A 10x oversubscribed Arm Holdings (NASDAQ:ARM) held its IPO on Thursday at an initial price of $51, but quickly shot higher. By the time the first trade was placed on the Nasdaq, Arm shares were already fetching $56.10 apiece. And by the time trading wrapped up for the day, Arm Holdings shares cost $63.59. That made for a ~25% one-day gain for investors lucky enough to get in at the IPO price.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But Needham analyst Charles Shi is not impressed.

In a note launching coverage of Arm Holdings, Shi commented that Arm stock looks fully valued at its current share price. The analyst declined to name a price target for Arm, and rates the stock only “hold” going forward.

Why is that?

“Arm’s architecture is a foundation of smartphones,” admitted Shi, “but we believe the world is entering a post-smartphone era that will see high-performance computing and [Internet of Things or IoT] lead the next phase of semiconductor growth.” While Arm may try to pivot to emphasize these sectors, it would face multiple competitors offering “viable alternatives” to its products — a situation that Shi analogizes to Intel’s efforts to replicate its dominant position in PC semiconductors elsewhere.

Indeed, as Shi points out, Arm already has tried to expand beyond smartphones into IoT. But five years of pouring money into research and development, and of tripling of output of processors tailored to IoT applications, has resulted in the following: IoT chips account for 70% to 80% of Arm’s chip volume, but contribute only about 10% of Arm’s total royalty revenues. Clearly, the market doesn’t value Arm’s IoT chips nearly as much as it does Arm’s smartphone chips.

Turning to high performance computing (think artificial intelligence), designing more chips for use in the data centers that power AI means Arm will be trying to horn in on a business already dominated by “Nvidia on the GPU side” and “Intel and AMD on the CPU side.” Flush with IPO cash today, Arm may be able to make a dent here, but it’s going up against some pretty stiff competition from three of the biggest names in semiconductors. Success cannot be guaranteed.

Meanwhile, back at the core smartphones business, while Arm can certainly “grow by capturing greater value” within its core market of smartphones, the very fact of its current dominance means there’s not a lot of upside left there — especially given how much the stock has already run up on Day 1.

All of which results in Shi presenting some pretty muted — and sobering — projections for Arm. Based on $0.64 in actual per share profits in fiscal 2023, and expected growth to $0.96 per share in fiscal 2024, and $1.22 per share in fiscal 2025, Shi sees Arm growing earnings 50% this year, but only 27% next year.

That’s still great growth. The problem is that it’s probably not great enough growth to justify Arm’s current valuation of nearly 100 times trailing earnings — or for that matter, even the 52x 2025 forward earnings assumed by Shi’s estimates. (To watch Shi’s track record, click here)

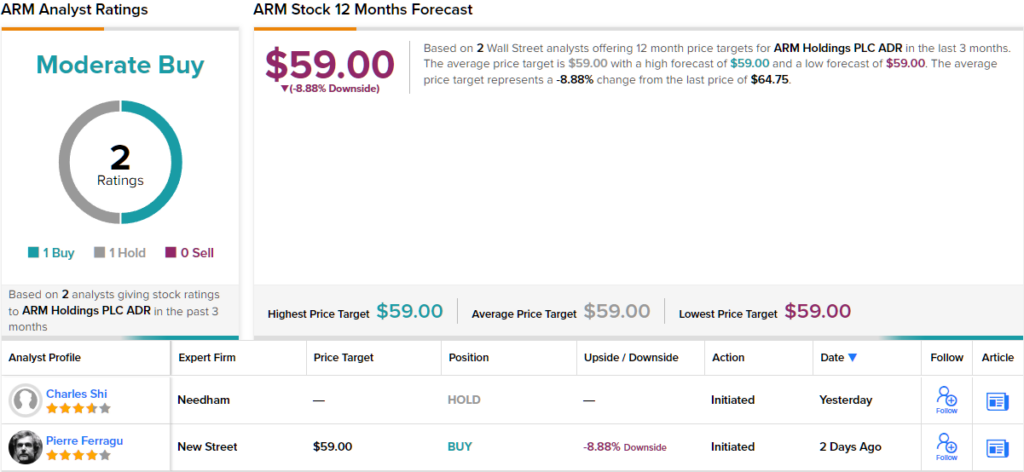

Overall, in its short time on the public markets, ARM has garnered 1 Buy rating and 1 Hold, making the analyst consensus rating a Moderate Buy. (See ARM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.