Shares of American Tower Corp. (NYSE:AMT) are currently hovering near their five-year lows following an extended decline over the past year. Despite recent share price losses, AMT, which owns and leases nearly 226,000 communication towers, maintains strong potential for robust dividend growth. Combined with the fact that the stock offers a respectable 4% yield at its current levels, I believe that American Tower can be a dividend powerhouse for prospective investors. Hence, I am bullish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

What Has Put AMT Under Pressure?

The surge in interest rates over the past year has cast a significant shadow on American Tower Corp, dampening the company’s profitability outlook. It’s noteworthy that this challenge is recurrent among all REITs, given their reliance on both debt and equity for expanding property portfolios.

In its quest to broaden its tower portfolio, American Tower has steadily accumulated substantial debt, which reached $47.2 billion by the end of Q2. To put this into perspective, the company’s total debt stood at $27.9 billion and $16.2 billion during the same periods in 2019 and 2015, respectively, underscoring the company’s consistent expansion efforts.

The impact of escalating interest rates on the company’s indebted balance was apparent in its most recent quarterly report. In Q2 2023, American Tower’s interest expenses amounted to $348.1 million, reflecting a 25.8% increase compared to the previous year’s $276.6 million. This surge is directly attributable to the higher variable interest rate on the company’s notes.

The substantial rise in interest expenses, unfortunately, overshadows American Tower’s otherwise robust performance. The company posted revenues of $2.77 billion for the quarter, signifying a year-over-year increase of 3.6%. Despite an elevated inflationary environment, the company also maintained its cash allocation for SG&A relatively stable year-over-year. This aided an adjusted EBITDA margin expansion of about 60 bps to 63.1%. Thus, Adjusted EBITDA outpaced revenues, growing by 4.7% to $1.74 billion.

However, factoring in interest expenses, American Tower’s adjusted funds from operations (AFFO) dipped by 0.4% to $1.15 billion. On a per-share basis, this metric declined by 2% to $2.46 due to additional shares issued over the past 12 months to facilitate the company’s acquisitions.

Looking ahead to Fiscal 2023, management anticipates AFFO/share to fall between $9.61 and $9.79, with the midpoint implying a year-over-year decline of 0.6%. This marks the first time in over a decade that the company’s AFFO/share is set to experience a decline.

The Dividend Remains Attractive

Despite the challenging environment created by fluctuating interest rates, American Tower’s dividend remains notably resilient. Sure, management’s guidance suggests a modest decline in AFFO/share compared to the previous year. However, the forward payout ratio still stands at a comfortable 67%, based on the current dividend run rate of $6.48. In the meantime, with shares sinking toward their five-year lows, American Tower’s dividend yield now stands at 4%. It’s the highest yield the stock has ever had.

Note that American Tower’s most recent dividend increase took place a couple of weeks ago, in late September. While the hike was by just 3.2%, it underscores management’s commitment to a growing dividend. It was a prudent hike, but it shows that the company’s payout ratio can support hikes even during a challenging year. Thus, a re-acceleration to the dividend growth rate once the current macro headwinds ease is not unlikely.

Overall, the current 4% dividend yield, combined with the potential for continued increases and the broad strength and enduring qualities of the company, presents a compelling case for income-oriented investors.

These qualities include the resilience and predictability of cash flows attributed to the essential and mission-critical nature of the telecommunications industry. Additionally, the industry’s oligopolistic structure, driven by substantial capital requirements, further solidifies American Tower’s position and provides a robust platform for sustained and predictable growth. Its ability to grow its revenues and expand its EBITDA margin in Q2, despite the tough REIT landscape, is a testament to these strengths.

Is AMT Stock a Buy, According to Analysts?

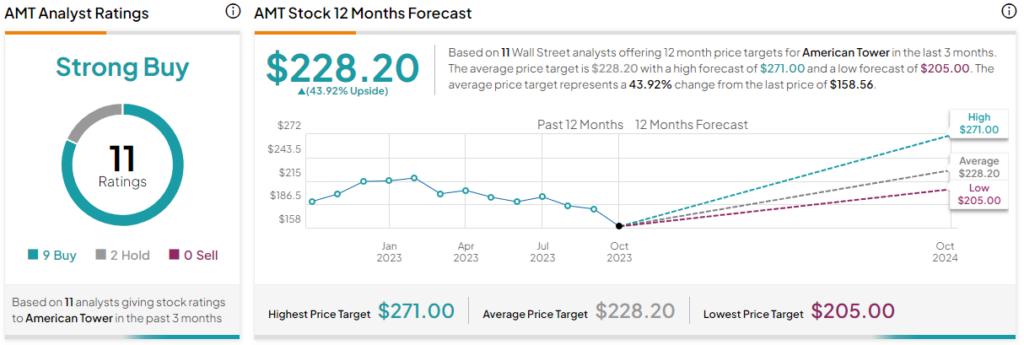

According to analysts, AMT stock comes in as a Strong Buy based on nine Buys and two Holds assigned by analysts in the past three months. The average AMT stock price target of $228.20 implies 43.9% upside potential.

The Takeaway

In conclusion, while American Tower is currently navigating challenges posed by rising interest rates affecting its profitability, the company’s resilient performance and strategic industry position present a compelling opportunity for investors seeking reliable income.

The blend of a 4% dividend yield, a recent dividend hike, and a comfy 67% forward payout ratio create a robust foundation for promising income prospects. This is despite the anticipated decline in AFFO/share for Fiscal 2023.

Further, the enduring qualities of the telecom towers industry, marked by essential service provision and oligopolistic dynamics, enhance American Tower’s potential for sustained and predictable growth. Thus, the stock stands out as an appealing choice for those seeking a growing income and stability.