We’re about to wrap up 2022, and it’s time to take stock of the stock market. Earlier this month, we got some good news on inflation – the November data showed the rate of price increases slowing to 7.1% annualized, from 7.7% in the prior month. That was followed by the Federal Reserve’s seventh interest rate hike of the year, an increase of 50-basis points that marked a slowdown from the previous run of four 75 bp hikes.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But comments from Fed Chair Jerome Powell have made it clear that, while the central bank may slow down its rate hikes to match a slowing inflation, it will keep up the policy of higher interest and tighter money until inflation is beaten – and that we should expect rates to rise above 5% and stay there through 2023.

That has investors growing increasingly worried about the risk of recession. But just because the markets are volatile doesn’t mean that strong opportunities can’t be found. Wall Street’s analysts are out there, combing the stock world, to find the right equities to buy.

Using TipRanks database, we identified two stocks that hold ‘Strong Buy’ consensus ratings from the Street’s analysts, and boast triple-digit upside potential for the coming year. Let’s find out just why these stocks may double or more in the year to come.

scPharmaceuticals, Inc. (SCPH)

scPharmaceuticals, the first stock we’re looking at, has developed a new drug, Furoscix (a furosemide injection), which has the potential to permanently change the treatment of chronic heart failure – by replacing IV infusion drugs with self-administered subcutaneous diuretic injections. Furoscix is the first – and so far, the only – drug candidate to reach FDA approval in this niche.

That approval was announced this past October. The FDA granted approval to Furoscix for marketing, and scPharmaceuticals has a commercial launch planned for 1Q23. That’s the company’s biggest news, and the main catalyst ahead.

Commercialization requires capital, and scPharmaceuticals has taken two steps in recent months to ensure it has plenty on hand. First, in October, the company announce a debt financing agreement with Oaktree Capital Management, worth up to $100 million. The company has used part of that funding to clear away outstanding debt, and the remaining funds are earmarked for support of the upcoming Furoscix commercialization activities.

In addition to this agreement, scPharmaceuticals announced in November a public offering of stock. The offering saw 6.62 million shares go on the market, at $5.25 each. The company realized approximately $50 million in gross proceeds, to add to its cash on hand.

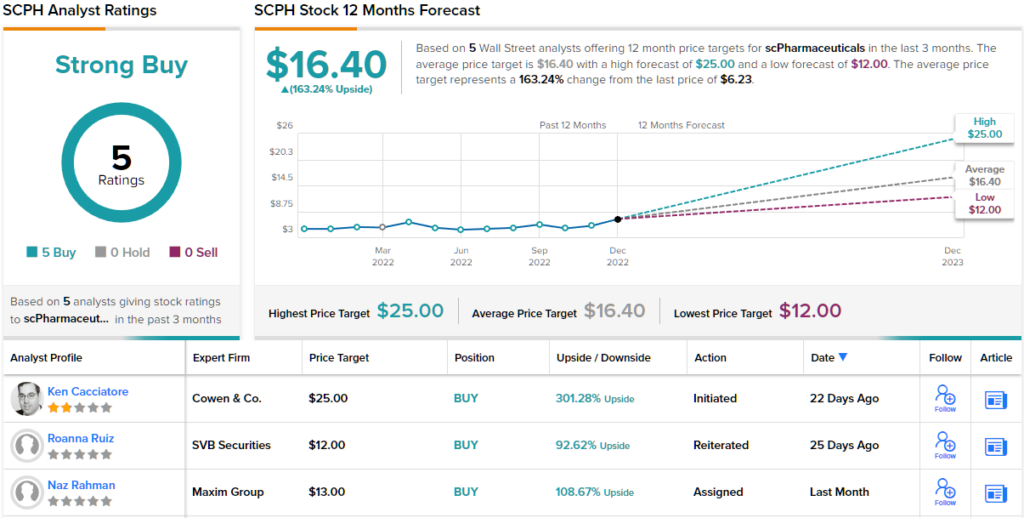

Covering this stock for Cowen, analyst Ken Cacciatore sees plenty of potential for investors to grab onto. He writes, “We believe Furoscix’s value proposition should ensure early and broad payor coverage despite entering a genericized market. Specifically, the average cost of a heart failure hospitalization could be close ~$20,000, and given the average treatment cost of Furoscix of ~$3,000 (assuming average 4 doses x $825/dose), Furoscix could offer ~ $17,000+ in saving per patient. In addition, given the concentrated prescriber base, we believe scPharma can address this opportunity with a thoughtful commercial strategy and a relatively lean salesforce.”

“Given the clear value proposition and the unmet need in this large market, we believe the shares are significantly undervalued,” the analyst summed up.

The analyst quantifies his bullish stance with an Outperform rating and a $25 price target that implies an impressive 302% upside for the next 12 months. (To watch Cacciatore’s track record, click here)

Overall, there are 5 recent analyst reviews on this budding commercial biopharma, and they all agree that this is one to buy, for a unanimous Strong Buy analyst consensus rating. The average price target of $16.40 indicates potential for a high 163% upside from the current trading price of $6.23. (See SCPH stock forecast on TipRanks)

New Amsterdam Pharma Company (NAMS)

Now let’s turn to New Amsterdam Pharma, a clinical stage biotech company working on a novel drug candidate to improve the treatment of metabolic diseases. The drug candidate, obicetrapib, works to lower LDL-C levels (the ‘bad cholesterol’) by blocking the cholesterol esterase transfer protein (CETP) that would otherwise move the ‘good’ HDL-C into LDL-Cs. Obicetrapib, if successful, would be a safe and convenient treatment option, available as an orally dosed, once-daily, low-dose therapy.

The company has multiple late-stage clinical trials ongoing, including the Phase 3 BROOKLYN study, which is looking at obicetrapib as a treatment for patients with heterozygous familial hypercholesterolemia whose condition is not responsive to current lipid-modifying therapies. This study saw the first patient dosed in July of this year.

BROOKLYN is hardly the only study New Amsterdam has at this time. The company is evaluating obicetrapib in two other Phase 3 trials, the BROADWAY and PREVAIL trials, both of which are evaluating the drug candidate in patient groups suffering from atherosclerotic cardiovascular disease. Furthermore, the Phase 2b ROSE trial is looking at obicetrapib as an adjunct to high-intensity statin therapies.

These trials give New Amsterdam a line-up of upcoming catalysts in the next year, but they won’t come cheap. The company raised necessary capital through a business combination, or a SPAC transaction, which was completed this past November. The combo, with Frazier Lifesciences Acquisition Corporation, brought New Amsterdam gross proceeds of $328 million.

Initiating coverage of New Amsterdam for Jefferies, analyst Dennis Ding points out the ‘steady cadence of late stage readouts over the next few years,’ and goes on to add, “NAMS has a novel LDL lowering pill for hyperlipidemia and is already inmultiple Phase III trials reading out over the next several years. We think the program is relatively derisked with strong PCSK9-like LDL lowering efficacy and has strong non-LDL biomarker improvements too and could be $3-4B+ in peak sales to NAMS, which is upside to current valuation.”

An opportunity of that magnitude has Ding rating NAMS shares as a Buy, while his price target of $24 implies that a one-year gain of 112% lies ahead for the company. (To watch Ding’s track record, click here)

Overall, this newly public biopharma has picked up 3 analyst reviews since the ticker started trading – and all are positive, making the Strong Buy consensus unanimous. The stock is selling for $11.30 and its $21.50 average price target suggests a robust 90% upside by the end of next year. (See NAMS stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.