Amazon’s stock (NASDAQ:AMZN) has rallied by an impressive 66.7% year-to-date. The big question is whether it’s a wise move to chase the stock. The current momentum behind the e-commerce and cloud behemoth is undeniably enticing, whether you’re considering adding to your existing position or initiating one. However, my optimism wanes when I look at Amazon’s current stock price. Despite some positive Q2 highlights, the stock’s current valuation is very difficult to justify. As a result, I’m neutral on AMZN stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Amazon’s Retail Business is Growing, but Profits Remain Thin

Amazon’s retail business has historically held back the company compared to its rapidly growing AWS segment. Nevertheless, growth in retail resumed in Q2, and the company was even able to reverse last year’s operating loss into an operating profit.

Specifically, the North American Retail division posted net sales of $82.5 billion, implying a year-over-year increase of 10.9%. The division’s operating profit also came in at $3.2 billion, greatly improving from last year’s operating loss of $627 million.

While Amazon’s North American Retail division undoubtedly marched in the right direction in Q2, when we step back to examine the broader perspective, the overall outlook appears less enchanting. In fact, the $3.2 billion in operating income still implies an operating margin of just 3.9%. This suggests the following two issues:

- Firstly, the division’s net income (although not directly reported) is even thinner when accounting for the interest expenses (due to debt) related to that segment.

- Secondly, such a thin margin means that operating income can easily turn negative again during unfavorable trading periods. This includes temporarily weaker consumer demand or inflation pressuring Amazon’s expenses.

In the meantime, Amazon’s International Retail business continues to record losses. The division’s sales grew by 9.6% to $29.7 billion. However, its operating loss came in at $895 million. That’s a lot of money to lose on an operating level from a business that’s supposed to have matured significantly at this point.

AWS Growth Decelerates, Profit Margins Shrink

Turning to the AWS segment, I believe that Amazon’s crown jewel is losing its appeal. For starters, the segment’s growth has been gradually decelerating. Just take a look at AWS’ revenue growth rate in recent quarters:

- Q1-2022: 37%

- Q2-2022: 33%

- Q3-2022: 27%

- Q4-2022: 20%

- Q1-2023: 16%

- Q2-2023: 12%

The gradual sequential deceleration couldn’t be more evident. At its current pace, I wouldn’t be surprised if the segment’s growth were to slip into the single digits in Q3-2023. So, what’s the reason behind this gradual deceleration? The answer is very straightforward — rising competition. The days when AWS was roaming freely in Cloudland are over. Alphabet’s (NASDAQ:GOOGL)(NASDAQ:GOOG) Cloud and Microsoft’s (NASDAQ:MSFT) Azure are constantly battling for market share.

This is evident in both these companies’ cloud segments, whose higher growth rates suggest they are capturing market share faster. Specifically, Alphabet’s Google Cloud grew its revenues by 28%, while Microsoft’s Azure grew its revenues by 26% during the same period.

If that didn’t signal bad news already, AWS’ operating income declined compared to last year. It landed at $5.4 billion compared to $5.7 billion in the prior-year period. Clearly, this result demonstrated the effect growing competition can have on a company’s ability to scale its profitability. Amazon seems to be investing more in AWS to remain competitive, and even then, the segment’s growth can’t really impress.

Has Amazon’s Valuation Run Ahead of Itself?

In my view, Amazon’s valuation may have run ahead of itself following the stock’s year-to-date rally. On the one hand, Amazon’s total operating income improved in its most recent Q2 results, primarily due to the North American retail division reversing last year’s operating losses. On the other hand, I just cannot see how Amazon can make enough money in the coming years to justify its $1.46 trillion market cap.

For context, consensus estimates point to Amazon reporting EPS of $2.17 this year. This implies an absurd forward P/E ratio of about 65x. While EPS is expected to grow further to $3.03 in fiscal 2024, again, that implies a very rich P/E of around 46.6. These forward multiples are notably higher than those of the S&P 500 (SPX) and most mega-cap stocks. Given the razor-thin margins in the retail segment and the declining profits in AWS, it’s very hard to argue that Amazon stock is not overpriced at its current levels.

What are Analysts Saying About AMZN?

Turning to Wall Street, Amazon continues to boast a Strong Buy consensus rating despite its elevated valuation. This is based on 39 Buys and one Hold assigned in the past three months. At $175.63, the average Amazon stock price target suggests 24.4% upside potential.

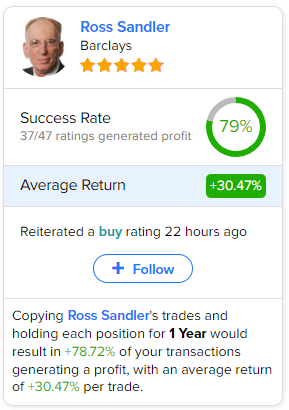

If you’re wondering which analyst you should follow if you want to buy and sell AMZN stock, the most profitable analyst covering the stock (on a one-year timeframe) is Ross Sandler from Barclays, with an average return of 30.47% per rating and a 79% success rate. Click on the image below to learn more.

The Takeaway

Overall, while Amazon’s year-to-date rally may be tempting to chase, caution is warranted. Despite some positive developments in Q2, the stock’s current valuation appears stretched and challenging to justify.

The Retail segment’s thin margins and the deceleration in AWS growth due to increased competition raise concerns about the company’s ability to sustain its current valuation. With an exorbitant P/E ratio versus most market benchmarks, it’s hard to ignore the possibility that Amazon stock could undergo a valuation compression, shedding away its recent gains. Accordingly, I remain neutral on AMZN stock.