American States Water (NYSE:AWR) and California Water Service Group (NYSE:CWT) are two Dividend Kings featuring the lengthiest dividend-growth track records. The title “Dividend King” is a term used among investors to classify companies that have increased their dividends annually for 50 or more years. For American States Water and California Water, these figures stand at 68 years and 55 years, respectively.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Thus, both water utility companies classify to be members of this elite of group stocks. In fact, American States Water’s dividend-growth track record is the most prolonged one in the globe. No other public company has consistently increased its payouts annually since 1955.

In this article, I am going to explain how AWR and CWT have managed to sustain such admirable dividend- (and hence earnings) growth track records and which of the two might be the better Dividend King to pick right now.

Decades of Invariable Growth

As signaled by their legendary dividend track records, both AWR and CWT feature decades of invariable growth. While their growth has slowed down in recent years as both companies have reached peak maturity stake, their profits have still been treading higher.

This can be attributed to a growing customer base, operational efficiencies, and strategic management of operating costs. They’ve also benefited from approved rate increases (approved by regulators), demonstrating their ability to navigate regulatory environments effectively.

Specifically, AWR’s and CWT’s net incomes have grown at compound annual growth rates (CAGRs) of 3.8% and 7.0%, respectively, effectively allowing them to sustain their dividend growth, as they have been doing for decades now. To understand why both companies are likely to keep growing their earnings and dividends for more decades ahead, it is essential to grasp the fundamental qualities that have consistently enabled their success up until now.

Recession-Proof Cash Flows

The pillar of AWR’s and CWT’s enduring success in maintaining exceptional growth track records lies in their remarkable ability to consistently deliver stable results, irrespective of the prevailing economic conditions.

Both companies have established themselves as recession-resistant entities due to water consumption’s fundamental importance for survival. Moreover, water exhibits a high degree of inelasticity, meaning that its demand remains largely unaffected despite higher pricing over time.

Regardless of the global circumstances, water consumption levels exhibit minimal fluctuations in response to external factors. As a result, water utility companies can enjoy an exceptionally predictable stream of revenues. The stability of AWR and CWT is further reinforced by their status as legal monopolies within their operating regions, a common characteristic in this industry.

Regulated Rate Increases Provide Growth

The second catalyst that has contributed to AWR’s and CWT’s continuous growth is rate case filing, a process utilized by utilities to present proposals for rate hikes, citing reasons such as increased operating costs or infrastructure upgrades. These rate hikes consistently outperform inflation, resulting in significant top-line growth.

For example, AWR’s adopted average water rate base grew at a CAGR of 11.3% from 2018 to 2022. For CWT, its base grew at a CAGR of 15.5% from 2016 to 2022, from where it is expected to grow at a CAGR of 19% through 2025.

Consequently, both American States Water and California Water Service Group possess a remarkable level of revenue-growth visibility. This visibility empowers them to responsibly increase their dividends in alignment with their net income growth projections.

Which is the Better Dividend Stock?

In my opinion, both AWR and CWT offer exceptionally secure dividends. Their payout ratios, which stand at approximately 72% and 56%, respectively, based on last year’s earnings, provide strong reassurance that their dividends are not at risk. What’s more, both companies have consistently grown their payouts for over half a century, underscoring their commitment to dividend growth.

The better question is which stock offers better dividend prospects. From a growth point of view, AWR and CWT have grown their dividends at 10-year CAGRs of 9.2% and 4.7%, respectively. Interestingly, AWR’s growth rate is much more significant than that of CWT, despite the latter’s EPS growth being superior, as previously discussed. This is why AWR’s payout ratio has climbed much higher than that of CWT lately.

Because of this, I believe that CWT enjoys better dividend-growth prospects from here. Not only will AWR have to slow down its current pace of dividend growth if its management doesn’t wish the payout ratio to reach more alarming levels, but CWT is also likely to enjoy improving base rate hikes in the coming years, as previously mentioned. Finally, CWT’s yield of 2.0% is marginally slightly higher than AWR’s, further adding to its edge.

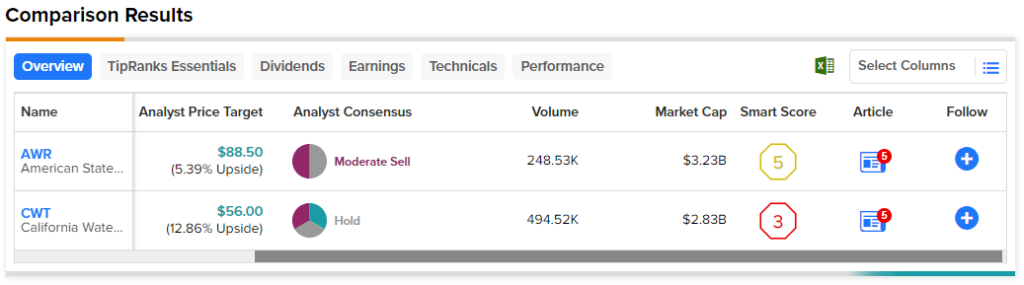

What are the Price Targets for AWR and CWT Shares?

Turning to Wall Street, AWR stock has a Moderate Sell rating based on one Hold and one Sell rating assigned in the past three months. The average AWR stock price prediction of $88.50 implies 5.2% upside potential.

Moving to CWT, the stock features a Hold rating based on one Buy, one Hold, and one Sell rating assigned in the past three months. The average CWT stock forecast of $56.00 implies 13% upside potential.

The Takeaway

Overall, I believe that both ART and CWT feature exceptional earnings and dividend-growth track records, which should endure moving forward despite their overly-mature operations. That said, I believe that CWT may offer stronger dividend-growth potential due to its more comfortable payout ratio and strong rate base visibility through 2025.

Finally, CWT’s forward P/E multiple of 22 appears much more attractive than AWR’s forward P/E of 31, which also explains the Moderate Sell rating the latter has attracted from Wall Street.