Altria Stock (NYSE:MO) has recently embraced an aggressive buyback strategy. Given the rather lasting downward pressure on shares, strategically repurchasing them at favorable prices stands poised to boost investor confidence in the stock. Yet, Altria’s sales figures seem to be worsening faster than ever. Sales of smokeable products sustain steep declines. Further, intensified competition from Philip Morris (NYSE:PM) in oral nicotine appears to hamper Atlria’s investment case. Thus, I am now bearish on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Q1-2024: Weakness All Around

Seeing Altria post weak results in the Smokeable Products division hardly comes as a surprise. We’ve seen this happen quarter after quarter. It stems directly from a declining number of smokers, compounded by fierce competition from alternatives like heated tobacco and oral nicotine products.

Up until recently, I maintained a rather bullish outlook on Altria. I supported the idea that its own oral tobacco products, along with price hikes in smokeable products, would sort of offset this deterioration. However, the situation appeared quite uglier in the company’s most recent Q1 results. Not only did Altria continue to post heavy sales volume declines in Smokeable Products, but its oral tobacco products also appeared to face severe headwinds, likely attributable to intensified competition from Philip Morris.

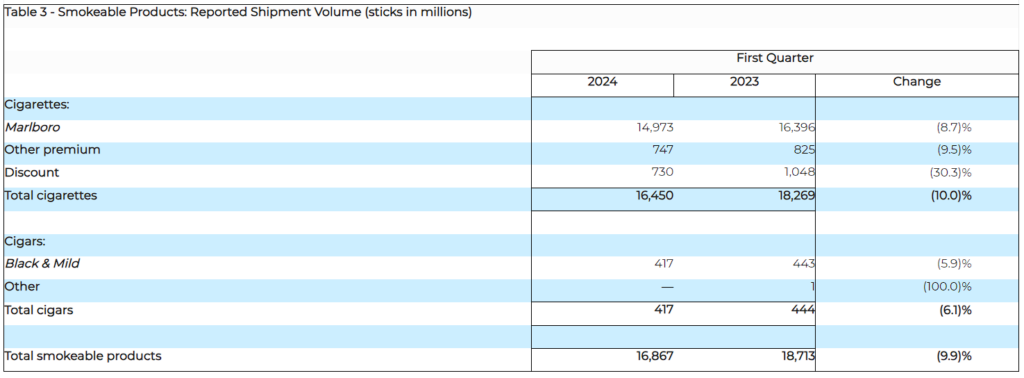

As evident from the table below, Altria saw significant declines in shipment volume within its Smokeable Products division. Sales of cigarettes, including its famous Marlboro brand and other premium and discount brands, continued to plummet. Even its cigars, once showcasing rather consistent sales due to their unique appeal, witnessed a notable downturn in sales volumes.

Altria has consistently responded to sales volume declines in its Smokeable Products division by enforcing price increases. Historically, this approach has proven somewhat effective. In Q1, the company maintained this strategy, roughly neutralizing the overall decline in smokeable product sales to about 3.6% through price increases. However, new concerns have surfaced, as Altria’s non-smokeable products are also experiencing declining shipment volumes.

In particular, despite the growing global demand for oral nicotine products, driven by the perception of a healthier alternative for nicotine consumption, Altria’s sales trajectory doesn’t align with this trend. At first glance, net revenues in the company’s Oral Tobacco division increased 3.7%. However, this was primarily driven by higher pricing, with total shipment volumes in the division actually declining by 3.1%.

The ongoing headwind seems to be attributed to increased competition from Philip Morris. Note that Philip Morris doesn’t really compete with Altria in the cigarette market, with its exclusive Marlboro and other brand rights targeting international markets. However, the company competes with Altria in the oral tobacco space, especially following the acquisition and integration of Swedish Match. And, unfortunately for Altria, Philip Morris is taking the U.S. market by storm.

Specifically, in Q1, Philip Morris achieved shipment volume growth of 40.0% in cans or 35.8% in pouches and pouch equivalents. This was fueled by Zyn nicotine pouch growth in the U.S., the brand acquired by Swedish Match, whose shipment volumes reached 131.6 million cans, celebrating year-over-year growth of 79.7%. Clearly, there is a direct connection between Philip Morris’s success and Altria’s falling volumes and the loss of market share in the space.

Accelerated Buybacks Help, But Don’t Solve the Core Issue

In late March, Altria’s management announced a $2.4 billion accelerated share buyback program in an attempt to bolster investor confidence in the stock. Shares were bought back from Morgan Stanley (NYSE:MS) and Goldman Sachs (NYSE:GS) in separate transactions. These trades were part of Altria’s previously announced extended $3.4 billion share repurchase program, which is expected to be concluded by this year’s end.

Altria received some additional cash following the sales of 35 million shares of Anheuser-Busch InBev (NYSE:BUD), so it makes total sense to retire some of its own shares at what appears to be a discounted valuation. Indeed, these repurchases helped to somewhat offset the company’s heavier revenue and net income decline, with adjusted EPS falling by just 2.5% in Q1 due to a lower share count.

Nevertheless, Altria’s ongoing buybacks don’t solve its core issue: declining sales across the board. I was previously more optimistic about the company’s future, hoping that the company’s Oral Tobacco division would be a long-term growth driver. Yet, with intense competition exacerbating the enduring challenges within the Smokable Products division, my optimism has waned considerably.

Is Altria Stock a Buy, According to Analysts?

Regarding Wall Street’s sentiment on Altria, the stock has a Hold consensus rating based on three Buys, two Holds, and two Sells assigned in the past three months. At $43.44, the average Altria stock forecast implies 0.9% downside potential.

The Takeaway

Overall, while Altria’s aggressive buyback plan may temporarily boost investor confidence, it fails to address the company’s underlying challenges.

Despite efforts to mitigate declining sales through price increases and share repurchases, Altria continues to grapple with declining demand for its smokeable products. Further, it appears that Altria is also facing increasing competition in the oral tobacco market, particularly from Philip Morris.

As such, my outlook on Altria has shifted to a bearish stance, reflecting the company’s ongoing struggle to find sustainable growth avenues in the face of mounting pressures.