The Advanced Micro Devices (NASDAQ:AMD) AI bull case took a while to reveal itself but is now looking a lot firmer following the announcement of two blockbuster deals.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Earlier this week, AMD and Oracle revealed a deal under which Oracle Cloud Infrastructure will start an initial rollout of 50,000 AMD MI450 chips in 3Q26, with plans to expand the deployment further from 2027 onward. This announcement came shortly after AMD and OpenAI unveiled a partnership aimed at deploying six gigawatts of AI capacity powered by AMD technology.

These developments have not gone unnoticed by Wedbush’s Matt Bryson, an analyst ranked among the top 1% on Wall Street. When Bryson last previewed AMD’s earnings, he noted that for his projections to push higher, he would need significantly more positive updates on AMD’s 350 and 400 series GPUs – progress that would enable the analyst to “substantially bolster” his datacenter GPU estimates.

Well, the Lisa Su-led company has taken on that challenge with aplomb. “Over the last quarter, AMD has clearly provided future certainty around GPU demand announcing new agreements that promise to substantially lift future GPU revenues,” the 5-star analyst said.

Even accounting for potential overlap between the two announcements – since much of OCI’s future capacity seems intended to meet OpenAI’s needs – Bryson estimates that each gigawatt of capacity could translate to roughly $20 billion in AMD product demand. This suggests the OpenAI partnership alone could “dwarf” Bryson’s previous forecasts, which anticipated total revenues of about $20 billion across 2026 and 2027 combined.

As a result, the analyst has made upward revisions to forward estimates. For Q3 and Q4, Bryson has raised his forecasts slightly to reflect stronger-than-expected demand in both PC and server compute, which he believes primarily benefits AMD. His datacenter GPU projections for this period remain largely unchanged.

Looking ahead to next year, Bryson has increased his datacenter GPU and AI estimates for the second half, particularly in the third and fourth quarters. Bryson now sees 2026 EPS of $5.81, revenue of $40.3 billion, and gross margins of 55.5%, vs. previous projections of $5.62 in EPS, $38.8 billion in revenue and 55.5% gross margins. Still, even with this upward adjustment, Bryson’s forecast for total AI datacenter revenue in 2026 remains around $10 billion, as he expects AMD’s revenue ramp to take a bit longer.

By 2027, however, Bryson anticipates AMD will be supplying a significant share of a gigawatt of capacity to OpenAI, driving AI-related revenue to about $20 billion. Consequently, even after factoring in higher operating expenses in line with revenue growth, he now sees EPS rising sharply to $9 in 2027, up from $5.81 in 2026.

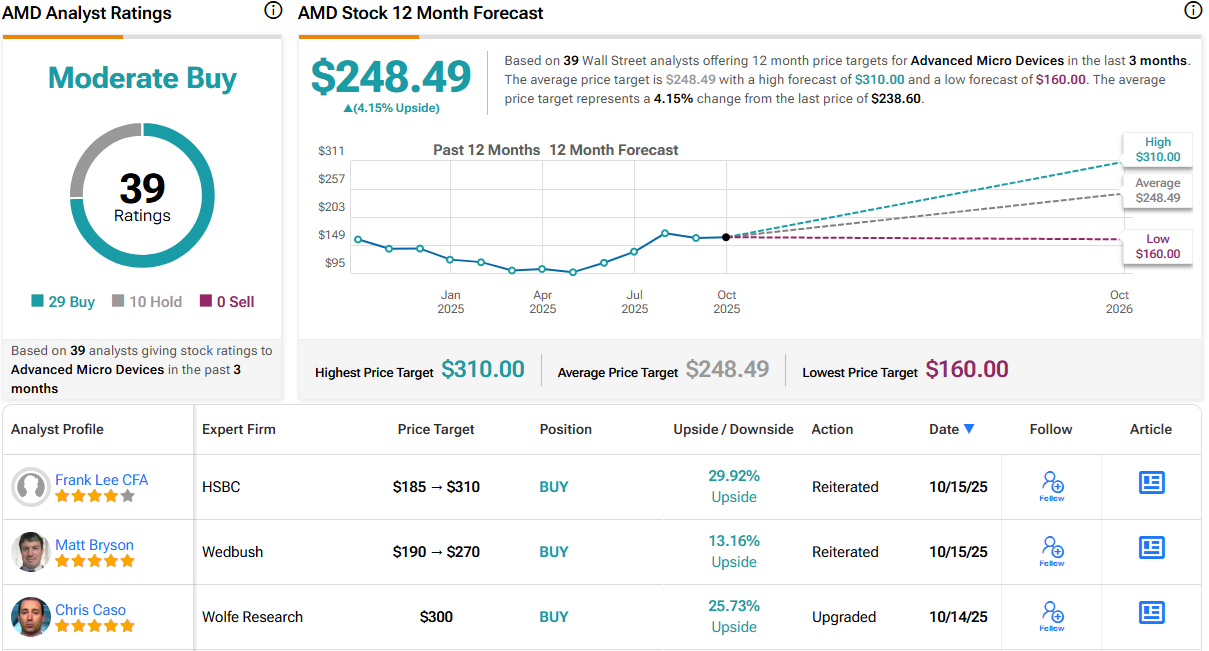

All of that merits a new price target, which goes from $190 to $270, suggesting the stock will gain 13% over the coming months. Bryson’s rating stays an Outperform (i.e., Buy). (To watch Bryson’s track record, click here)

29 other analysts also back AMD’s case, while 10 Holds can’t detract from a Strong Buy consensus rating. However, the big recent gains (up 170% over the past 6 months) now leave room for just modest one-year upside of 4%. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.