. With lovo on market for SCD, we forecast BLUE reaching 2026E profitability, assuming one additional financing event. Based on peer (competitor) valuations, we believe that investors understand the SCD revenue opportunity, and thus we view the lovo-cel launch as a ‘prove it’ event, key to BLUE’s share price appreciation.”

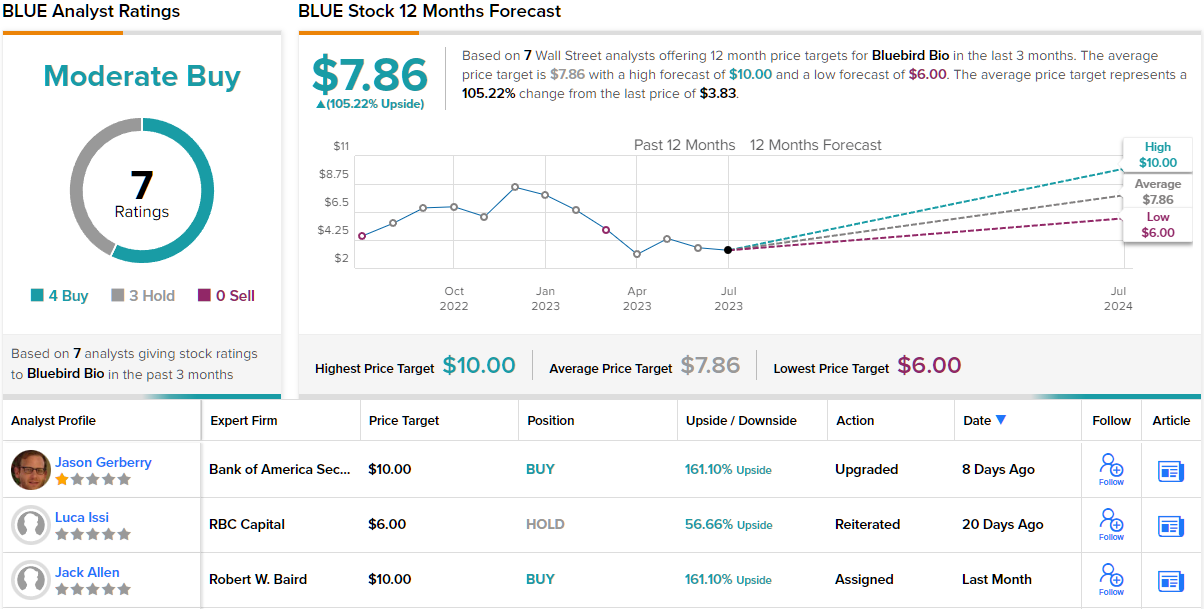

Based on lovo-cel’s potential strength, Gerberry rates BLUE shares a Buy, and his $10 price target shows his confidence in a one-year potential gain of 161%. (To watch Gerberry’s track record, click here)

Overall, the 7 recent analyst reviews on BLUE split 4 to 3, favoring Buys over Holds, for a Moderate Buy consensus rating. The stock has an average price target of $7.86, pointing toward 105% increase over the coming 12 months, from the current trading price of $3.83. (See BLUE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.