American Tower Corporation (NYSE:AMT) features several qualities that can insulate the company from market downturns. Consequently, amid challenging market conditions, American Tower could be an optimal choice for investors who are seeking a secure stock that has the potential to maintain its growth in the face of uncertainty.

These qualities, coupled with American Tower’s ~3% yield and robust dividend-growth prospects, are likely to spark boosted investor interest in the company’s shares. Accordingly, I am bullish on the stock.

What are American Tower’s Unique Strengths?

American Tower has put up an impressive track record of growing financials thanks to its unique qualities. Specifically, the company’s revenues have grown every single year without exception since its IPO all the way back in 1998, even in the face of significant economic hurdles such as the Great Financial Crisis and the COVID-19 pandemic.

With the markets bracing for a potential recession in the near term, these very same strengths are poised to once again demonstrate American Tower’s resilience and potentially propel its results to even greater heights. Let’s break them down!

Strength #1: An Oligopolistic Industry

American Tower operates in a niche market of leasing telecommunication towers with only a handful of major players like SBA Communications (NASDAQ:SBAC) and Crown Castle (NYSE:CCI). This oligopolistic structure greatly benefits the company, allowing it to wield considerable pricing power and discourage potential competitors from entering the market.

The latter point is particularly crucial, as the industry’s current state makes it highly unlikely for new players to emerge. The construction and acquisition of telecommunication towers are capital-intensive procedures only feasible for companies with sufficient profitability to support the journey. Without the required capital, it’s basically impossible for new players to enter the space.

The scarcity of players in this market allows American Tower to focus on offering quality services and innovative solutions without having to engage in price wars. In turn, this enables the company to establish a strong and reliable customer base, which is vital in an industry that relies heavily on long-term contracts. This leads us to strength #2.

Strength #2: Long-Term Contracts with Reliable Counterparties

Another strength that American Tower enjoys that should shield its results during a potential economic downturn is its long-term contracts that are backed by reliable counterparties.

More specifically, American Tower’s tenants include all telecommunication majors like AT&T (NYSE:T), Verizon Communications (NYSE:VZ), and T-Mobile US (NASDAQ:TMUS). These tenants typically sign long-term contracts with the company, which range from five to 10 years in length. They are also linked to automatic renewals and rent escalations.

It’s worth noting that the reason the company is able to land such attractive contracts is that telco towers are incredibly critical for telecommunication companies, essentially requiring 100% uptime to adequately serve their customers. Consequently, American Tower enjoys a steady stream of revenue and cash flow over an extended period, forming a predictable and stable business.

Strength #3: Fruitful Economies of Scale

Finally, another strength that American Tower enjoys is the benefits of economies of scale. As the company expands its operations and acquires more towers, it can then spread its fixed costs over a larger number of towers, reducing its operating expenses and increasing its profitability.

Moreover, with the ability to attach multiple antennas in each tower (e.g., hosting a T-Mobile antenna and then adding another antenna from Verizon), the company can increase its leasing revenues without incurring any additional costs, thus driving profitability higher as it scales. This is yet another catalyst that further bolsters the company’s profit margins over time. It also holds true even during a recessionary environment, as telecommunication coverage is an essential service.

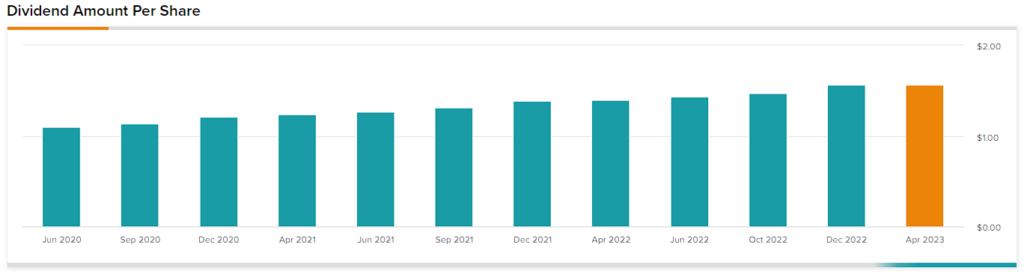

Strong Dividend-Growth Prospects & Decent Dividend Yield

Not only does this company possess distinctive qualities that can protect against a potential market downturn, but its ~3%-yielding dividend can also buffer against any volatility. In line with its consistent revenue growth record, American Tower features a robust dividend history. The company has increased its dividend for 10 consecutive years at a compound annual growth rate of 20.6%.

Although the current pace of dividend growth may seem difficult to maintain, it seems that American Tower is well-positioned to continue supporting significant dividend increases in future years.

To support this argument, management’s outlook for Fiscal 2023 suggests that adjusted funds from operations per share (AFFO/share, a cash-flow metric used by REITs) will range between $9.49 and $9.72, implying a payout ratio of approximately 65% at the midpoint. As a REIT with highly-predictable cash flows, American Tower has the flexibility to deplete its payout ratio even further. This, combined with the company’s underlying growth that will delay this process, indicates a strong likelihood of robust dividend increases in the near future.

Is AMT Stock a Buy, According to Analysts?

As far as Wall Street’s sentiment goes, American Tower features a Strong Buy consensus rating based on 12 Buys and two Holds assigned in the past three months. At $239.85, the average American Tower stock forecast implies 15.9% upside potential.

Conclusion

In conclusion, I believe that American Tower offers a compelling investment case for those seeking a resilient company that can maintain its growth even in uncertain market conditions.

Its unique strengths, including its position in an oligopolistic industry, long-term contracts with reliable counterparties, and economies of scale, should protect it from a potential recession in the near term or at a later time. In the meantime, its strong dividend-growth prospects and attractive yield offer investors notable income potential with limited risks.