There are murmurings on Wall Street that the big tech-led year-to-date rally is about to run aground, but according to one prominent Wall Street analyst, that is not the case at all.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

In fact, the opposite is true, says Wedbush’s Daniel Ives, who believes many are in for a positive surprise as Q2 earnings season gets underway. “We believe a new tech bull market has begun to take shape being led by the AI Revolution and we expect to see a better-than-expected 2Q earnings season for the tech space over the next few weeks,” the 5-star analyst opined.

According to Ives’ checks, catalyzed by not wanting to get left behind in the new AI-driven environment, in the June quarter, enterprise IT budgets have “started to show signs of improvement.”

And while the tech sector’s surge so far in 2023 has been built on multiple expansion rather than higher earnings, Ives thinks that is about to change. “We believe further evidence of this generational AI spending trend will be sprinkled in the forecasts/commentary from Microsoft, Google, Amazon, Nvidia, AMD, IBM, and other tech software/chip stalwarts during this key 2Q earnings season and be a catalyst for a broader tech rally ahead,” he explained.

With this in mind, we decided to get the lowdown on two equites Ives recommends investors load up on ahead of the anticipated surge. Running the tickers through TipRanks’ database, we found out that each boasts a “Strong Buy” analyst consensus. Let’s take a closer look.

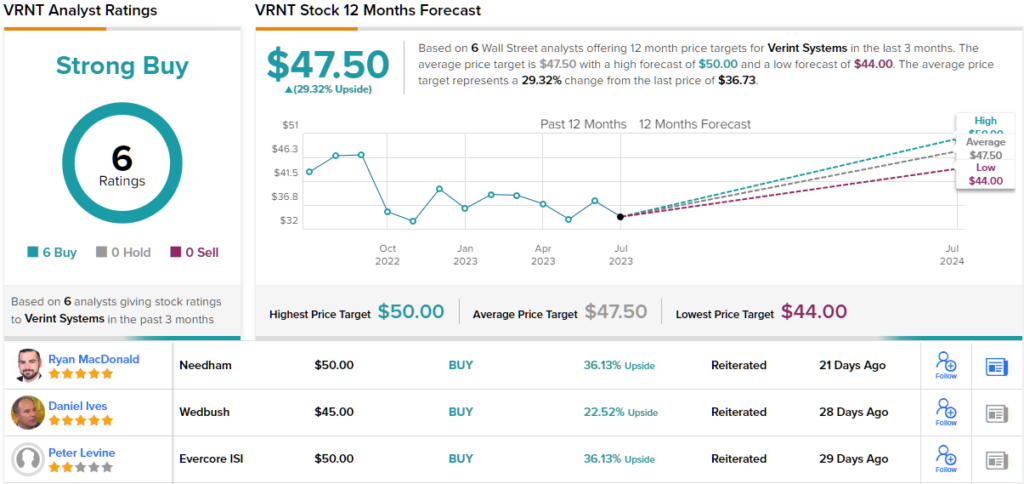

Verint Systems (VRNT)

First up, Verint Systems, a global provider of software and services and a leading player in the field of customer experience management, workforce optimization, and surveillance technology. The company’s comprehensive suite of software applications enables organizations to capture, analyze, and act upon vast amounts of customer and security-related data, helping them make informed decisions, enhance operational efficiency, and improve overall performance.

The company is also heavily involved in the AI game via its Da Vinci platform, an advanced analytics and artificial intelligence platform that leverages machine learning algorithms, natural language processing, and predictive analytics to extract actionable insights from various data sources.

Boosted by strong SaaS momentum, the company delivered a decent set of results in the most recent print – for the first quarter of fiscal 2024 (April quarter). While revenues dropped by 0.6% year-over-year, the figure reached $216.6 million compared to the Street’s $216.1 estimate. Adj. EPS hit $0.53, also above the Street at $0.47. For FY24, the company stuck to its guidance and for total revenue of ~$935.0 million (+/- 2%), SaaS revenue to increase by 25% and pro forma EPS of $2.65 at the midpoint, the same as the Street expected.

The stock, though, has not been getting much love this year and has remained flat so far. However, Ives thinks the AI opportunity is about to play out.

“VRNT continues to incorporate generative AI within its platform as customer engagement is a top priority for enterprises,” the top analyst explained. “We believe that VRNT has well-positioned itself to be an AI winner due to its Da Vinci platform with its robust and diverse customer engagement data… We continue to believe Verint continues capitalizing on its SaaS transition to further strengthen its profitable growth profile despite the current operating environment.”

All told, Ives rates VRNT shares as Outperform (i.e., Buy), while his $45 price target suggests the stock will climb 23% higher over the coming months. (To watch Ives’ track record, click here)

5 other analysts have recently waded in with VRNT reviews, and like Ives, they are all positive, providing this stock with a Strong Buy consensus rating. The average target is a bit higher than Ives will allow; at $47.5, the figure makes room for 12-month returns of ~29%. (See VRNT stock forecast)

Palo Alto Networks (PANW)

For our next Ives-recommended tech name, we’ll turn to Palo Alto Networks, a leading cybersecurity company known for its innovative solutions in network security. Founded in 2005, the company has established itself as a trusted provider of next-generation firewall and advanced threat prevention systems. With its emphasis on prevention rather than just detection and response, Palo Alto Networks aims to help organizations proactively safeguard their networks and data from cyberattacks, enabling them to operate securely in today’s digital landscape.

It’s a value proposition well-suited for the modern world, and it has helped the company deliver positive results in the FQ3 readout (April quarter) of May. During the quarter, revenue grew by 24% compared to the same period last year, reaching $1.7 billion, while meeting Street expectations. Additionally, Billings increased by 26% year-over-year, amounting to $2.3 billion. On the bottom line, adjusted EPS of $1.10 surpassed analysts’ forecasts by $0.17.

Looking ahead to FQ4, PANW anticipates revenue in the range of $1.937 billion to $1.967 billion, with the midpoint above the consensus at $1.95 billion. Moreover, adjusted EPS is projected to be in the range of $1.26 to $1.30, compared to analysts’ estimate of $1.18.”

That’s the sort of stuff the Street likes and despite a recent pullback over fears Microsoft is about to enter the cybersecurity arena, the shares have put in an excellent display in the tech-led rally – up by 70% year-to-date.

That’s not to say the stock has no room left to run. There’s more goodness on the way, according to Daniel Ives, who writes, “Based on our recent checks we believe the PANW cloud growth story is set to hit its next stage of growth and remains in a golden position of success over the next 12 to 18 months. We believe the risk/reward on this cyber security bellwether makes it a table pounder at current levels as the free cash flow story ramps further in Jokic-like fashion heading into FY24.”

Accordingly, Ives rates PANW shares an Outperform (i.e. Buy) to go alongside a $290 price target. The implication for investors? Upside of 22% from current levels.

Overall, this is a stock with plenty of coverage and almost all of it positive. Barring two Holds, all 29 other reviews say Buy, making the consensus view here a Strong Buy. The $257.59 average target suggests shares will generate 8.5% returns in the months ahead. (See PANW stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.