Over the past two years, inflation has dominated headlines as prices have been rising at their fastest pace since the late 1970s. In June of last year, the inflation rate peaked at a 40-year high of 9.1%. However, the latest data from this past June revealed a somewhat encouraging annualized rate of just 3%. Markets rose on the news, reflecting a sense of relief and optimism that the worst is over.

With this boost to overall economic sentiment, investors now have a favorable backdrop to explore new stock picks that can provide additional income in 2023 and beyond. One of the most effective ways to achieve this is through high-yield dividend stocks, particularly those with strong potential for share growth.

With this in mind, we used the TipRanks’ database to zero in on two stocks that, according to Wall Street analysts, could generate a combination of considerable capital gains and dividend income – making them a potential double-fisted payday for investors.

Ternium SA (TX)

We’ll start south of the border, where Ternium is Latin America’s largest flat steel producer and one of the largest steel firms in the Western Hemisphere. The company has production facilities in Mexico, Argentina, Brazil, and Colombia, as well as in Central America and the southern US. The largest consumers of Ternium’s products are Mexico, followed by Argentina and the US.

The company’s products include a range of steel in many different types. Ternium produces hot-rolled and cold-rolled steel, steel tubes, shaped steel, galvanized sheeting, tinplate, and a variety of prefab items specifically for the construction industry. In addition to steel production, Ternium is active in iron ore mining in Mexico and in the production of coke and slag. Last year, the company reported net sales revenue of $16.4 billion.

In April of this year, Ternium reported its 1Q23 results, and a look back at the first quarter will show how the company stands. Total steel shipments came to 3.065 million tons, up 4% year-over-year, while iron ore shipments fell 11% y/y to 799,000 tons. The company’s quarterly net sales of $3.6 billion showed a 16% y/y drop, and missed the forecast by over $25 million. At the bottom line, however, the results showed a stronger positive bent; the $1.91 non-GAAP EPS was 92 cents per share better than had been anticipated.

The company finished the quarter with a sound cash position, reporting $612.3 million in net cash from operations. Capital expenditures came to $197.9 million, and the free cash flow afterwards was $414.4 million. Ternium reported a cash position of $3 billion exiting Q1, up 15% from the prior quarter.

Turning to the dividend, we find that Ternium takes an unusual approach, paying out twice per year. The last payments, sent out in November in May, were $1.80 and $0.90 per ADS, respectively. These payments annualize to $2.70 per ADS, and yield a solid 6.5%.

Ternium stock has gained an impressing 50% this year, outperforming the broader market by far. Yet, according to Morgan Stanley’s 5-star analyst Carlos De Alba, the stock is in a position to continue showing gains.

“TX shares are undervalued and offer an attractive risk-reward. We believe TX profitability has reached an inflection point and in the past this has proven a good entry point for the stock. The company has a strong balance sheet with a net cash position, even considering ongoing growth investments, and we expect it to pay an attractive dividend that is underestimated by the market… A future possible listing in a Latam equity market may generate passive investor demand for the stock, further elevating its trading multiple,” De Alba opined.

To this end, the top analyst rates Ternium shares an Overweight (i.e. Buy), while his $51 price target implies a one-year upside potential of ~17%. Based on the current dividend yield and the expected price appreciation, the stock has ~23% potential total return profile. (To watch De Alba’s track record, click here)

Overall, this old-school industrial stalwart has picked up 4 recent analyst reviews, including 3 Buys and 1 Hold, for a Strong Buy consensus rating. (See TX stock forecast)

New York Community Bancorp (NYCB)

For the second stock on our list, we’ll shift from the steel industry to financial services. New York Community Bancorp is a major name in the US banking sector. The New York-based bank holding company is the parent company of the New York Community Bank; in fourth quarter of last year it acquired Flagstar Bank, and in March of this year, in the wake of the bank failure crisis, the Flagstar subsidiary acquired certain of Signature Bank’s assets.

NYCB now operates some 435 branches, and boasts total assets worth $123.8 billion. In addition, the holding company has $83.3 billion in loans outstanding, and $84.8 billion in deposits. The bank’s subsidiaries offer a full range of banking services for both retail and commercial customers, as well as business and real estate services. The company operates a regional headquarters in Troy, Michigan, and is listed among the 100 largest US banks.

This bank holding company did well in the first quarter of the year, as shown by its quarterly financial release. 1Q23 was NYCB’s first full quarter of operation after the Flagstar acquisition, and so its results came in for extra scrutiny.

At the top line, the company showed revenues of $2.65 billion. This was up from $346 million at the end of 1Q22, increasing by more than 7x in just one year. The bottom line figure, an EPS of $2.87 by GAAP measures, was up from 31 cents in the year-ago period and was $2.63 ahead of the forecast. The non-GAAP EPS was 23 cents per share, and was 2 cents better than expectations.

NYCB successfully integrated Flagstar into its operations, and acquired an important wealth management business, among other things, from the failed Signature Bank. The Q1 report showed that NYCB came out of this past spring’s financial crisis in a stronger position than it was in prior.

On the dividend, this company has kept up a quarterly common share payment of 17 cents since 2016, and made its most recent payment in May of this year. The 17-cent dividend annualizes to 68 cents per common share and gives a strong yield of 5.8%.

Watching this stock for Raymond James is analyst Steve Moss, who believes that the Signature asset acquisition puts the bank in a solid position to support growth going forward.

“We expect NYCB’s second quarter results will be marked by core deposit growth and NIM expansion, which should differentiate the bank from its peers, improve confidence in the EPS trajectory. We also expect NYCB will report a stronger balance sheet due to capital generation and lower wholesale funding, post the March 2023 acquisition of SBNY from the FDIC. If NYCB is able to sustain these trends, and retain most of SBNY’s teams, we believe the stock’s valuation should re-rate meaningfully higher over time,” Moss opined.

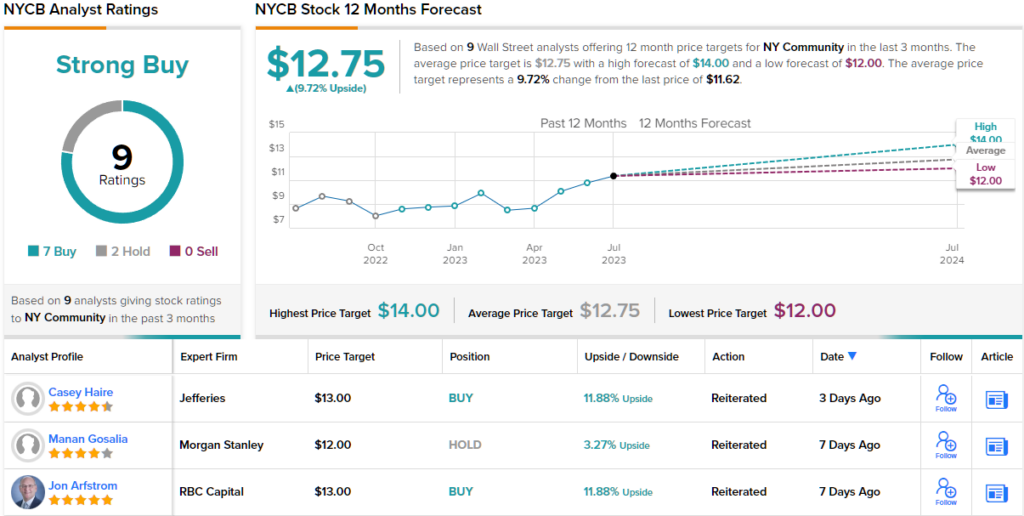

This stance induced Moss to put a Strong Buy rating on NYCB shares, and his $14 price target indicates a potential for 20.5% share appreciation in the coming year. (To watch Moss’s track record, click here)

Overall, of the 9 recent analyst reviews on NYCB, 7 are to Buy compared to 2 to Hold, giving the stock a Strong Buy consensus rating. (See NYCB stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.