In this piece, I evaluated two semiconductor/chip stocks, Broadcom (NASDAQ:AVGO) and ON Semiconductor (NASDAQ:ON), using TipRanks’ comparison tool to determine which is better. A deeper analysis suggests a bullish view might be appropriate for both, albeit with one presenting much greater risk.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Broadcom designs, develops, manufactures, and supplies a wide range of semiconductor and infrastructure software products for the data center, wireless, storage, networking, broadband, and software markets. ON Semiconductor targets the cloud, Internet of Things, automotive, industrial, and medical markets with its intelligent power and image-sensing technologies.

Shares of Broadcom are up 55% year-to-date and 85% over the last 12 months. However, ON Semiconductor stock is up only 6% year-to-date and over the past year after plunging by almost 22% on Monday due to weak fourth-quarter guidance.

With such a dramatic difference in stock-price performance after Monday’s sell-off in ON, it’s no surprise that ON is trading at a steep discount to Broadcom. Later on, we’ll compare their price-to-earnings (P/E) ratios to gauge their valuations against each other and that of their industry.

For comparison, the U.S. semiconductor industry is trading at a P/E of 43.6 versus its three-year average of 29.4.

Broadcom (NASDAQ:AVGO)

At a P/E of 25.9, Broadcom is trading at a steep discount to its industry’s current valuation — and even a small discount to the industry’s three-year average P/E. Thus, despite its robust year-to-date rally, a bullish view looks appropriate for Broadcom, especially considering its long-term stock price appreciation.

Over the last three years, shares of Broadcom are up 160%, while they’ve gained more than 300% over the past five years, indicating long-term price appreciation. Thus, although the stock is off 8% over the last three months, it looks like a name that’s worth buying and holding for the long term.

In fact, Broadcom is one of the relatively few tech companies that pays dividends, making it even more attractive as a long-term buy-and-hold position. The chipmaker pays a solid dividend yield of 2.19%, which is quite attractive for a technology stock, given that the sector’s average dividend yield is only about 1%. Additionally, the chipmaker has boosted its dividend annually for the last 13 years, a strong track record.

Broadcom is also exceptionally profitable with a soaring net income margin, which has climbed from 12.4% in 2020 to 24.5% in 2021, 34.6% in 2022, and 39.3% over the last 12 months.

Finally, Broadom’s pending acquisition of VMware (NYSE:VMW) has been delayed, but it said recently that it expects the deal to close “soon” and before the expiration of the merger agreement. In the original press release announcing the deal, Broadcom said the acquisition would add about $8.5 billion of pro-forma EBITDA within three years of the closing, supporting the benefits of the combination.

What is the Price Target for AVGO Stock?

Broadcom has a Strong Buy consensus rating based on 16 Buys, two Holds, and zero Sell ratings assigned over the last three months. At $984.94, the average Broadcom stock price target implies upside potential of 17.08%.

ON Semiconductor (NASDAQ:ON)

After its post-earnings 21.7% plunge, ON Semiconductor is now trading at a P/E of about 12.6, placing it at a steep discount to its industry and to Broadcom. After that sell-off, the stock is now in oversold territory, suggesting a bullish view might be appropriate, although investors should monitor the company closely due to the high level of risk.

First, the company’s Relative Strength Index of 20.3 means it is now in oversold territory, given that anything below 30 is considered oversold.

Also, the company did beat estimates, coming in at $1.39 per share in adjusted earnings on $2.18 billion in revenue versus the estimates of $1.34 per share on $2.15 billion in revenue. However, the market dumped ON Semiconductor shares rapidly due to the company’s weaker-than-expected guidance.

ON expects its revenue to decline to between $1.95 billion and $2.05 billion for the fourth quarter, but analysts had been expecting $2.18 billion. The company also guided for adjusted earnings of $1.13 to $1.27 per share for Q4 versus the consensus of $1.36 per share. Likely after that guidance, the consensus of analysts tracked by TipRanks fell to $1.24 per share.

While the Street’s reaction to the weak guidance seems a bit overdone, it is somewhat understandable, given the company’s history of falling revenue. While ON Semiconductor grew its revenue 28% year-over-year in 2021 and 23.5% year-over-year in 2022, its revenue tumbled 6% year-over-year in 2019 and 4.8% in 2020.

Management blamed a single “outlier” automaker customer for the lowered forecast, suggesting it could be just a temporary setback, especially considering the company’s long-term stock-price appreciation. Even after Monday’s sell-off, ON Semiconductor stock’s three-year and five-year returns are similar to Broadcom’s, at 168% and 268%, respectively.

Thus, ON Semiconductor may also be a decent buy-and-hold position over the long term after Monday’s sell-off, although the weaker guidance suggests a higher level of risk with ON.

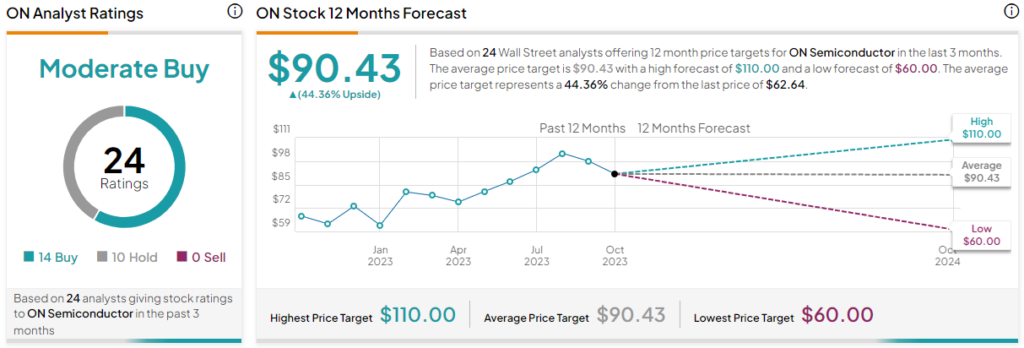

What is the Price Target for ON Stock?

ON Semiconductor has a Moderate Buy consensus rating based on 11 Buys, 10 Holds, and zero Sell ratings assigned over the last three months. At $100.06, the average ON Semiconductor stock price target implies upside potential of 44.4%.

Conclusion: Bullish on AVGO and ON

Although both semiconductor stocks receive bullish ratings, a key difference between them is in the amount of risk. Both look like solid long-term buy-and-hold stocks due to their great longer-term returns. In fact, Broadcom’s three-month pullback of about 8% does present a decent entry point for long-term investors.

However, ON’s weak guidance is a cause for concern. If things don’t turn around, that stock could go horribly wrong, but in the event of a recovery, this week’s sell-off will end up being a major buying opportunity.