Amazon (NASDAQ:AMZN) stock appears to be trading at an absurd valuation following the stock’s rally of more than 46% year-to-date. Investors’ confidence in the stock has likely been powered by a strong recovery in the shares of most mega caps, fueled further by the frenzy surrounding AI-related companies (with notable advancements in AI being made by Amazon).

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

However, I harbor significant skepticism regarding Amazon’s ability to maintain its current stock price levels, given the company’s persistently feeble profitability prospects. Despite the robust cash flows generated by AWS, its growth has been steadily decelerating.

Meanwhile, its retail division persists in grappling with the challenge of achieving substantial margins. Given that interest rates remain elevated and that Amazon may have a hard time growing into its current and forward valuation multiples, I am bearish on the stock.

AWS Growth Slowing Down

Amazon’s crown jewel is its AWS segment, which carried the company’s expansion over the years through its strong, profitable growth. However, the segment’s growth has been on a gradual deceleration trend. In Amazon’s most recent fiscal Q1 results, the AWS division grew by just 16%. This was lower than the previous quarter’s (Q4 2022) AWS growth of 20%, Q3-2022’s growth of 27%, Q2-2022’s growth of 33.3%, and Q1-2022’s growth of 37%.

You can clearly identify the pattern of sequential deceleration between each quarter, with the cloud market maturing fast and competitors such as Alphabet’s (NASDAQ:GOOGL)(NASDAQ:GOOG) Cloud and Microsoft’s (NASDAQ:MSFT) Azure fighting fiercely for market share.

In the meantime, AWS’ profitability seems to have a hard time scaling. AWS’ operating income declined by 26% in constant currency year-over-year to $5.1 billion. What’s even more concerning is the sequential decline in operating income between each and every quarter since the previous year, where it stood at $6.5 billion.

These figures raise red flags, as they suggest that AWS is struggling to maintain its dominance in the face of fierce competition. This is particularly evident when we compare it to Azure, Microsoft’s cloud platform, which demonstrated a remarkable sustained growth of 27% (or 31% in constant currency) in its most recent results. Similarly, Google’s Cloud division also achieved significant growth of 28% in Alphabet’s latest results.

Can the Retail Division Turn a Profit?

With AWS profitability prospects shrinking in recent quarters, Amazon may have a hard time offsetting its retail division’s inability to achieve meaningful levels of net income. The North American retail segment delivered an operating income of $0.9 billion, which was an improvement from last year’s operating loss of $1.6 billion. However, even now, this suggests an operating income margin of just 1.2%.

In the meantime, the International retail segment continues to lose money constantly. In fact, operating losses amounted to $1.2 billion, stable year-over-year, more than offsetting North America’s operating income of $0.9 billion. In other words, Amazon’s retail segment is consistently operating at a loss, which raises significant concerns.

It is surprising that despite reaching a substantial scale, Amazon has not been able to leverage its economies of scale to generate a profit. Considering that Amazon is no longer in its early expansion phase and has established global dominance, one can’t help but wonder when the company will be able to achieve profitability in its retail division.

Is AMZN Stock a Buy, According to Analysts?

Turning to Wall Street, Amazon continues to boast a Strong Buy consensus rating based on 37 Buys and one Hold assigned in the past three months. At $137.62, the average Amazon stock price prediction suggests 9.3% upside potential.

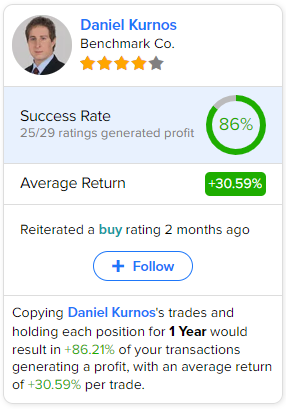

If you’re wondering which analyst you should follow if you want to buy and sell AMZN stock, the most accurate analyst covering the stock (on a one-year timeframe) is Daniel Kurnos from Benchmark Co., with an average return of 30.59% per rating and an 86% success rate.

Takeaway – Amazon May Not be Able to Grow Into Its Valuation

Overall, I believe that due to AWS’ decelerating growth and declining operating income, as well as the retail division’s inability to post noteworthy profits, Amazon may not be able to grow into its current and forward valuation multiples.

Wall Street expects that the company will deliver earnings per share of about $1.56 this year based on consensus estimates and $2.59 per share in Fiscal 2024. This implies a P/E of roughly 80 for this year or a forward P/E of about 48 based on next year’s earnings. Both multiples are completely absurd in the current market environment, even as the equity markets seem to be undergoing a recovery. For reference, the S&P 500’s (SPX) forward P/E multiple is around 20.

Besides, there remains considerable uncertainty regarding Amazon’s ability to meet these earnings projections, given the underwhelming performance of both AWS and the retail division. But even in the event that Amazon manages to meet or surpass these estimates, the current valuation multiples appear disproportionately inflated relative to the valuation of most large/mega caps and the relatively high interest rates.

In light of this, it is unlikely that significant upside is on the horizon, as the market would be imprudent to push these already lofty multiples even higher. Given the absence of a substantial margin of safety and the limited potential for further gains, my perspective on Amazon stock is contrarian, leaning towards a bearish outlook.