According to strategists from J.P. Morgan, who have been tracking biotech fund flows to gauge interest levels, the volatility exhibited over the last few years has persisted in 2020, but for now, flows have taken off in a single direction.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Momentum in the biotech space has fueled the charge forward, with the fund flow winning streak now at 8 weeks. On top of this, as of May 21, the capital taken in by the IBB ETF quarter-to-date has already hit more than $2 billion, and the material gain for this period lands at $289 million.

It should come as no surprise, then, that investor focus has locked in on the biotech sector. However, given the industry’s volatile reputation, market watchers are turning to the best in the biotech stock picking business. Enter the Baker Brothers.

Brothers Julian and Felix Baker have earned guru-like status on Wall Street, with the track record to back it up. Baker Bros. Advisors, the hedge fund founded by the brothers in 2000 that focuses primarily on biotech companies, grew $250 million in managed assets in 2003 into $16.2 billion worth of assets as of May 15, 2020. Not to mention back in October 2019, the fund raked in a $1.4 billion gain in just two weeks after positive catalysts for two of its holdings, Seattle Genetics and BeiGene, sent shares skyrocketing.

Looking to the legendary brothers for inspiration, we scanned the fund’s recent 13F filing to see if its activity would point us in the right direction, and zeroed in on three biotech stocks in particular. Running the tickers through TipRanks’ database, we found out that each has received Buy ratings from analysts and sports some impressive upside potential.

BioDelivery Sciences (BDSI)

Subscribing to a patients-first philosophy, BioDelivery Sciences focuses on developing cutting-edge therapies for patients with serious and debilitating chronic conditions. Based on the strength of its Belbuca product, its drug designed to help manage severe pain, this biotech has scored several fans.

Among those singing BDSI’s praises are the Baker brothers. Acquiring a new stake in the company, Baker Bros. Advisors snapped up 1,638,334 shares valued at $8.07 million.

Representing Cantor, analyst Brandon Folkes also likes what he’s seeing. Following its Q1 2020 earnings release, he tells clients that the primary driver of his bullish thesis is Belbuca.

Looking at Belbuca’s performance in the most recent quarter, the drug generated net sales of $33.5 million, a 79% increase from the prior-year quarter. In addition, total Belbuca Rxs came in at 99,486, with NBRx at 7.3%. As for total Rxs, they were up 52%, and Folkes points out that the net revenue per Belbuca Rx exceeded his original forecast. BDSI also notched a 28% year-over-year gain in unique prescribers.

During the quarter, coverage for Belbuca grew after it added more than 2 million Medicare patients. It also expanded coverage in two regional commercial plans, representing 900,000 patients. Not to mention Folkes argued, “With a strong balance sheet we believe BDSI is well positioned to continue to drive growth in 2020 and beyond.”

The story for BDSI doesn’t end there. The company’s other product, Symproic, also delivered a solid quarterly performance, with it acquiring 1,170 new prescribers. Adding to the good news, total Rxs reached 16,137, up 19% from the prior-year quarter. It was able to achieve an 11.7% total RX share and 13.3% net Rx share.

Folkes concluded, “We have viewed BDSI as a Belbuca execution story, and the company continues to exceed its execution goals as well as our expectations time after time for Belbuca and now has started to do the same with Symproic. BDSI continues to execute on its commercial plan to drive continued growth of Belbuca, such that we believe investors will be rewarded by the company’s solid execution across both products in 2020 and beyond, which should drive upward earnings revisions and further upside in BDSI stock.”

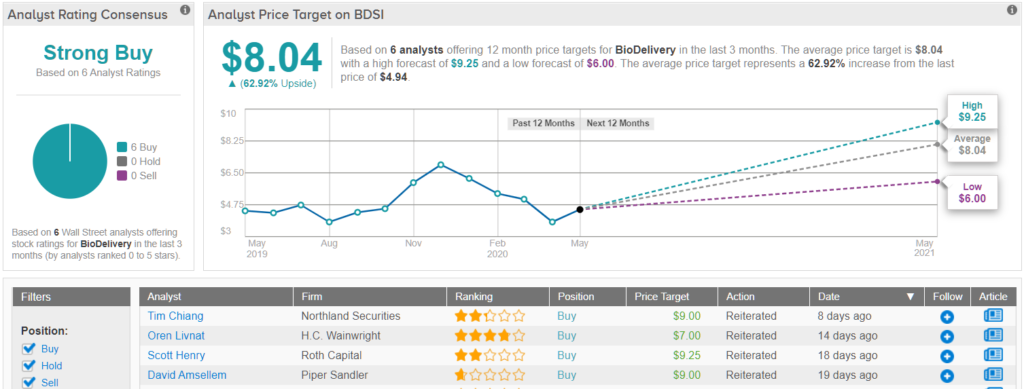

To this end, Folkes kept his Overweight call and $8 price target as is. Should this target be met, a twelve-month gain of 62% could be in store. (To watch Folkes’ track record, click here)

Turning now to the rest of the Street, other analysts are on the same page. Only Buy ratings have been received in the last three months, 6 to be exact, so the consensus rating is a Strong Buy. In addition, the $8.04 average price target puts the upside potential at 63%. (See BioDelivery stock analysis on TipRanks)

IVERIC Bio Inc. (ISEE)

Focused on the discovery and development of treatment options for retinal diseases, IVERIC hopes to address significant unmet medical needs. While some investors have expressed concern regarding a recent trial delay, ISEE is still attracting significant support.

Back in March, management announced that it was going to push back the initiation of the pivotal Phase 3 program for Zimura, its lead asset, in Geographic Atrophy (GA) based on the potential patient safety issues stemming from COVID-19. The trial will feature elderly participants who are required to visit physician offices for treatment, which is problematic as they might be more susceptible to the virus, lending itself to potential trial disruptions.

Baker Bros. Advisors has been sitting in the bull camp. Even more positive on the stock now, the fund boosted its ISEE holding by a whopping 1,054%, or 1.5 million shares. At over 1.6 million shares, the total position is valued at $6.93 million.

Meanwhile, Cowen analyst Ken Cacciatore remains unphased by the trial delay. “By pausing now for the pandemic to normalize, this should ensure a more seamless, continuous study. Encouragingly, in the interim, the company continues to bring clinical sites on board, which should allow for accelerated enrollment once the study is initiated. And, we believe, the recently received Fast Track designation from the FDA and the potential eligibility for expedited priority review could offset these delays,” he commented.

Digging a bit deeper into Zimura, it is an anti-C5 aptamer that inhibits terminal complement activation implicated in the pathogenesis of GA, an advanced form of dry AMD. In the original Phase 2/3 study in GA, the therapy was able to meet its primary endpoint, and was generally safe without causing any cases of inflammation and endophthalmitis.

Additionally, Cacciatore noted, “Based on these results – and given the size and design – the FDA indicated that the Phase II/III trial could serve as one of two pivotal studies, which we believe substantially de-risks the Zimura development. If the next Phase III results are positive, we believe IVERIC should be able to file the Zimura NDA in H2:2022 with a potential U.S. launch in H2:2023.”

As 1.5 million people in the U.S. suffer from GA, with it causing 20% of blindness, the fact that there aren’t any therapies available creates a significant market opportunity. This prompted Cacciatore to state, “The unmet need in GA is clear, given the lack of FDA-approved therapies for dry AMD, and we believe Zimura represents a potential $750 million opportunity.”

With respect to its gene therapy programs, ISEE plans to submit the IND for IC-100 in Q4:2020 and initiate the Phase 1/2 study in Rhodopsin-Mediated Autosomal Dominant Retinitis Pigmentosain H1:2021.

Based on all of the above, Cacciatore stayed with the bulls. Along with an Outperform rating, the $15 price target remains unchanged. This target conveys his confidence in ISEE’s ability to skyrocket 254% in the next twelve months. (To watch Cacciatore’s track record, click here)

Looking at the consensus breakdown, it has been relatively quiet when it comes to other analyst activity. Only one other review has been published recently, but it was also bullish, so the consensus rating is a Moderate Buy. Given the $14 average price target, the upside potential lands at 230%. (See IVERIC stock analysis on TipRanks)

Minerva Neurosciences (NERV)

With its innovative therapies, Minerva Neurosciences’ goal is to dramatically improve the lives of patients battling central nervous system (CNS) diseases. Ahead of an upcoming unblinding of data for its lead candidate, roluperidone (MIN-101), the biotech has found itself on the Street’s radar.

The Baker Brothers recently decided to pull the trigger on this stock. Adding a NERV position to the fund, Baker Bros. Advisors bought up 688,531 shares. The hedge fund’s new stake boasts a value of $4,145,000.

Writing for BTIG, five-star analyst Thomas Shrader has high hopes for NERV as it gears up for the release of Phase 3 data evaluating roluperidone as a treatment of the negative symptoms (the loss of functions) associated with schizophrenia. He points out that the trial is modeled closely after the successful Phase 2b study, which was well-sized and held up to significant data reanalysis, with it also being deemed acceptable as an initial trial for approval if confirmed in the Phase 3 trial.

“Overall, we see roluperidone as having a unique place in the schizophrenia treatment landscape less prone to generics that overwhelmingly treat positive symptoms of the disease (things like hallucinations). A second drug in Phase 2 studies for insomnia provides modest downside protection in case of Phase 3 disappointment, but the roluperidone unblinding is the reason to own the stock,” Shrader commented.

Speaking to the available market, Shrader believes the commercial opportunity is “huge” as schizophrenia affects almost 1% of Americans and drugs in the space are both widely used as well as expensive, with the cost coming in at around $50 per day if patent protected. He added, “The lead drug roluperidone has shown the ability to treat the negative symptoms of schizophrenia making it essentially unique in the treatment landscape.”

While some have interpreted the Phase 2b results to mean that the placebo adjusted treatment effect was modest, Shrader calls this conclusion “premature”. To support this claim, he argues efficacy in the Phase 2a trial was close to producing results that make independent living more likely, efficacy was still building at nine months and the Phase 3 trial extension runs a full year and the treatment effect from baseline, not placebo, might be a more accurate metric.

If that wasn’t enough, its MIN-202 (seltorexant) therapy is another strong component of the development pipeline, with it achieving a rapid onset of action and a short half-life designed to work quickly but reduce the “hangover effects” that come with sleep aids. In addition, Phase 2b data showed superior and more sustained efficacy compared to Ambien. Going forward, Shrader sees the candidate as having the potential to be a major upside driver.

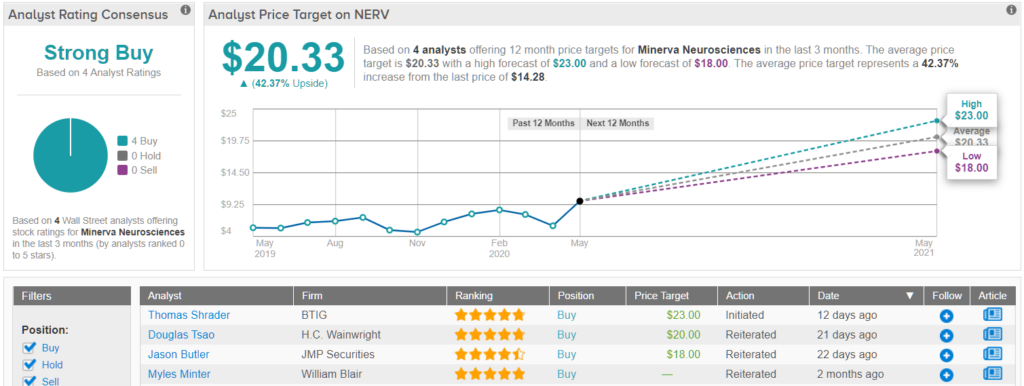

All of this prompted Shrader to join the bulls. To kick off his coverage, he published a Buy rating and set a $23 price target. A 61% twelve-month gain could materialize if the target is reached. (To watch Shrader’s track record, click here)

What does the rest of the Street think about NERV? It turns out that other analysts have also been impressed. 4 Buy ratings and no Holds or Sells have been assigned in the last three months, making the consensus rating a Strong Buy. The $20.33 average price target indicates 42% upside potential. (See the Minerva stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.