Organized labor strikes are nothing new, they’ve been a part of industry for well over a century now. But the recent move by the UAW, to strike against Detroit’s Big 3 automakers, has taken a new twist – the union is hitting all three at once, after the breakdown of contract negotiations.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Specifically, the UAW has initiated strike actions at final assembly plants for Ford, GM, and Stellantis. Labor leaders are flexing their muscles this time, looking to gain back past concessions and to push for higher wage increases in the face of inflation. With a Friday deadline looming, there are concerns that the UAW may expand the strike to engine and transmission plants, as well as final assembly.

However this turns out for the Big 3 and their dealership networks, Oppenheimer’s 5-star analyst Brian Nagel says that the labor dispute offers investors some clear opportunities, writing, “While the wage-related battle between UAW and leading, domestic auto manufacturers remains fluid and could drag on for some time, we tend to view any disruptions within new vehicle production processes as generally positive for used car and auto parts retail.”

Getting into more granular detail, Nagel adds, “Near term, labor-related strife at domestic auto OEMs is likely to further impact new vehicle production and hence pricing for autos. Longer term, higher cost infrastructures for auto OEMs could elevate further vehicle prices, thereby bolstering demand for more attractively-priced pre-owned cars and encouraging consumers to keep and maintain vehicles longer.”

Taking this as a starting point, we’ve used the TipRanks platform to pull up the details on two stocks, both Buy-rated and ones that stand to potentially gain as the UAW strike rumbles along. Here they are, presented along with comments from some of the Street’s top analysts.

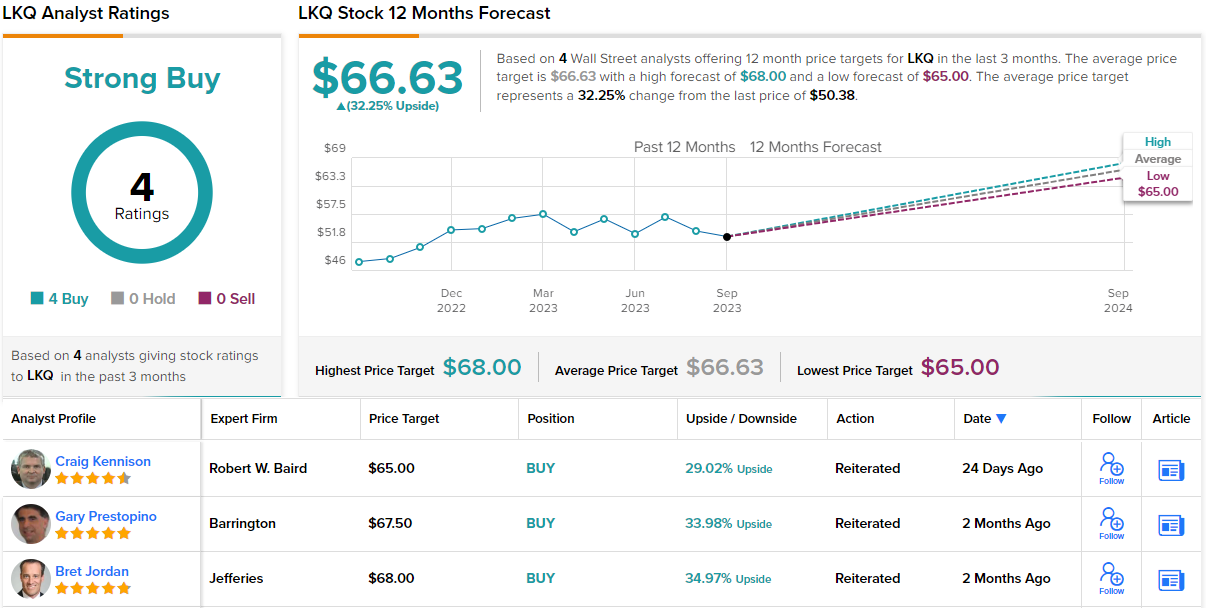

LKQ Corporation (LKQ)

First up on our list is LKQ, a leader in the market for salvaged and recycled auto parts. The company was founded in 1998, on a simple idea that has taken root: car owners and mechanics want lower-cost alternatives to manufacturer-authorized parts when it comes to repairing and accessorizing their vehicles. LKQ stepped into that niche, providing alternative and specialty parts, with an eye on quality and high-value.

The company has developed an international footprint, and has operations in 25 countries in North America, Europe, and Asia. LKQ can boast 1,600 locations and some 45,000 employees, and its after-market parts have racked up more than 170 million cumulative road miles every year. The company’s largest geographical segments are in North America and Europe, while its largest operating segment is the Specialty business, offering high-end after-market parts and accessories in the US and Canadian markets.

Even before the UAW strike, LKQ’s results were impressive. The company posted $3.4 billion in revenue for 2Q23, the last quarter reported, a total that was up 3.3% year-over-year and in-line with analyst expectations. At the bottom line, the $1.09 adjusted diluted EPS came in 1 cent over the forecast.

In a metric of particular note to dividend investors, LKQ reported strong y/y gains in its cash flow figures. The company brought in $480 million in operating cash flow and $414 million in free cash flow for 2Q23, compared to $328 million and $288 million in the second quarter of last year. The solid cash flow backed up the firm’s dividend payment, which was declared on July 27 and paid on August 31 at 27.5 cents per common share. That payment annualizes to $1.10 per common share and the 2.2% yield is in-line with peer companies.

Watching LKQ for Stiffel, 5-star analyst Michael Hoffman takes note of the company’s cash generation, but is more cognizant of the potential for LKQ to expand its business should the carmakers face a prolonged labor strike. Hoffman writes, “Our investment thesis for LKQ focuses on its breadth of recurring low growth organic sales growth that translates into mid-single or better FCF sustainable CAGR. The LKQ superior fulfillment and market position in the North American and UK and European aftermarket auto parts and services market supports this outlook. The OE parts disruption seen during the pandemic benefited LKQ. By association that would suggest the UAW strike is a benefit. The current rolling, limited UAW strike is not likely to have an impact. However, if the scope widens or the strike persists for a long time then LKQ is likely to see demand for aftermarket parts that would have been fulfilled with OE parts (cars inside warranty periods typically use OE parts).”

Looking ahead, the analyst gives the stock a Buy rating with a $66 price target to suggest a one-year upside of 31%. (To watch Hoffman’s track record, click here.)

All 4 of the most recent analyst reviews here are positive, making LKQ’s Strong Buy consensus rating unanimous. The stock is selling for $50.38, and its $66.63 average price target is just a touch above Hoffman’s target and implies a 32% increase for the next 12 months. (See LKQ’s stock forecast.)

AutoZone, Inc. (AZO)

The second stock we’ll look at is AutoZone, a well-known name – especially for do-it-yourself car buffs. AutoZone is a retailer, and a leader in the niche for aftermarket car parts, accessories, and all the small needs for conducting vehicle maintenance in your own driveway; customers can find everything from brakes and rotors to batteries, and fuel line cleaners to engine coolants.

The company has built its business by becoming a one-stop for everyone’s automotive needs, and since being established in 1979, has grown to have a presence in all 50 states plus DC and Puerto Rico, as well as in Mexico and Brazil.

In its most recent financial results, released earlier this week for fiscal 4Q23, AutoZone showed an interesting split in its sales growth. Domestic (that is, US) sales posted a modest 1.7% y/y gain in the quarter, while international sales jumped 34%. That fueled a company total of $5.7 billion in revenue, up 6.4% y/y and $80 million ahead of the estimates, with same-store sales increasing 4.5% in a favorable comparison to the 2.5% expectation.

At the bottom line, AutoZone reported a diluted EPS, by GAAP measures, of $46.46, compared to $40.51 in the previous year’s Q4. This result was $1.57 higher than had been anticipated.

Solid results, pointing toward more growth to come, caught the attention of JPM analyst Christopher Horvers. The 5-star analyst is optimistic about AutoZone going forward, and says of it, “We continue to believe that AZO is positioned for comp acceleration and a modest re-rating off what we view as trough levels (16x FY1). As such, we continue to recommend buying, as trends should improve over the coming year on improved execution, ongoing supply chain and IT initiatives, and the potential for more favorable winter weather in early 2024. Margins remain under control with potential upside in 1Q, with AZO’s capital allocation philosophy adding ~10 pts to EPS growth in FY24.”

Quantifying hist stance, Horvers puts an Overweight (Buy) rating here, with a price target of $2,975 to imply a 12-month share price increase of 15%. (To watch Horvers’ track record, click here.)

There are 11 recent analyst reviews on AZO shares, with a breakdown of 8 Buys to 3 Holds supporting the Moderate Buy consensus rating. Shares are currently trading at $2,583.36 and carrying an average price target of $2,844.78, a combination that suggests the stock will gain 10% on the one-year horizon. (See AutoZone’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.