We’re winding up the first half of 2023, and what could be more natural than to figure out the best stocks for the rest of the year? Stock picking of this sort is an essential skill for every investor, and fortunately, the Street’s analysts make it easy. They are always ready to point out which stocks are their ‘Top Picks,’ and we can follow those recommendations.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

In this case, we’re looking at three stocks that have ‘top pick’ designation from the analysts, and also feature an attractive combination of a low initial cost and a solid double-digit upside potential for the next 12 months.

So, let’s give them a closer look. Using the TipRanks database, we’ve pulled up the details on these three names. Together with the analyst commentaries, well find out just what makes them Top Picks for the rest of 2023.

Janus International Group (JBI)

Some essential products are so ordinary, so everyday, that we just overlook them – without realizing just how important they are. Janus, an industry leader in commercial and industrial doors, holds that sort of niche. The company offers a wide range of rolling and swinging doorways and entryway products for commercial-grade use, with a particular specialty in rolling steel doors, smart entry systems, and hallway systems designed for and marketed toward commercial self-storage facilities. The company also works with the more general community of commercial and light industrial enterprise customers.

We’re in the digital age, so it should come as no surprise that Janus has developed a digital doorkeeping product, Noke. This is a smart lock and smart entry system, able to connect to smartphone and tablet devices through Bluetooth. The system is optimized for self-storage facilities, allowing customers easier access to their store rooms, and site ownership and management greater ability to monitor and manage the facility.

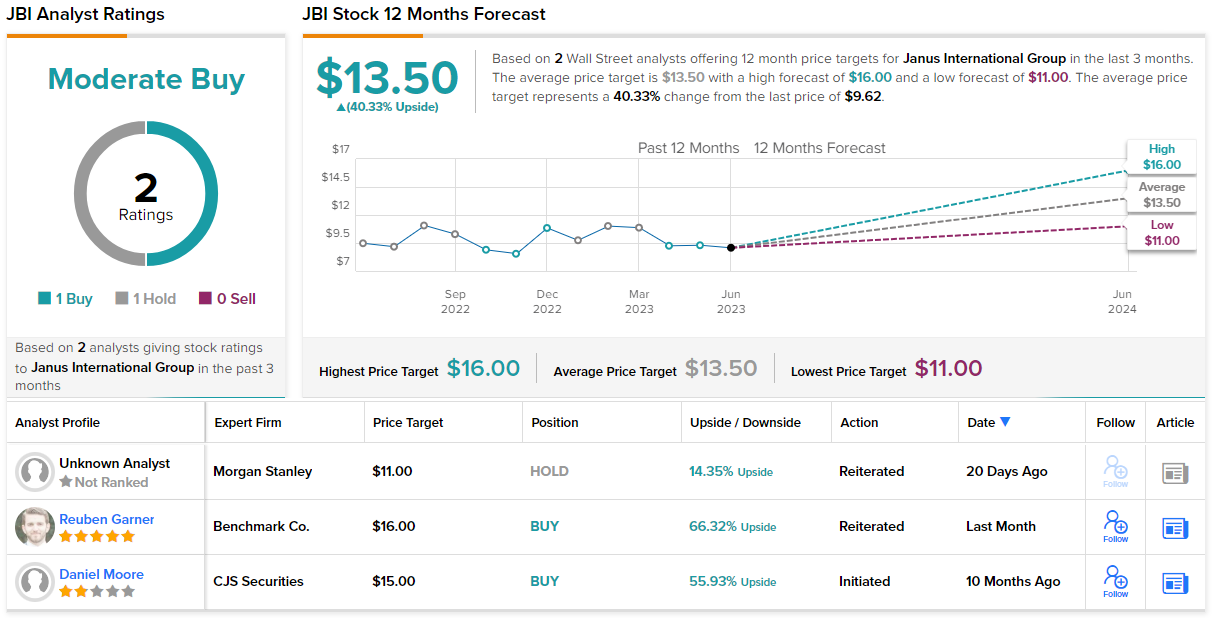

For one indicator of just how necessary something so simple as a door can be, we can look at Janus’ revenue results. The company has a solid record of year-over-year top line growth in recent quarters, and the last reported results, from 1Q23, were no exception. Janus’ revenue total, of $251.9 million, came in $9.25 million better than had been forecast – and was up 9.75% year-over-year. At the bottom line, Janus recorded adj. EPS of 18 cents, beating the forecast by a penny, and jumping 5 cents per share from the prior year’s Q1 result.

Looking ahead, Janus guided toward 2023 full-year revenue in the range of $1.06 billion to $1.08 billion, up from the previous range of $1.05 billion to $1.07 billion. At the midpoint, the new revenue guidance represents a 5% increase when compared to 2022 and meets Street expectations.

The company’s sound results and optimistic outlook, combined with its industry-leading position, caught the eye of Benchmark’s 5-star analyst Reuben Garner, who wrote, “With a strong quarter under its belt and solid backlog, management raised guidance for FY23 topline and EBITDA (roughly by the 1Q beat), and the company remains nicely on track for its mid-term targets issued last quarter… While we aren’t sure when the discount/disconnect will close between Janus’ fundamentals (and performance) and the stock’s valuation, we are increasingly confident that it ultimately should and will. With other names in our group making a run of late and Janus’ multiple discount to its peer group increasing to nearly 50%, we are moving JBI to our Top Pick.”

Going forward from this stance, Garner rates JBI shares as a Buy, and his $16 price target indicates room for 66% share growth on the one-year time horizon. (To watch Garner’s track record, click here)

On the Street, it’s rather quiet on the JBI front. Only one other has recently chimed in with a review. Adding their Hold into the mix, Janus gets a Moderate Buy consensus rating. Shares are priced at $9.62, and the $13.50 average price target implies a one-year upside potential of 40%. (See JBI stock forecast)

Genius Sports (GENI)

For as long as people have competed at sports, there has been sports betting. Gamblers will bet on the results of games, fans will bet on their favorite teams, casual gamers will place a bet for a thrill. Genius Sports, a tech firm working in data management and integrity, provides software services for sports betting and media companies, offering improved quality for the sports data needed by leagues, teams, and fans. Genius partners with over 650 sports organizations, and covers some 240,000 sports events.

The firm was founded back in 2001, in London, and has since grown to become a globe-spanning operation. Genius Sports counts more than 1,800 people on its staff, and boasts offices in New York, LA, Medellin, Sofia, and Vilnius. The company’s technology is used in more than 150 countries, and major leagues – including the NFL, NASCAR, and the NCAA – depend on Genius for accurate data.

While Genius has carved out a solid niche for itself, in an industry that drips cash, the company’s results in the 1Q23 period were mixed. The total revenue figure was solid; Genius brought in $97.23 million at the top line, up more than 13% y/y and nearly $5 million ahead of the expectations. At the bottom line, however, the company’s earnings came in just under the estimates. The reported EPS was negative, a 12-cent loss per share, and 1-cent worse than had been anticipated.

These mixed results were more than balanced by the company’s outlook going forward. Genius is guiding toward Q2 revenue of $80 million vs. consensus at $78.05 million, and for Q3, the $99 million revenue guidance was also above the $97.44 million expected on Wall Street.

All of this is background to JMP analyst Jordan Bender’s notes on Genius Sports. He sees the company holding an advantageous position in the sports betting arena, and getting a boost from its access to data rights. Bender says of Genius, “We are now recommending shares of GENI as our top pick in our coverage universe. The online sports betting ecosystem is vast, and companies are fighting for their piece of the pie. The company operates in the most attractive part of a complex ecosystem by owning long-term data rights necessary for any betting operator to price bets, while only competing against one major company globally. Management has checked nearly all the boxes including 1) hitting quarterly estimates, 2) removing the SPAC warrants, 3) investing in its technology to insulate itself from potential competition, and 4) positioning itself for a FCF inflection.”

All of this adds up to an Outperform (Buy) rating, in Bender’s eyes, and his $8 price target points toward share growth of 41% over the next year. (To watch Bender’s track record, click here)

There’s a general optimism on Wall Street about this stock, evidenced by the 6 unanimously positive analyst reviews which give GENI shares their Strong Buy consensus rating. The stock is selling for $5.66, and at $7, the average share price suggests a 24% one-year gain. (See GENI stock forecast)

Alight, Inc. (ALIT)

We’ll wrap up with software company Alight, a firm that offers business process software products on the popular subscription model – call it BPaaS. The company’s products are designed to bring cloud-based solutions to business processes, analytics, and human capital. The company makes use of AI to improve process automation and risk management, while predicting customer needs and capabilities.

Alight provides these critical services to enterprise customers in the healthcare, wealth management, and payroll industries, at any scale needed. The company’s flagship platform, Worklife, has been shown to provide a solid ROI, through actionable insights and desirable outcomes. Alight itself has benefited from a combination of diversified customers, long-tenured blue-chip clients, and a recurring revenue model that supports both strong cash flows and future growth. At the end of last year, Alight could depend on a revenue stream composed 84% of annual recurring revenue, and a solid 98% average revenue retention rate.

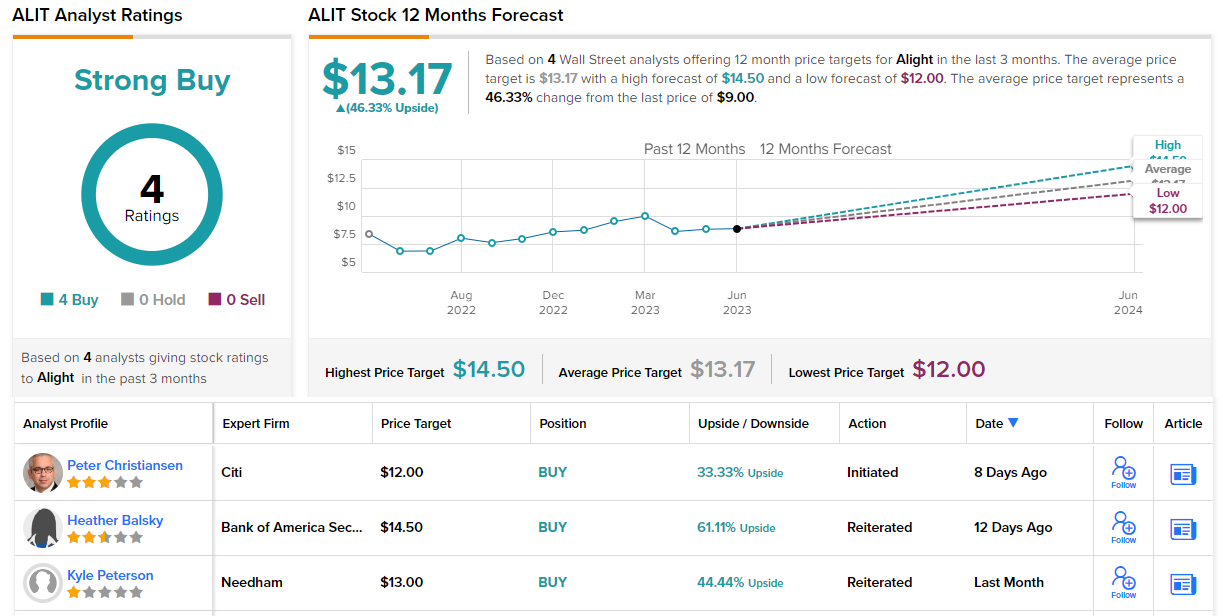

In its recent 1Q23 results, Alight showed nearly 15% y/y top line revenue growth, with the $831 million reported beating the estimates by $27.35 million. The company’s bottom line, an adj. EPS of $0.13, was 1-cent better than the forecast and 1-cent better than the year-ago result. The company’s BPaaS revenue grew 50% y/y, and cumulative BPaaS bookings passed $1.5 billion.

The strong BPaaS performance was the first metric noted by Needham analyst Kyle Peterson, who does not hesitate to paint an upbeat picture of the stock’s prospects: “As BPaaS deals continue to become a larger piece of the business (BPaaS revenue is expected to grow 15%+ MT(midterm)), ALIT expects total revenue growth of 6-8%, EBITDA margin expansion of 400–500 bps and operating cash flow conversion of 60-80% over the MT. We view the MT financial framework as attractive and attainable given the numerous revenue growth levers, ongoing cost optimization efforts, and the sizable TAM which we believe provides ample room for LT growth.”

“With the shares trading at an EV/EBITDA of ~9x our FY24 estimate, we view the risk-reward as favorable. ALIT remains our Top Pick for 2023,” Peterson went on to say.

In-line with this stance, Peterson gives the stock a Buy rating, with a $13 price target that indicates room for 44% share appreciation in the year ahead. (To watch Peterson’s track record, click here)

This is another stock with a unanimous Strong Buy consensus rating – this one based on 4 positive analyst reviews. The shares are currently trading for $9.00, and the $13.17 average price target suggests a 46% increase from that level in the next 12 months. (See ALIT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.