The S&P 500 has delivered the goods this year, having gained a very strong 23% throughout 2023. Meanwhile the tech heavy NASDAQ has outperformed the Street’s headline index by generating even stronger returns of 42%.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

But there’s a sector whose gains even puts that performance in the shade. The semiconductor sector’s main index, the SOX (the Philadelphia Semiconductor Index), is up by 62%, as investors have shown huge enthusiasm for semi stocks. That is not all that surprising, given AI has been the year’s main theme and semi firms are responsible for making the chips used in data centers powering the AI tech.

But following such remarkable gains, is it wise to keep on leaning into the sector as 2024 approaches?

Bank of America’s Vivek Arya, a 5-star analyst ranked right at the top echelons of Street experts, thinks the ride ahead might get a little bumpy, but there are just too many positive developments taking place that will keep pushing chips stocks forward.

“We see potential for higher volatility and intra-sector rotations following the strong run in semiconductors but note secular tailwinds for the industry remain in place,” Arya noted: “1) Continued adoption/investment in AI infrastructure, 2) Growing chip design complexity, 3) Automotive semiconductor content proliferation, and 4) Government focus on silicon independence (public investment).”

Of course, choosing the right stocks set to benefit the most from these tailwinds will be key, and here Arya singles out two of the year’s strongest performers as ones that will keep on delivering the goods – Nvidia (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD).

It’s not only Vivek who sees more good times ahead for the pair; according to the TipRanks database, both are rated as Strong Buys by the analyst consensus. Let’s find out why.

Nvidia

Talk of semi outperformance in 2023, and the first name that comes to mind is Nvidia. The stock is up by a huge 237% this year as the chip giant has delivered a series of beat-and-raise earnings reports that stunned Wall Street. The reason for the outsized success has been down to the role it has played in facilitating the all-conquering rise of AI. Nvidia has essentially cornered the market for the AI chips used in data centers to power the tech, its best-in-class offerings commanding more than an 80% share of the market.

Its success in the segment is not only down to the chips’ quality, but also because Nvidia provides the complex software needed to make them work. Not to mention, Nvidia has its fingers in many other pies – from gaming to automotive to crypto.

A quick look at some of the numbers offered in the most recent earnings report tells the story. In FQ3, the results once again exceeded expectations on all fronts. With record Data Center revenue of $14.51 billion (up by a huge 279% year-over-year), total revenue reached $18.12 billion, amounting to a 205.6% y/y increase, and outpacing consensus by $2.01 billion. Likewise, at the bottom-line, adj. EPS of $4.02 came in $0.63 above the analysts’ expectations. The company also delivered the goods on the outlook, expecting revenue in the fiscal fourth quarter to reach $20 billion, plus or minus 2%, way above the Street at $17.82 billion.

For Bank of America’s Arya, even factoring in 2023’s huge gains, Nvidia still represents the best chip stock out there, and amazingly, it still looks relatively cheap.

“NVDA remains our top pick,” says the 5-star analyst, “Despite 230% YTD move, NVDA is trading at a depressed 24x/20x CY24/25 PE implying many are skeptical in sustainability of genAI investments. We believe it’s early to predict a peak, as these trends take decades to play out… We expect NVDA to maintain its leading 75%+ market share position, followed by 10%-15% share combined across hyperscalers/OEMs investing in custom silicon projects… If NVDA can hold its 75%+ market share, we believe the company can generate >$40 in EPS by CY27E.”

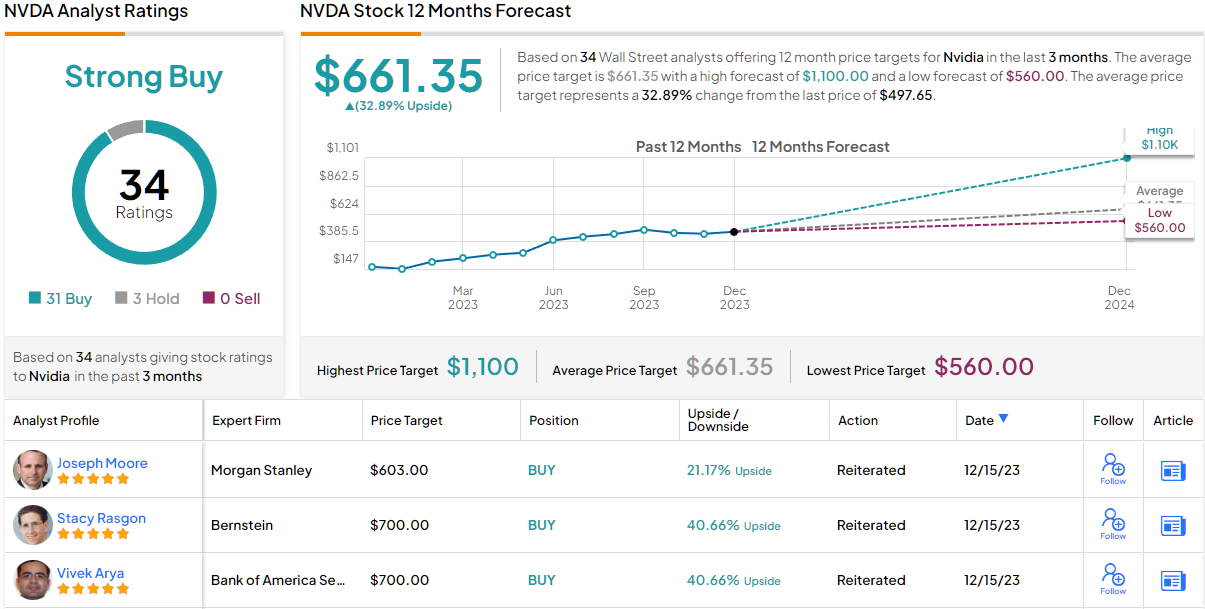

These comments form the basis for Arya’s Buy rating on NVDA while his price objective of $700 makes room for further gains of 41% in the year ahead. (To watch Arya’s track record, click here)

Amongst Arya’s colleagues, 30 other analysts join him in the bull camp, completely outmaneuvering the 3 Holds on file, and all naturally culminating in a Strong Buy consensus rating. Going by the $661.35 average target, a year from now, investors will be pocketing returns of 35%. (See Nvidia stock forecast)

AMD

It’s rather fitting that the next BofA pick we’ll look at is AMD. Because while Nvidia undoubtedly remains the AI stock, then AMD is seen by many as the name that could give it a run for its money in the space. That is down to the quality of its own offerings that could become a viable alternative to Nvidia’s AI-focused products, but it should also be remembered that AMD has had previous success in reining in a runaway segment leader. Intel used to be the undisputed CPU king, but AMD, under the leadership of CEO Lisa Su, rose from flirting dangerously with bankruptcy around a decade ago to take advantage of Intel’s missteps and continuously eat away at its dominance.

In 2023, AMD can also be seen as a mini-Nvidia. Its year-to-date gains might not be quite as high, but at 117%, that is a very respectable return. Meanwhile, its quarterly readouts have not been quite as jaw-dropping but have all provided beats on both the top-and bottom-lines.

The latest, for Q3, saw revenue reach $5.8 billion, representing a 4.1% YoY increase and beating the Street’s call by $110 million. Adj. EPS of $0.70 came in $0.02 above the analysts’ forecast.

Meanwhile, the company recently launched its latest lineup of AI chips, setting the scene to become a credible rival to Nvidia. With strong prospects in the field, and prior concerns abating, BofA’s Arya thinks it’s time for a reassessment of his AMD model.

The analyst recently upgraded his rating from Neutral to Buy and raised his price objective from $135 to $165, suggesting shares will appreciate by 18.5% over the coming months.

Explaining his stance, Arya said, “Our prior concerns of Embedded (FPGA) and Gaming (consoles) corrections have now generally materialized, with quickly increasing opportunities in data center GPUs/accelerators suggesting upside to medium-term sales outlook… We view AMD as well-positioned to gain incremental share of the hugely profitable $100bn+ accelerator market while continuing to make progress in server CPUs against incumbent INTC… Overall, we see AMD to continue delivering strong double-digit earnings growth through CY26E.”

Turning now to the rest of the Street, where AMD receives a Strong Buy consensus rating, based on an additional 25 Buys and 8 Holds. However, many seem to think the shares have soared enough for now; going by the $131.47 average target, the stock will see downside of 5.5% over the one-year timeframe. (See AMD stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.