Just because this past year has been difficult, doesn’t mean that we can’t approach the New Year with a degree of hope. Inflation has shown some signs of moderation, and if that holds, we can look forward to some consequent easing in the pace of the Fed’s interest rate hikes – and that will reduce the risk of recession. And in that case, next year’s stock environment could take a turn for the better.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

A better stock environment in 2023 will set investors up for portfolio gains – and more so if they’re willing to shoulder the risk that walks along with reward. And if investors want to get into risk/reward calculations, that will lead them into the penny stocks. These low-cost equities bring the advantage of a low cost of entry plus the potential for unseemly gains.

Still, these stocks are controversial. The high reward potential comes with a high-risk potential, you just can’t have one without the other. As a result, investors either love the pennies or they hate them. But for anyone willing to take the chance, we’ve used the TipRanks Penny Stock Screener to find two of these high-potential equities that offer Strong Buy analyst consensus ratings to go along with their huge upside potential. Here are their details, along with comments from the Street’s analysts.

OcuPhire Pharma (OCUP)

First up is OcuPhire Pharma, a clinical-stage biopharmaceutical firm specializing in the development of new medications for ophthalmic conditions – that is, diseases and conditions of the eyes. OcuPhire’s pipeline features Nyxol, a 0.75% phentolamine ophthalmic solution for the treatment of pharmacologically induced mydriasis (RM). The company is at the cusp of commercializing this new drug – it has submitted the New Drug Application this month and expects to receive approval in 2H23 with a commercial launch to follow.

This is a major milestone for the company, as getting a new drug onto the market is the ‘holy grail’ for clinical biotechs. Nyxol, an eyedrop whose other indications include the treatment of conditions such as presbyopia and night vision disturbances (NVD), is well-positioned to fill that role. OcuPhire, in November of this year, entered into a global license agreement with FamyGen Life Sciences for the commercialization of Nyxol, across all indications. The agreement includes a $35 million upfront payment and double-digit royalties.

While this company has a solid commercialization candidate in Nyxol, it has not put all its eggs in that basket. OcuPhire is also developing APX3330, a new drug candidate for the treatment of diabetic-induced eye conditions like retinopathy and macular edema. The company plans to release data from the ZETA-1 Phase 2b trial early next year.

While OcuPhire is pre-revenue, the company has a sound cash foundation, with $13.9 million on hand as of the end of 3Q22. According to management, this is enough to fund operations into 4Q23.

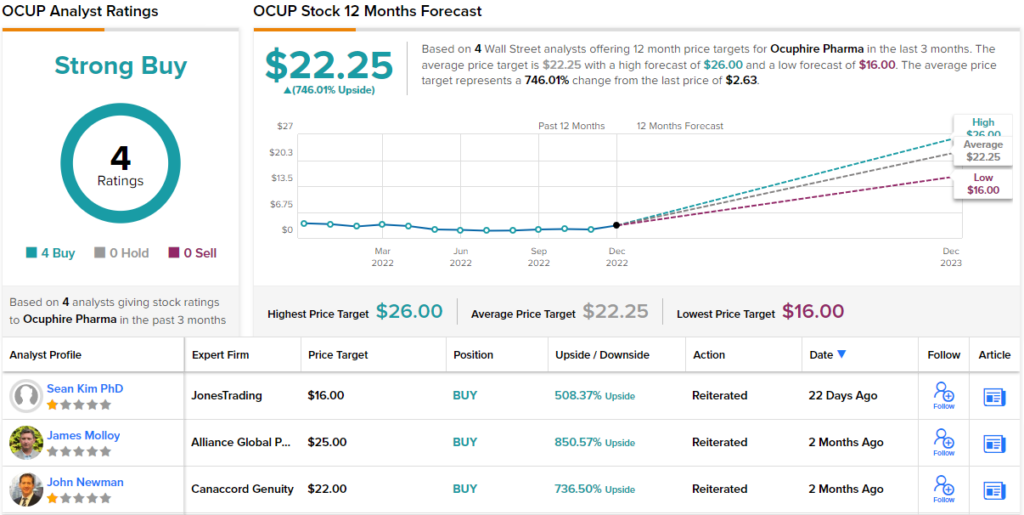

In coverage of this stock for Jones Research, analyst Sean Kim is impressed by the NDA on Nyxol – as well as the drug’s additional indications still at the clinical stages. These multiple paths give OcuPhire a flexibility that will boost its chances of success. Kim writes, “We are encouraged by the company’s continued execution of its development plans for Nyxol and look to additional program updates for the other two indications, specifically, presbyopia and night vision disturbances (NVD) as we ease into 2023. We also await the company’s highly anticipated ZETA-1 Phase 2 top-line results for APX3330 in diabetic retinopathy expected to report in early 2023. We believe APX3330 in diabetic retinopathy remains underappreciated and presents favorable risk/reward heading into its ZETA-1 readout given its large addressable market and the stock’s current valuation.”

With these catalysts in mind, Kim rates OCUP as a Buy, and sets a $16 price target that implies a powerful 508% upside potential for the coming year. (To watch Kim’s track record, click here.)

Kim’s take is bullish, but he’s far from the only upbeat analyst here. The stock has 4 recent analyst reviews on file, and they all agree that it’s a Buy, making the Strong Buy consensus unanimous. The shares are selling for $2.63 and have an average price target of $22.25, suggesting that a huge one-year gain of 746% lies ahead for the stock. (See OcuPhire’s stock forecast at TipRanks.)

Special end-of-year offer: Access TipRanks Premium tools for an all-time low price!Click to learn more.

Rigel Pharmaceuticals, Inc. (RIGL)

Next up is Rigel Pharmaceuticals, a drug company currently operating at the development, clinical, and commercial stages of the pipeline. The company has several drug candidates in pre-clinical stages, and several undergoing clinical trials. In addition, Rigel has two FDA-approved drugs on the market, available to patients.

The common factor in Rigel’s stable of products is a focus on hematologic disorders, cancers, and rare immune diseases. The company works on the discovery and development of novel small molecule drugs with potential to improve the lives of patients.

Of special interest to investors are Rigel’s two approved products. These are Tavalisse, for the treatment of adult chronic immune thrombocytopenia, and Rezlidhia, a treatment for r/r acute myeloid leukemia. Having two marketable assets gives Rigel a steady income stream (see below) – but the big news here is the approval, earlier this month, of Rezlidhia for use in the US. The company announced last week that the drug is now available by prescription on the US market.

In the last reported quarter, Rigel showed a top line of $22.4 million, of which $19.2 million came from sales of Tavalisse. Year-over-year, Tavalisse sales were up 20%. The company is complementing its Tavalisse sales with a commercial launch of Rezlidhia, which will partly use the existing marketing teams. The Rezlidhia commercial program will be undertaken in partnership with Forma Therapeutics.

H.C. Wainwright analyst Joseph Pantginis sees the Rezlidhia launch as the main story here, and goes on to outline his bullish outlook for the drug.

“An estimated 20,000 cases of AML are diagnosed annually in U.S., and about 6-9% of these cases are mIDH1+ r/r AML cases appropriate for Rezlidhia intervention,” Pantginis explained. “With strong efficacy and safety data in tandem with an extensive commercialization plan, we believe that Rezlidhia should be a key value driver for the company going forward and Rigel is well-positioned to have a formidable heme/onc therapeutic portfolio with two commercialized products in going into 2023.”

“As domestic commercialization begins, the company continues to pursue regulatory approvals and/or potential partners in other global markets. For these reasons, along with a successful commercial launch under its belt, our opinion is Rigel is on track to rapidly execute on this plan,” the analyst went on to add.

The analyst’s numbers tell the rest of the story. Pantginis rates these shares as a Buy, and his $15 price target indicates his confidence in a frankly amazing upside of 1110% on the one-year time frame. (To watch Pantginis’ track record, click here.)

There are 4 recent analyst reviews here, with a 3 to 1 breakdown favoring Buy over Hold for a Strong Buy consensus rating. The stock’s sale price of $1.24 and average price target of $5.25 combine to give an upside potential of 323% for the next 12 months. (See Rigel’s stock forecast at TipRanks.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.