Heading into Advanced Micro Devices’ (AMD) Q1 report, a popular view on Wall Street was that the chip giant should meet expectations for the quarter but will probably struggle with the outlook on account of weakness in the data center segment. And that’s more or less how it turned out.

Protect Your Portfolio Against Market Uncertainty

- Discover companies with rock-solid fundamentals in TipRanks' Smart Value Newsletter.

- Receive undervalued stocks, resilient to market uncertainty, delivered straight to your inbox.

AMD reported revenue of $5.353 billion, amounting to a 4.4% sequential drop and down 9.1% year-over-year, but above the Street’s $5.3 billion forecast. Both data center and PCs sales declined with the former down by 22% quarter-over-quarter and the latter falling by 18% sequentially and by a larger 65% from the same period a year ago. However, the Embedded segment (mostly Xilinx) put in a strong performance, up by 11.8% quarter-over-quarter and now representing 29% of sales. As for the profitability profile, AMD dialed in adj. EPS of $0.60, higher than the $0.56 anticipated by the analysts.

The outlook came in soft, though. For Q2, the company sees revenue coming in around $5.3 billion, give or take $300 million, compared to consensus at $5.52 billion. Additionally, AMD guided for gross margins of 50% for Q2, flat QoQ and amounting to a 400bps y/y drop whilst coming in just below the analysts’ 50.4% forecast.

The Street was not particularly impressed and, as of this writing, shares are down ~9%.

Ahead of the print, Morgan Stanley analyst Joseph Moore was amongst those predicting a disappointing outlook, and he concedes that even for Q1, data center and PCs were “weaker than expected.” However, looking further down the line, he remains convinced that AMD is “setup well” for the second half of the year.

“Overall, then, this is a mixed quarter, but given the selloff we remain positive on the story,” Moore went on to say. “The businesses that investors focus on – microprocessors and graphics processors for PC and data center – are poised to grow nicely from here, with large 2h snapback potential, with strong product related ramps in every area. The growing view that Intel is executing better with its server roadmap is not something that we have heard from cloud customers, who remain committed to AMD for large and important projects.”

All told, then, Moore sticks with an Overweight (i.e., Buy) rating although the price target has been lowered from $102 to $97, now suggesting shares will climb 18% higher over the coming months. (To watch Moore’s track record, click here)

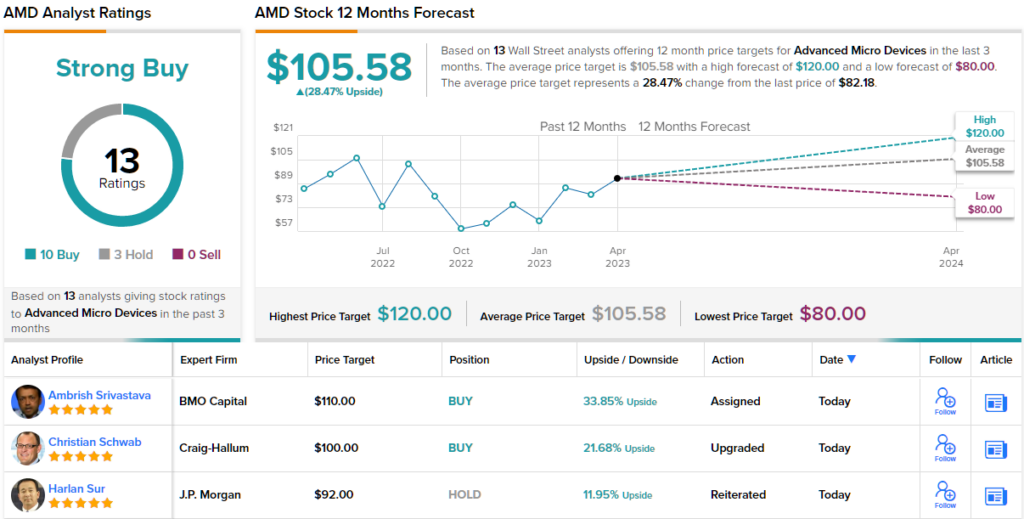

Most on the Street remain in AMD’s corner. The analyst consensus rates the stock a Strong Buy, based on 10 Buys vs. 3 Holds. At $105.58, the average target makes room for one-year gains of 28%. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.