Alphabet (NASDAQ:GOOGL) (NASDAQ:GOOG) is on the brink of revealing its Q3 results (it will report them on October 24), and investors are eager to see if the strong momentum from Q2 will persist. Following a surprising performance last quarter, where Alphabet exceeded both top- and bottom-line estimates, there’s a reasonable expectation that the company’s positive trajectory will endure. Consequently, my outlook on the stock remains bullish.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Building on Q2 Momentum

Alphabet’s Q3 results are likely to be robust, building on the impressive momentum witnessed in the preceding quarter. The company’s Q2 showcased a remarkable surge across all facets of the business, resulting in revenue growth of 9% (in constant currency) to $74.6 billion and a 19% increase in earnings per share to $1.44 compared to the previous year. This not only beat Wall Street’s revenue growth consensus estimate by 2.5% but also beat its EPS estimate by 7.3%, sparking a significant rally in the stock.

The Advertising Business: Robust Despite Headwinds

A standout feature of Alphabet’s Q2 performance was the resilience of its Advertising business, defying a challenging macroeconomic environment. Economic uncertainty regarding a potential decline in consumer spending and the added concern of rising interest rates could have affected ad revenues. Yet, Alphabet posted a solid 3.2% growth in ad revenues to $58.1 billion. This success is especially noteworthy given the comparison to the strong performance of Q2 2022, a period of robust global ad spending.

Google Search Advertising & Search

In its Google Search Advertising & Search division, the company saw notable 4.7% year-over-year revenue growth, driven by a rebound in the retail industry. Further, it’s worth noting that despite AI advancements, Search was not affected at all by potential competitors. While ChatGPT was initially perceived as a killer to Google’s business model, Search apparently remains highly resilient.

I anticipate that Search will continue to gain significant traction in Q3, thanks to the robust product resilience coupled with Google’s integration of AI, thereby solidifying its dominant position in the market. Notably, in Alphabet’s Q2 earnings call, management emphasized that nearly 80% of advertisers are already leveraging at least one AI-powered Search ads product. This is poised to enhance the firm’s return on ad spend (ROAS), suggesting a promising outlook for robust revenue growth in the upcoming results.

YouTube & Shorts

I am equally excited about Alphabet’s YouTube division, which also performed admirably in Q2, achieving revenue growth of 4% to $7.7 billion. Noteworthy is the milestone of YouTube Shorts, which now engages a staggering two billion logged-in users monthly. That’s very impressive, given that Shorts was Introduced just a year ago. As creators seamlessly incorporate Shorts as a vertical extension to their long-form videos within the platform, I am optimistic that the platform will maintain its strong momentum throughout Q3.

Google Cloud: Now Growing Profitably

Building on its exceptional Q2 performance, the Google Cloud business recorded a remarkable 28% year-over-year revenue increase, reaching an impressive $8.0 billion. Noteworthy is the consecutive second quarter of positive Cloud operating profits, underscoring the company’s ability to sustain consistent profitability in this rapidly expanding business.

Google Cloud showcased strong financial performance, achieving an operating income of $395 million with a notable 5% profit margin. Alphabet’s ongoing integration of AI capabilities into its Cloud offerings continues to drive growth. A prime example is Pfizer (NYSE:PFE), now utilizing Google Cloud to improve its security operations, showcasing the tangible success of this strategic focus.

Given the upcoming potential cross-selling initiatives for the company’s extensive AI offerings, my confidence in Google Cloud’s growth potential remains strong. Consequently, I anticipate a commendable performance reflected in Alphabet’s Q3 results for this particular business segment, too.

What Does Wall Street Expect from Alphabet in Q3?

Given Alphabet’s strong momentum coming off of Q2, as well as the fact that the macroeconomic environment hasn’t worsened notably since then, Wall Street expects another quarter of strong results.

Revenue expectations for the quarter come in at $75.76 billion, implying a year-over-year increase of 9.65%. Analysts also predict a substantial year-over-year increase of 36.4% in earnings per share, landing at $1.45, driven by higher revenues and operating efficiencies following Alphabet’s strategic measures over the past year (including layoffs).

Is GOOGL Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, Alphabet features a Strong Buy consensus rating based on 30 Buys and four Holds assigned in the past three months. At $151.06, the average Alphabet stock forecast implies 9.5% upside potential.

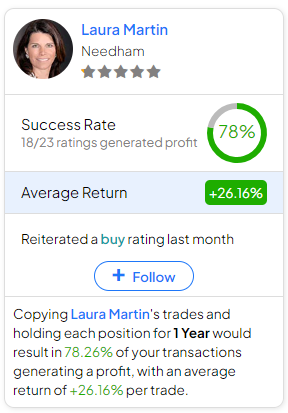

If you’re wondering which analyst you should follow if you want to buy and sell GOOGL stock, the most profitable analyst covering the stock (on a one-year timeframe) is Laura Martin from Needham, boasting an average return of 26.16% per rating and a 78% success rate.

Conclusion

Overall, Alphabet’s strong momentum witnessed in Q2 is expected to persist, with robust performances across its Advertising, YouTube, and Google Cloud divisions. The company’s resilience in the face of economic challenges, coupled with advancements in AI integration, positions it favorably.

With Wall Street anticipating strong Q3 results, the forecasted revenue and earnings growth reinforce my bullish outlook on Alphabet’s stock. Consequently, I plan to hold my shares and capitalize on any opportunistic dips to further enlarge my position.