It doesn’t take much for sentiment to shift abruptly on Wall Street. Markets could be up one moment, then all of a sudden crash on account of a negative development.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

And looking at its current state, it won’t take much for it to come tumbling down, says Morgan Stanley’s chief investment officer and chief US equity strategist, Mike Wilson.

“The S&P 500 risk/reward today is one of the worst I’ve ever seen, given the earnings setup that we see in front of us combined with the valuation that we have today,” Wilson noted.

“The equity market is not trading well under the surface,” he goes on to add, citing businesses with troubled balance sheets, good news already reflected in high valuations, real estate sector challenges, the potential for regional bank troubles to flare up again, amongst other bubbling issues with anyone tipping over into a crisis potentially leading to a meltdown. The result? The S&P 500 could see a drop of more than 25% from current levels.

So, what’s an investor to do to safeguard against such a scenario? Lean into the classic defensive play, dividend stocks, and preferably ones with high yields.

We’ve gotten this process started and have pulled out of the TipRanks database two such names certain Wall Street analysts are pointing investors toward right now – and one of these even boasts a yield of 13%. Let’s see why these could be the right choices to offer protection in the event of a sharp shock to the markets.

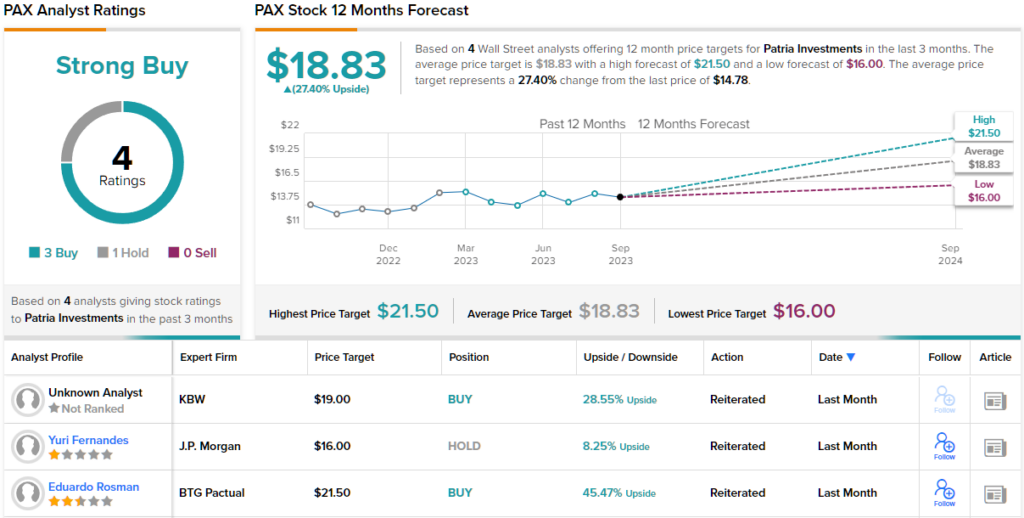

Patria Investments (PAX)

Patria is one of the leading investment firms in Latin America, and can boast of a global footprint with offices in 10 cities on 4 continents. The company has 30 years’ experience, and as of June 30 this year had more than $28 billion in total assets under management, an increase of 7% compared to the same time in 2022.

Patria’s portfolio isn’t just large, it’s also well-diversified. The company has investments in private equity, in credit and capital financing, in real estate, and in strategic infrastructure projects in energy, transportation, and data. Patria’s overall investment strategy has always focused on generating attractive returns for its own investors.

In the company’s last financial release, for 2Q23, Patria showed good headline results, along with a dividend declaration that should get return-minded investors to take notice. At the top line, Patria’s revenue was solid, coming in at $78.6 million. This figure was up an impressive 41% year-over-year, and beat the forecast by over $14 million. At the bottom line the EPS of 30 cents per share, missed the estimates by 1 cent – although it was up 50% from the prior-year figure.

Turning to the dividend declaration, we find that the company set a 25.1-cent payment per common share, that went out on September 8. This payment is fully covered by the firm’s earnings, and the annualized rate of just over $1 gives a solid yield of ~7%.

Latin America is sometimes overlooked in the world’s economic market, but it has potential to be a true powerhouse. With a population of 665 million, and several dynamic capital markets, it’s no surprise that the region has produced leading investment firms such as Patria. This is the background to BTG Pactual analyst Eduardo Rosman’s bullish view.

“We consider Patria a premium asset manager in LatAm, reflecting its strong brand power and unique funding (in hard currency with long-term commitments). Moreover, Patria could be one of the key platforms consolidating the LatAm asset management market. We believe the valuation is attractive… With the Brazilian and Chilean capital market recovering and the liquidly of the stock improving, we think the stock in one to watch closely in 2H23. We are Buyers at current levels,” Rosman wrote.

Along with a Buy rating, Rosman sets a $21.50 price target for the next 12 months, suggesting a gain of 48% could be in the cards. (To watch Rosman’s track record, click here)

Overall, this stock has 4 recent reviews from Wall Street’s analysts, with a 3 to 1 breakdown favoring Buys over Holds – for a Strong Buy consensus rating. The $14.78 current trading price and the $18.83 average price target combine to imply a 27% increase for the year ahead. With the annualized dividend added in, that’s a potential one-year return of 34%. (See Patria stock forecast)

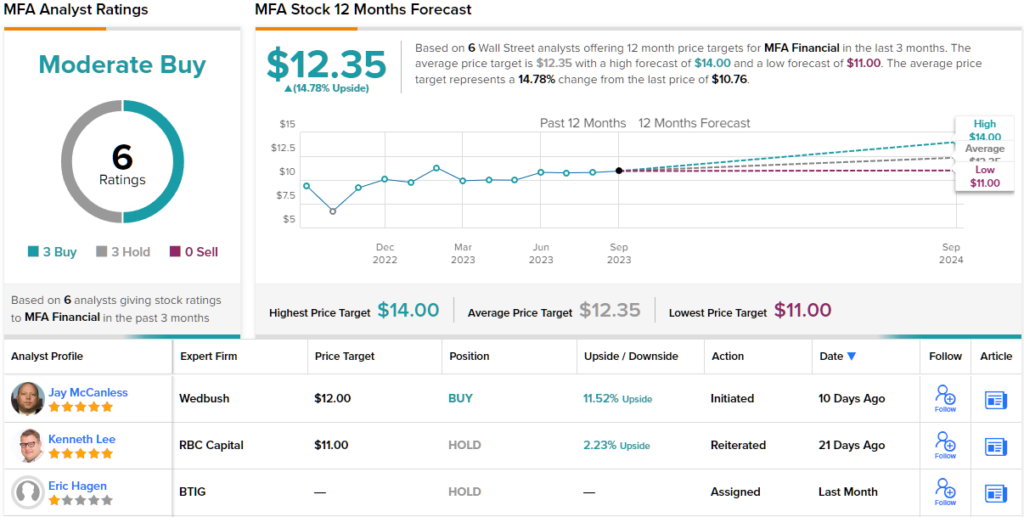

MFA Financial (MFA)

Now, let’s dive into MFA Financial, a real estate investment trust (REIT) that specializes in the residential real estate sector. The company manages residential mortgage assets with leverage, encompassing both residential whole loans and residential mortgage-backed securities (RMBS). The company’s portfolio totals over $8.85 billion as of June 30 this year.

MFA reported total assets at the end of 2Q23 of $9.73 billion. This represented a gain of approximately $620 million in six months. Importantly, more than $329 million of the company’s total assets were in unrestricted cash or cash equivalents, which can be used to support a generous dividend. REITs are required by government regulators to return capital and profits directly to investors, and frequently use dividends to meet that obligation.

The company doesn’t just hold strong cash assets, it also generates a profit. While revenues were down in Q2, falling 15% y/y to $44.5 million, and missed the forecast by over $9.4 million, the company’s EPS was sound. Distributable earnings, the non-GAAP measure of income, came to 40 cents per share, or 6 cents ahead of the forecast. With the company’s cash holdings, this EPS guaranteed full coverage of the quarterly dividend payment.

That dividend was last paid on July 31 at 35 cents per common share. The annualized rate of the current common share dividend, $1.40, gives a sky-high yield of 13%.

This REIT has caught the attention of Wedbush’s 5-star analyst Jay McCanless, who sees the firm’s ability to expand the portfolio and maintain the dividend as key attractions. McCanless writes of MFA, “We expect to see modest net interest margin expansion over the next several quarters, driven by modest loan portfolio growth with higher yields from an increasing mix of business purpose loans. While funding costs are also expected to rise, they should be held in check, at least in the near term, by the company’s swap portfolio, which provided $26 million of positive carry in 2Q23. We also expect a stable and consistent contribution to revenue from Lima One fees and a modest increase in operating expenses over our forecast horizon. At this time, we expect the company’s $0.35 quarterly dividend to hold steady through at least the end of 2025.”

The analyst quantifies his stance with an Outperform (i.e. Buy) rating, and a $12 price target that implies a 10.5% share appreciation in the next 12 months. (To watch McCanless’ track record, click here)

In total, there are 6 recent analyst reviews here, with a 3-3 split between Buys and Holds to give the stock a Moderate Buy consensus rating. The average price target of $12.35 is somewhat more bullish than McCanless allows, suggesting ~15% increase from the current share price of $10.76. That increase, plus the dividend, together point to a return of ~28% in the coming year. (See MFA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.