By next week, many of the market heavyweights will have already dialed in their latest earnings, but that doesn’t mean the reporting season is over. There are many more interesting financial statements on the way, amongst them one from retail favorite AMC Entertainment (NYSE:AMC), slated to announce Q2 results on Tuesday, August 8, after the market close.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

With an improving release slate in 2023, ahead of the print, Wedbush analyst Alicia Reese notes that theatrical exhibition is “on the path to normalization.”

According to Reese’s estimates, the 2023 North American box office will show a 20% improvement compared to 2022, reaching ~78% of 2019 pre-Covid box office. And with its vast network of premium large format screens, Reese sees AMC “at least maintaining its 22% market share if not expanding.”

Reese also anticipates the Q2 performance will come in better than consensus expectations. She is calling for revenue of $1.305 billion and adjusted EBITDA of $170 million vs. the respective $1.274 billion and $146 million the Street is forecasting. Reece’s forecast for EPS of $(0.04) is in line with consensus. Elsewhere, the analyst sees domestic revenue reaching $1.032 billion, with attendance showing a 7% year-over-year increase and tickets up 8%.

Reese is also looking toward “positive commentary about the successful Barbie and Oppenheimer runs to-date in both the domestic and European markets.”

“We also expect an overall optimistic view on the company’s ability to mitigate any negative impacts of the ongoing labor strikes, should they end in the next one to two months,” the analyst further said.

If that all sounds like quite the endorsement, then think again. The company is involved in a court case over the conversion of its preferred APE units – a judge last month rejected a settlement that would have allowed the conversion – and that, along with other issues, has serious implications for the business.

“In spite of recent box office successes, AMC is instead concerned with its cash requirements, APE shares falling, and the writers’ and actors’ strikes persisting,” Reese explained. “What may not be clear to AMC’s shareholders is that if the company is unable to convert APE shares, AMC will be forced to issue significantly more APE shares to cover its upcoming cash requirements. This will result in significantly more dilution for the company’s overall outstanding share count.”

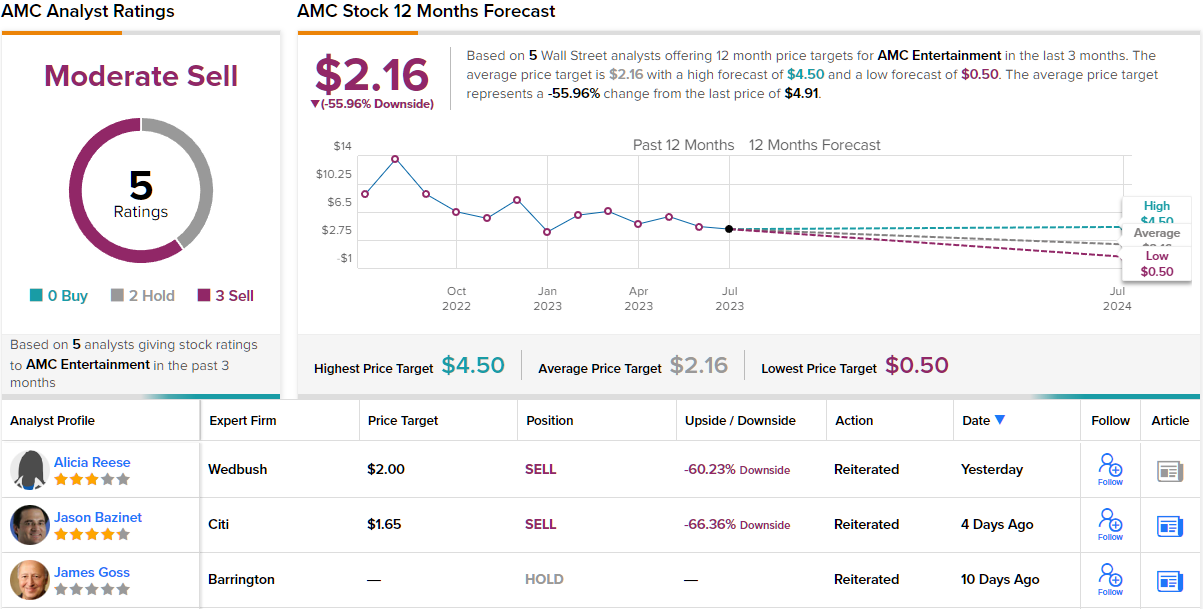

For now, then, Reese sticks with an Underperform (i.e., Sell) rating and $2 price target, suggesting shares are overvalued to the tune of ~60%. (To watch Reese’s track record, click here)

Overall, 2 other analysts join Reese in the bear camp while 2 remain on the sidelines, all culminating in a Moderate Sell consensus rating. The $2.16 average target is slightly above Reese’s objective and implies shares will drop 56% from here. (See AMC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.