Regional bank stocks rallied sharply on Friday, giving some hope for a possible recovery, after a recent slump caused by the collapse of First Republic Bank. The question now is, was that a real lift or a classic ‘dead cat’ bounce?

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Offering his insights, Brett Rabatin, an analyst at the Hovde Group, described the recent sell-offs in the banking industry as a ‘rare opportunity.’ Despite concerns regarding potential bank failures, Rabatin believes that the sector may have reached a bottom.

J.P. Morgan analyst Steven Alexopoulos is also in the bull camp. “With sentiment this negative, in our view it won’t take much to see a significant intermediate-term favorable re-rating of regional bank stocks,” he said. “Meantime, we see the favorable updates coming from select banks that deposit balances have remained stable (or increased) helping to counterbalance very negative sentiment.”

So let’s zoom in from the macro, and look at two regional banks, PacWest and Western Alliance. Each saw extreme volatility last week, ending with a spike in share price. Here are the details, along with comments from one of Wall Street’s top professionals on TipRanks, a platform that ranks analysts based on their past performance.

PacWest Bancorp (PACW)

We’ll start with PacWest. This Beverly Hills-based bancorp operation has one wholly owned subsidiary, the Pacific Western Bank. The banking operations include the usual services offered by a ‘relationship-based community bank,’ from personal and commercial banking and deposits, loans, and mortgages to small business and real estate finance and venture lending. The bank serves small- and mid-market businesses, including venture-backed firms.

PacWest is focused mainly on its home state of California, where it has 67 service branches. The company also has two additional branches, located in Denver, Colorado and in Durham, North Carolina. Working through its branches, the bank had $44.3 billion in total average assets through the first quarter. That total included averages of $25.7 billion in loans and $28.2 billion deposits.

Of the two stocks we’re looking at here, PacWest has seen the harder spin from volatility. In fact, with its six-session losing streak and 71.4% price collapse to a record low by May 4, PacWest helped lead the regional banks down – while also showing its worst six-day run since entering the public markets bank in 2000.

But what goes down can come back up, and PacWest led the regional banks in their collective rebound. The California banking firm posted a powerful gain of 81.7% by the time trading closed for the week, and its upward momentum was so strong that PACW shares had their trading halted several times on Friday due to excessive volatility.

One factor that helped to buoy PacWest was the dose of good news in the bank’s recent update on its uninsured deposit coverage status. The recurring bank failures have depositors worried about their cash – but PacWest was able to assure them that, while it holds $8.1 billion in uninsured deposits as of the end of 1Q23, it also has total liquidity, in cash on hand and undrawn credit, of $12.4 billion. This gives the bank a healthy coverage ratio of 153%, and gives confidence to both depositors and investors.

RBC 5-star analyst Jon Arfstrom takes a sanguine view PACW, noting: “The deposit update is helpful as it shows relatively stable balances, the available cash and liquidity to uninsured deposit levels have increased since quarter end, borrowings are down, and the company is actively considering other options, which we and others had expected and management had openly discussed on the past earnings calls.”

“Like we mentioned [already], being in the stock requires an ability to handle higher volatility and also the ability to react to the news flow that seems to follow the company at this point. The update from PacWest shows stability at the company and some continued improvement in the trends as evidenced by the lower borrowings and a higher liquidity to uninsured ratio,” Arfstrom added.

Looking forward, Arfstrom sees room for a $17 price target on PACW, consistent with his Outperform (Buy) rating, and suggesting a robust one-year upside of 195%. (To watch Arfstrom’s track record, click here)

While the RBC view is bullish, the Street still gives PACW shares a Hold rating, based on 8 recent reviews that include 2 Buys and 6 Holds. The shares are trading for $5.76 and the average price target, of $17.20, is a shade more bullish than Arfstrom’s, implying a gain of 198% in the next 12 months. It will be interesting to see whether the analysts update their targets or change their ratings shortly. (See PACW stock forecast)

Western Alliance Bancorporation (WAL)

The second stock we’re looking at is Western Alliance Bancorporation, a premier banking company in the United States, boasting assets exceeding $65 billion. Its flagship subsidiary, Western Alliance Bank, was ranked as the best-performing large bank with assets greater than $50 billion in 2021 by both American Banker and Bank Director. With a nationwide presence, Western Alliance Bank operates as a full-service financial institution with individual banking and financial brands strategically located in key markets across the country.

Earlier last week there was a run on WAL shares, as word spread that the bancorp was exploring a possible sale of all or most of its assets. In the context of recent events (that unforgettable forced sale of First Republic to JPM), the rumor had legs – and was not dispelled until Western Alliance issued a formal press release categorically denying that it has looked into such a transaction. Backing its stance, the company has even said that it is exploring ‘legal options’ in response to news reports on the subject.

By week’s end, WAL had shifted around enough to give the most steadfast investor a bad case of vertigo. The stock ended the week with a 49% jump in Friday’s session. However, its price remained below the level at which it was trading before the drop.

In his coverage for RBC, analyst Jon Arfstrom makes a case for staying bullish on WAL. He writes: “Western Alliance provided us with detailed intra-quarter deposit and capital information and capital ratios were up and deposits continued the positive trend that has been occurring since the depths of the crisis in mid to late March. We like the fundamental trends at Western Alliance and believe they have a viable path to achieving their deposit growth goals and meeting their expectations they discussed on their earnings call.”

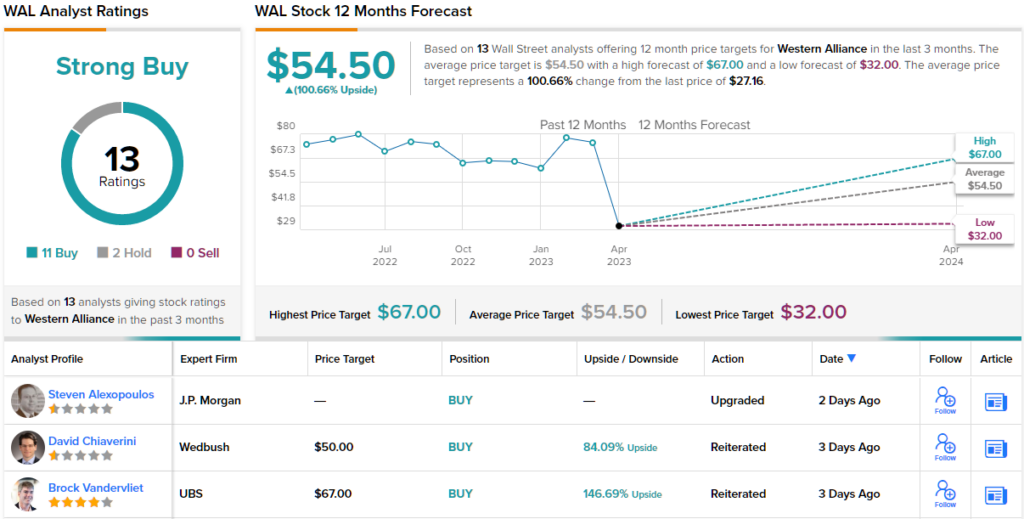

Showing his confidence in WAL, Arfstrom rates the stock as Outperform (i.e. Buy), and his $59 price target implies a robust 117% upside for the next 12 months.

Most of Arfstrom’s colleagues on Wall Street also remained unfazed by the recent volatility. Based on 11 Buys vs. 2 Holds, the stock boasts a Strong Buy consensus rating. Moreover, the $54.50 average price target presents potential one-year share gains of ~101%. (See WAL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.